Key takeaways

- The German government regulates medical coverage by public health insurance. Thus, the plans from different public health insurance companies don’t vary much.

- You can save up to 1100 € per year by switching to a cheaper public health insurance company in Germany.

- We have developed a public health insurance cost calculator that you can use to determine your savings.

- The public health insurance premium is 14.6% of your gross monthly salary plus the additional contribution.

- Additional contributions are set independently by each insurance company.

This is how you do it

- Check the additional contribution (Zusatzbeitrag) of your current public health insurance provider.

- You should make the switch if your public health insurer’s additional contribution is greater than that of others.

- Based on the price-performance ratio, experts recommend TK, HKK, BKK Firmus, and Audi BKK as some of Germany’s best public health insurance companies.

- We find TK the best public health insurance provider for expats. Its website, mobile app, and customer service are in English. You can register with TK online.

- We recommend getting private health insurance via an insurance broker. They are experts and can help you find the best plan for your needs. You can book a call with an expert we recommend here.

The AI overview and answers are as good as the sources it uses.

To ensure you get AI answers from a deeply researched, maintained, and up-to-date source, add GermanPedia to your preferred sources.

Table of Contents

How do public health insurance companies calculate the insurance premiums?

Statutory health insurance premiums depend on your gross monthly income. It’s 14.6% of your gross income plus an additional contribution (Zusatzbeitrag in German).

Each public health insurance company sets its own additional contribution percentage. The average additional contribution is 2.9% (as of 2026).

So, the total public health insurance premium is 17.5% (14.6 + 2.9%) of your gross monthly salary as of 2026.

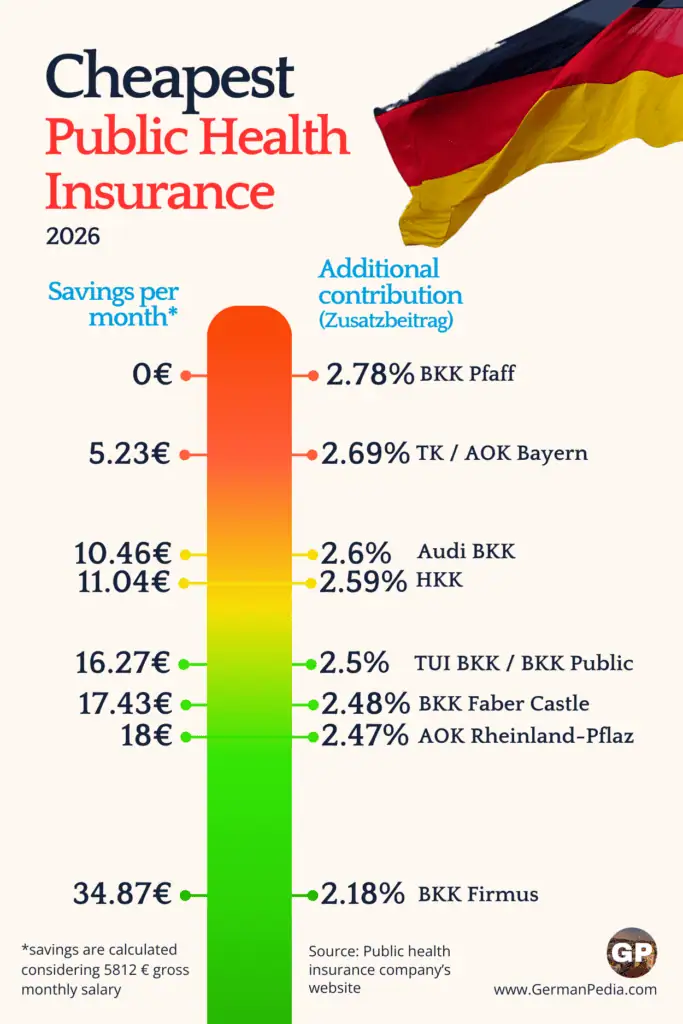

Cheapest health insurance companies in Germany

| Base health insurance contribution | 14.6% (as of 2026) | |

| Public health insurance company | Additional contribution (2026) | Additional contribution (2025) |

| BKK Firmus | 2.18% (=) | 2.18% |

| AOK Rheinland-Pfalz / Saarland | 2.47% (=) | 2.47% |

| BKK Faber-Castell & Partner | 2.48% ⬆️ | 2.18% |

| BKK Public | 2.50% ⬆️ | 2.30% |

| Tui BKK | 2.50% (=) | 2.50% |

| HKK | 2.59% ⬆️ | 2.19% |

| Audi BKK | 2.60% ⬆️ | 2.40% |

| AOK Bayern | 2.69% (=) | 2.69% |

| Techniker Krankenkasse | 2.69% ⬆️ | 2.45% |

| BKK Pfaff | 2.78% (=) | 2.78% |

BKK Firmus offers the lowest additional contribution of 2.18%. This is 0.6% less than BKK Pfaff, at the tenth spot on the list.

BKK24 Krankenkasse charges 4.39% for the additional contribution, which is the highest as of 2026. So, if you switch from BKK24 to BKK Firmus, you’ll save 2.21% of your gross monthly salary.

We find TK the best public health insurance provider for expats. It offers its website, mobile app, and customer support in English.

You can register with TK online for free in 2 minutes using our “TK registration service.“

Register with TK

- Biggest public health insurance company in Germany based on number of members.

- Enjoy low premiums

- Get English customer support, website, and mobile app.

- Complete the application process in English.

How much can you save by changing your public health insurance company?

All public health insurance companies offer similar services. Unlike private health insurance, public insurance plans don’t differ much.

So, it doesn’t matter which public health insurance provider you choose. However, switching to a public insurance company with lower additional contributions can save much money in the long run.

We have developed a public health insurance cost calculator that you can use to determine your exact savings.

If you are an employee, your savings will be half of a self-employed. It’s because your employer contributes half of the premium.

Public Health Insurance Cost Calculator

- Calculate how much different public health insurance companies cost.

- You can check if you are insured with the cheapest public health insurance.

- Calculate how much you can save by switching to cheaper public health insurance.

How do you change public health insurance in Germany?

You can change your public health insurance provider anytime without restriction. You can get a public health insurance plan directly from the new insurance provider.

Almost every public health insurance company offers online registration.

We find TK the best public health insurance provider for expats. It offers its website, mobile app, and customer support in English.

You can register with TK online for free in 2 minutes using our “TK registration service.“

Is Private health insurance the better choice for high earners?

Whether private health insurance is the right choice for you depends on your personal situation.

- Are you married?

- Do you have kids?

- How much do you earn?

- Does your partner earn?

- Your health condition

We know the German healthcare system is complex and can be confusing. So, we developed the “health insurance finder” tool to help you find which health insurance (public or private) is best for you and why.

However, if you are looking for the best medical coverage, private health insurance is the answer. But to be eligible for private health insurance in Germany, you should earn at least 77,400€ (as of 2026).

You should also check if you can afford private health insurance in the long term. It’s because returning to statutory health insurance is difficult.

Generally speaking, private health insurance is usually a better option for high-earners in Germany. This is because private insurance offers better medical coverage at a lower cost.

However, you cannot insure your non-working family members for free in private health insurance. You must get a separate private insurance policy for your non-working spouse and children.

So, if you are the sole earner in your family, private health insurance can be expensive.

We recommend getting private health insurance via an insurance broker. They are experts and can help you find the best plan for your needs. You can book a call with an insurance broker we recommend here.

Book a free call with a health insurance expert

- German health insurance is a complicated product. There are several factors that must be considered before deciding which health insurance is best for you. An expert can guide you and help you pick the best option for you.

- An Insurance broker is liable for their advice. This means if the policy they recommended doesn’t offer the coverage you requested, they are liable to pay the damages incurred in the future.

More topics

- Best private health insurance as per top rating agencies

- Switch from private to public health insurance

- Private vs public health insurance

- Private health insurance cost in old age

- Why is private health insurance cheaper than public health insurance?

- Employer’s contribution to private health insurance

- Private health insurance for self-employed

- Health insurance for students

- Health insurance for children

- Healthcare in Germany

- Best public health insurance in Germany

References

- https://www.bkk-firmus.de/leistungen/beitragssaetze/uebersicht-beitragssaetze.html

- https://www.hkk.de/versicherung-und-tarife/hkk-vorteile/preis-leistungs-vorteil

- https://www.audibkk.de/mitglied-werden/mitgliedschaft-bei-der-audi-bkk

- https://www.tk.de/firmenkunden/versicherung/beitraege-faq/beitragssaetze/hoehe-tk-beitragssaetze-2032248

- https://www.hek.de/einfacher-service/faq/faq-versicherung-beitraege/

- https://www.bertelsmann-bkk.de/ueber-uns/medien/news/neuerungen-2024

- https://www.ruv-bkk.de/mitgliedschaft/mitglied-werden/beitragssaetze/