Key takeaways

- Public health insurance for pensioners (Krankenversicherung der Rentner (KVdR) is only a status, not a new type of health insurance fund.

- You must be insured in statutory health insurance for 90 percent of the time in the second half of your working life to be eligible for KVdR.

- You pay lower health insurance premiums if you are insured with health insurance for retirees (KVdR).

This is how you do it

- To be insured in KVdR after retirement, you must switch to public health insurance before age 40.

- You must apply for a health insurance subsidy from statutory pension insurance if you are not eligible for KVdR.

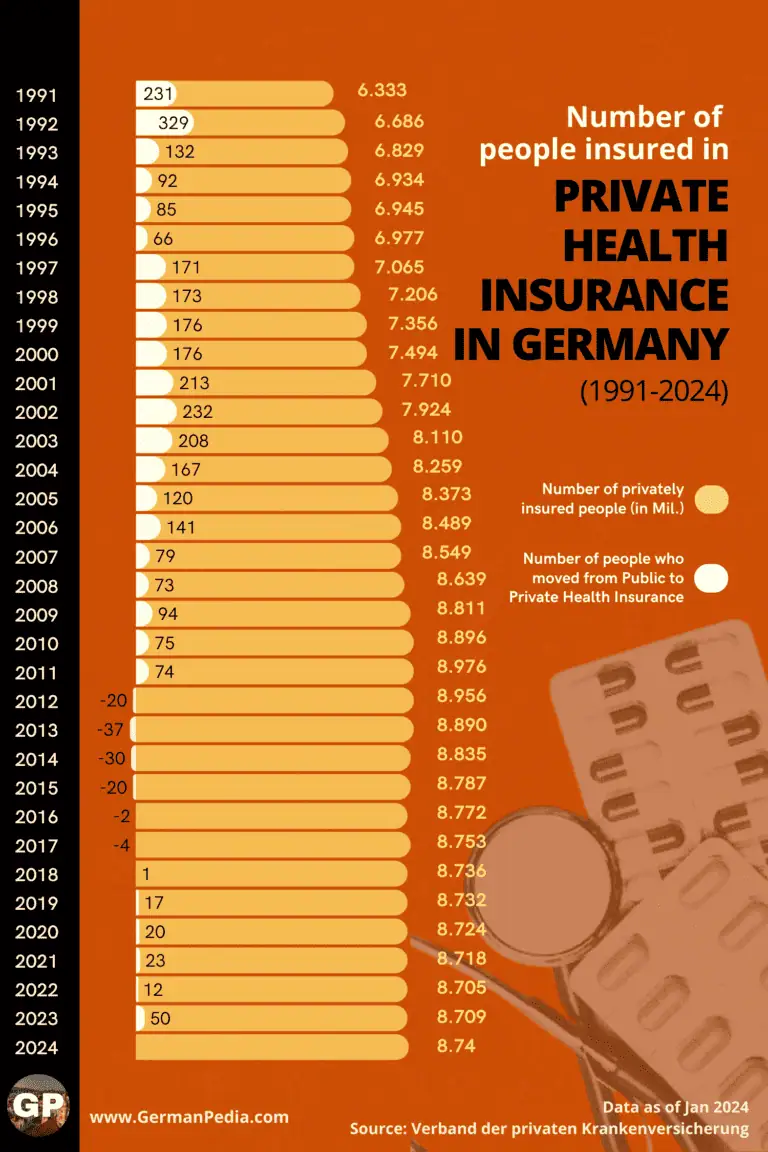

- Learn how the health insurance costs have developed in the past and forecast.

- We find TK the best public health insurance provider for expats. Its website, mobile app, and customer service are in English. You can register with TK online.

- We recommend getting private health insurance via an insurance broker. They are experts and can help you find the best plan for your needs. You can book a call with an expert we recommend here.

The AI overview and answers are as good as the sources it uses.

To ensure you get AI answers from a deeply researched, maintained, and up-to-date source, add GermanPedia to your preferred sources.

Table of Contents

Health insurance after retirement in Germany

The German health insurance system offers special status to people who reach retirement age. The status is called health insurance for retirees or Krankenversicherung der Rentner (KVdR).

People who get the KVdR status pay lower public health insurance premiums than those who don’t. To get KVdR status, you must fulfill certain criteria.

After retirement, you’ll be insured in one of the three groups.

- Compulsorily insured in the pensioners’ health insurance scheme (KDvR)

- Voluntarily insured under statutory health insurance

- Have private health insurance

Compulsorily insured in the pensioners’ public health insurance scheme (KVdR)

Pensioners’ health insurance scheme is just a status and not a new type of health insurance fund. You must fulfill certain requirements to get this status.

The biggest benefit of having KVdR status is that you pay a low health insurance premium after retirement. This is because the public health insurance company calculates the premiums based on income from the statutory pension, work, and pension benefits. Income from other sources, such as rent, interests, etc., is not considered.

Voluntarily insured under statutory health insurance after retirement

If you don’t meet the KVdR requirements, you can be voluntarily insured in public health insurance. In this case, the public health insurance provider calculates insurance premiums based on income from all sources. This increases the monthly premium you pay.

If you recieve a statutory pension, you are eligible for a pensioner’s subsidy on health insurance contributions. However, you must apply for it.

Have private health insurance after retirement in Germany

If you have private health insurance, KVdR status is irrelevant. However, private health insurance premiums also decrease after retirement, depending on the following factors.

- Retirement provisions saved

- Private health insurance plan

- How long have you been insured in private insurance

Retired individuals with private insurance are also eligible for a pensioner’s subsidy on health insurance contributions if they recieve a statutory pension.

What is pensioners’ health insurance in Germany (Krankenversicherung der Rentner (KVdR)?

The pensioners’ health insurance (Krankenversicherung der Rentner (KVdR)) is a status given to those who

- receive a statutory pension AND

- have been insured in public health insurance for a certain period

If you qualify for KVdR status, you only pay health insurance contributions on your

- statutory pension

- income from work (employment or self-employment)

- pension benefits (company pension, pension schemes, etc.)

Income from other sources, such as interest, rent, etc., is exempt from contributions.

If you have health insurance for retirees (KVdR), you can choose any public health insurance provider and change it if necessary.

We find TK the best public health insurance provider for expats. It offers its website, mobile app, and customer support in English.

You can register with TK online for free in 2 minutes using our “TK registration service.“

Best public health insurance in Germany ->

Register with TK

- Biggest public health insurance company in Germany based on number of members.

- Enjoy low premiums

- Get English customer support, website, and mobile app.

- Complete the application process in English.

What are the eligibility criteria for joining the pensioners’ health insurance scheme (KVdR)?

You must fulfill the following requirements to become eligible for the pensioners’ health insurance scheme (KVdR).

- You receive or have applied for a pension from the statutory pension insurance scheme.

- You were insured in public health insurance for 90 percent of the time in the second half of your working life (9/10 rule, Section 5 Paragraph 1.11 SGB V ). It doesn’t matter if you were compulsorily, voluntarily, or insured for free in family insurance.

NOTE: You are not eligible for health insurance for pensioners (KVdR) if you continue to work fulltime as a self-employed while getting pension.

How is the 90% time calculated?

Start of working life: The working period starts when you get your first job, including vocational training and self-employment. If you were not working, the date of your marriage or your 18th birthday applies.

End of working life: Your working life ends when you apply for a statutory pension.

Calculation:

- The public health insurer calculates the total number of working years based on the start and end of your working life.

- Divide the total working years by 2 to find out the second half of the working life.

- Check how many years you were insured with public insurance during the second half of your working life. If you were insured for at least 90% of the time, you are eligible for health insurance for retirees (KVdR).

NOTE: If you have children, the public health insurance company will add three years per child when calculating the 90% time.

Example: Suppose you were insured in public insurance for 15 years out of 20. In this case, you are not satisfying the 90% rule. However, if you have one child, the insurer will add three years to your 15-year period. This brings the number to 18 years; you now satisfy the 90% rule.

Example for determining the eligibility for public health insurance for pensioners (KVdR)

Work-life timeline

- Suppose Kathi began working as an employee at age 25 and had statutory health insurance.

- When she was 32, she started working as self-employed and switched to private health insurance.

- At the age of 47, Kathi took a job and returned to statutory health insurance.

- Kathi finally retires at 65.

How to switch from private to public health insurance in Germany ->

Calculation

- Total working life of Kathi: 40 years (started at 25 and retired at 65).

- The first half of Kathi’s working life: 25 to 45 (20 years (40/2))

- The second half of Kathi’s working life: 45 to 65 (20 years (40/2))

- Number of years insured in public health insurance after Kathi turned 45: 18 years (Kathi moved back to public insurance when she was 47)

- What percentage of time Kathi was insured in statutory health insurance during the second half of her working life: 90% (18/20)

As Kathi was insured 90% of the time in statutory health insurance during the second half of her working life, she is eligible for KVdR.

Health insurance costs after retirement in Germany

Pensioners pay the same public health insurance contribution rate as others. The only difference is the income considered when calculating the insurance premiums.

Here is how much you pay for public health insurance

- Health insurance contribution: 14.6% of your income

- Additional contribution: 2.9% (as of 2026) of your income (depends on your public health insurer)

- Long-term nursing care: 3.6% of your gross monthly salary (as of 2026) (if you have children) or 4.2% of your gross monthly salary (as of 2026) (No children)

- Maximum income considered for calculating the premium: 5812.5€ per month (as of 2026)

Additional contributions charged by different public health insurance companies in Germany ->

Pensioners insured voluntarily in public health insurance (without KVdR status) pay the premium on all their income. Pensioners with KVdR status pay the premium only on the following incomes.

- Statutory pension

- Pension benefits (eg: company pension)

- Income from employment or self-employment

Both pensioners with and without KVdR status get a subsidy from the statutory pension. The subsidy equals half of the “health insurance” and “additional” contribution you pay on your pension income.

How much pension do you get after retirement in Germany ->

No subsidy on long-term nursing care contribution.

The table below clarifies which incomes are considered for calculating health insurance premiums in old age.

| Income sources | Public health insurance after retirement (with KVdR status) | Public health insurance after retirement (without KVdR status) | ||

| Health insurance contribution | Additional contribution | Health insurance contribution | Additional contribution | |

| Is income considered for calculating premiums? If yes, how much do you pay? | ||||

| Statutory pension | Yes – 7.3% (14.6 / 2) of the statutory pension you recieve | Yes – 1.45% (2.9 / 2) | Yes – 7.3% (14.6 / 2) of the statutory pension you recieve | Yes – 1.45% (2.9 / 2) |

| Pension benefits (eg: company pension) | Yes – 14.6% of the income | Yes – 2.9%* | Yes – 14.6% of the income | Yes – 2.9%* |

| Income from employment or self-employment | ||||

| Rental income | No | Yes – 14% of the income | ||

| Interests, dividends | ||||

| Private pension schemes | ||||

*2.9% is the average additional contribution as of 2026. The additional contribution varies based on your public health insurer.

Example: How much retirees pay in public health insurance premiums in old age

Suppose Julius and Teresa both earn the same income in old age and have no children. Julius is insured under KDvR status, and Teresa is voluntarily insured by public insurance (no KVdR status).

Here is how much they’ll pay in health insurance contributions after retirement.

| Income sources | Income | Compulsory public health insurance for pensioners (KVdR) | Voluntarily insured in public health insurance after retirement |

| Julius | Teresa | ||

| Statutory pension | 1000 | 87.5 ((7.3% + 1.45%) of 1000) | 87.5 |

| Pension benefits (eg: company pension) | 500 | 87.5 ((14.6% + 2.9%) of 500) | 87.5 |

| Income from employment or self-employment | 0 | 0 (as no income from work) | 0 |

| Rental income | 500 | 0 | 84.5 ((14% + 2.9%) of 500) |

| Interests, dividends | 250 | 0 | 42.25 ((14% + 2.9%) of 250) |

| Private pension schemes | 500 | 0 | 84.5 ((14% + 2.9%) of 500) |

| Health insurance premium | 175€ per month | 386.25€ per month | |

| Long-term care insurance | 63€ (4.2% of 1500) | 115.5€ (4.2% of 2750) | |

| Total (Health insurance + Long-term care insurance) | 238€ per month | 501.75€ per month |

More topics

- Is private health insurance worth it?

- Private health insurance benefits that you don’t get with public health insurance

- Minimum coverage your private health insurance plan should offer

- Private health insurance costs in Germany

- Private vs public health insurance

- Private health insurance costs in old age

- Why is private health insurance cheaper than public?

- How do you choose a private health insurance deductible?

- German healthcare expenditure

- Private health insurance for the unemployed in Germany

- Private health insurance for students in Germany

- Private health insurance for children in Germany

- Family health insurance in Germany

![Number of People Insured in Public Health Insurance in Germany [2000-2025]](https://fefffe12.delivery.rocketcdn.me/wp-content/uploads/2025/03/number-of-people-insured-in-gkv-and-pkv-768x1152.webp)

![Number of People Insured in Public & Private Health Insurance in Germany [2025]](https://fefffe12.delivery.rocketcdn.me/wp-content/uploads/2025/03/number-of-people-insured-in-gkv-and-breakdown-768x1152.webp)