Learn everything about company pension schemes in Germany. Understand when it makes sense to join a company pension plan, changes in German law regarding occupational pension, and alternatives to company pension insurance.

Key Takeaways

- The company pension plan is for employees only. And every employee in Germany has the right to get a company pension plan.

- Since 2019, every employer in Germany must add at least 15% to the employees’ pension contributions on top.

- Companies can implement company pension insurance in five ways; direct insurance, pensionfonds, pensionskasse, provident fund, and direct commitment by a company.

- Usually, it’s not worth taking a company pension in Germany. Instead, it’s better to invest in ETFs or real estate.

This is how you do it

- If your employer contributes more than 25% to the company pension plan, it’s worth joining it.

- If the company pension plan guarantees at least 2% interest and the option to get the complete pension in one lump sum, you should consider joining the pension plan.

- Open a free ETF savings plan with one of the brokers in Germany. Contribute a fixed amount every month to build your retirement provisions. You can open a free ETF savings plan with Scalable Capital*

- Investing in real estate is another way to build your old age provision.

Table of contents

What is a company pension scheme in Germany?

A company pension scheme or occupational pension scheme is for employees only. It is called “betrieblicher Altersvorsorge (bAV)” in German.

Under the company pension scheme, you and your employer contribute to the monthly pension contribution. And in return, you get monthly pension payments after retirement.

You pay the monthly premium from your gross salary (deferred compensation). Thus, don’t pay taxes and social contributions. And your employer adds at least 15% of the pension contributions on top.

You have the following options to get paid after retirement.

- Monthly pension throughout life.

- All the capital is paid out immediately after retirement (lump sum payout).

- Part of the capital is paid out immediately after retirement, and the rest is in monthly pensions.

For example, suppose you want to contribute 250 € every month to your company pension plan.

In this case, your net income will reduce by approx. 129.43 € only as you pay 250 € from your gross salary. But you invested 250 € + 37.5 € (15% of 250 € from your employer) into the company pension scheme.

Thus, you save 120.57 € monthly in taxes and social security contributions and get 15% (37.5 € every month in this example) from the employer for free.

NOTE: All these savings might suggest that taking a company pension scheme is a no-brainer. But in reality, it’s not worth taking a company pension scheme, as you’ll see next in this guide.

Is it worth taking a company pension policy in Germany?

No, taking a company pension scheme in Germany is not worth it for three main reasons.

- You’ll pay income tax and social security contributions on your monthly pension after retirement. It’ll eliminate the tax advantages you enjoyed during the savings phase.

- You might not live long enough to get back what you paid into the pension.

- You contribute to the company pension from your gross salary. Hence, you enjoy tax benefits and low social security contributions. But at the same time, with reduced gross income, your monthly contribution to the statutory pension insurance also declines. Hence, reducing your statutory pension after retirement. Thus, consider it while calculating the company pension benefits.

You can learn about other pension provisions available in Germany in our guide on Pensions in Germany.

Sample calculation to illustrate company pension schemes aren’t worth it

During the savings phase

| | Monthly | Total capital saved in 30 years (No interest earned) |

|---|---|---|

| Gross Salary | 3150 € | |

| Monthly contribution to the company pension scheme from your gross income | 184 € | 66240 € (184 € per month * 12 months * 30 years) |

| Employer’s contribution to the company pension scheme | 27.6 € (15% of 184 €) | 9936 € (27.6 * 12 * 30) |

| Total contributions to the company pension scheme | 211.6 € (184 + 27.6) | 76176 € (66240 + 9936) |

| Tax savings | 48 € | |

| Social Security contributions savings | 36 € | |

| Your contribution to the company pension insurance or reduction in your net salary | 100 € (184 – 48 – 36) | 36000 € (100 * 12 * 30) |

Source: Finanztip

During the retirement phase, if paid out at once

| | No interest earned during the savings phase | 2% interest earned during the savings phase |

|---|---|---|

| Total capital saved in a company pension scheme or the gross amount you are entitled to get after retirement | 76,176 € | 102,786 € |

| Tax on the saved capital | 10,360 € (13.6 % of total capital) | 14,784 € (14.3 % of total capital) |

| Social security contributions on the saved capital | 14,305 € (18.7 % of total capital) | 19,008 € (18.5% of total capital) |

| The net reduction in the statutory pension scheme due to contribution to the company pension plan | 42 € per month 10,080 € (42 * 12 * 20) Assuming you live till you are 85 years. So, if you retire at 65, you’ll receive 42 € per month less state pension for 20 years. | 42 € per month 10,080 € (42 * 12 * 20) |

| Total Deductions on your gross pension amount | 34,745 € (Tax + Social Security + Net state pension reduction) | 43,872 € |

| Net capital you’ll get after retirement | 41,431 € | 58,914 € |

| Net profit | Net capital received after retirement – Net amount contributed 41431 € – 36000 € = 5431 € | 58914 € – 36000 € = 22,914 € |

During the retirement phase, if paid out monthly

| | No interest earned during the savings phase | 2% interest earned during the savings phase |

|---|---|---|

| Gross company pension | 213 € per month | 292 € per month |

| Tax on pension | 29 € (13.6 % of total capital) | 42 € (14.3 % of total capital) |

| Social security contributions | 40 € (18.7 % of total capital) | 54 € (18.5% of total capital) |

| The net reduction in the statutory pension scheme due to contribution to the company pension plan | 42 € per month | 42 € per month |

| Net company pension | 102 € | 154 € |

| Number of years to get back your contributions | 29 years = 36000 / (102 * 12 months) If you retire at 65, you’ll be 94 till you get the contributed amount back. | 19 years = 36000 / (154 * 12) If you retire at 65, you’ll be 84 till you get the contributed amount back. |

Source: Finanztip

Summary

| Your net contribution to the company pension plan in 30 years. | 36,000 € (100 € per month) | |

|---|---|---|

| Company Pension Insurance | No interest | 2% interest |

| Net profit after retirement if the saved capital is paid out at once | 5431 € (15% of 36k) | 22,914 € (63% of 36k) |

| The number of years to get back contributed amount if you receive a monthly pension. | 29 years | 19 years |

| ETF Investment | 2% interest | 4% interest |

| Monthly contribution from net income | 100 € | 100 € |

| Gross capital after 30 years | 49,655 € | 70,000 € |

| Gross profit after 30 years | 13,655 € (49,655 – 36,000) | 34,000 € (70k – 36k) |

| Capital gains tax on the profit | 3413 € (25% of 13,655) | 8500 € (25% of 34k) |

| Net profit after 30 years | 10,241 € (13,655 – 3413) | 25,500 € (34k – 8500) |

It’s clear from the above table that there is no significant benefit to taking a company pension scheme in Germany, especially if you opt for monthly pension payments.

Moreover, you can achieve the same or better returns if you invest in an ETF savings plan from your net income.

In a company pension plan, you must live for at least 29 or 19 years after retirement to regain your saved capital (36k €) if you opt for monthly pension benefits after retirement.

It means you’ll be 94 or 84 years old by the time you get all your saved capital back.

Unfortunately, the average life expectancy in Germany is 78.3 years for men and 83.2 years for women.

Thus, most people don’t even get back the amount they contributed from their net income, i.e., 36k € (in our example).

On the other hand, you have full access to your money invested in the ETF savings plan. And you can do whatever you want with it.

Thus, investing money in low-cost broad market ETFs makes more sense than taking a company pension scheme in Germany.

When does it make sense to take company pension plans?

The company pension plans make sense in the following cases.

- Your employer contributes 25% or more to your company pension schemes.

- Your employer guarantees at least 2% interest on the savings, and you take out a lump sum payout after retirement.

However, not many employers in Germany offer such generous contributions or guarantee an interest rate.

But you can negotiate the employer’s contribution to the pension during compensation negotiations.

How many employees in Germany have occupational pension schemes?

| Total employed population in Germany | 45.7 million as of Jun. 2023 45.3 million as of Dec. 2019 |

| | as of 2019 |

| Total employees with one or more types of company pension schemes | 18.2 million (40.1% of total employees in Germany) |

| Total active company pension plans in Germany | 21 million (It means people took multiple company pension schemes) |

| Pensionsfonds | 0.5 million |

| Pensionskasse | 4.7 million |

| Direct commitments and Provident fund | 4.7 million |

| Direct insurance | 5.2 million |

| Public supplementary pension providers | 5.8 million |

Changes in German law concerning company pension schemes

Here is a timeline of the German government’s changes to the company pension schemes.

- Since 2002: Employees in Germany have the right to pay part of their monthly gross salary into a company pension contract. As you contribute to the pension insurance from the gross salary, you defer your income to the future. Thus it’s also called “deferred compensation.”

- Until 2017: To receive a company pension, you must have stayed with the company for at least 5 years and be at least 25 years old when leaving the company.

- From 2018: To receive a company pension, you must have stayed with the company for at least 3 years and be at least 21 years old when leaving the company.

- Since 2018: You can contribute up to 8% of the German state pension contribution assessment limit tax-free into a company pension plan. So, as the “German state pension contribution assessment limit” increases, your tax-free contribution to the company pension plan also increases. You can contribute 584 € per month tax-free to your company pension scheme in 2023. The tax-free amount is increased to 604 € per month in 2024.

- Since 2018: Similarly, contributions to the company pension plan of up to 4% of the “German state pension contribution assessment limit” is free from social security contributions. It’s 292 € per month in 2023 or 302 € per month in 2024.

- Since 2019: Every employer in Germany must add at least 15% to the employees’ pension contributions.

- Since 2022: Every employer in Germany must subsidize existing company pension contracts signed before 2019.

- Since 2020: After retirement, you don’t pay health insurance contributions on the first 169.75 € of your monthly pension benefits.

- 2023: You can contribute 584 € per month tax-free to your company pension scheme in 2023. Similarly, you can contribute 292 € per month to your company pension plan without paying any social security contributions.

- 2024: The tax-free amount is increased to 604 € per month in 2024. Similarly, the social security contributions limit is increased to 302 € per month in 2024.

How many types of company pension schemes are available in Germany?

There are 5 types of company pension schemes in Germany.

- Direct insurance (Direktversicherung in German)

- Pension fund (Pensionskasse in German)

- Pension fund (Pensionsfonds in German)

- Provident fund (Unterstützungskasse in German)

- Direct commitment by a company (“Direktzusage eines Unternehmens” in German)

All types of company pension plans have the same core concept. They differ regarding who takes the pension insurance policy and where your money is invested.

Direct insurance (Direktversicherung in German)

A direct pension plan is the most popular form of the company pension scheme. In it, your employer takes a life or pension insurance policy on your behalf.

As the employer takes the pension insurance policy for all its employees, it can negotiate good offers with the insurance companies. But it also comes with a limitation.

The limitation is that your new employer might not take over your current company pension plan. The reason is employers don’t want to manage pension contracts from different insurance providers.

Hence, direct insurance is not the best option for frequent job changers.

Pensionskasse

In this form of company pension scheme, employees contribute to a pension fund (Pensionskasse) every month from their gross salary.

The Pensionskasse does not invest your money in ETFs or high-risk investments. Instead, it puts your money in safe bonds.

Hence, Pensionskasse guarantees a minimum pension in the retirement phase. But offer low-interest rates on your saved money.

Pensionsfonds

Pensionfonds are similar to Pensionskasse. The only difference here is the pension company invests your money in ETFs or high-risk investments.

Hence, offering higher returns with higher risks.

Provident fund (Unterstützungskasse in German)

In this type of company pension plan, pension contributions go into a legally independent institution. The provident fund institution manages the money and invests it where ever it sees fit.

In a provident fund pension plan, your employer has a say on where the money is invested. Moreover, your employer can take a loan against the provident fund.

But don’t worry; your pension is secure even if your employer goes bankrupt.

The insurance company that manages the provident fund ensures that your pension is safe by taking an insurance policy.

As your insurance company takes insurance to reduce the risk, it’s also called a reinsurance policy.

Lastly, there is no upper limit to the provident fund pension plan contributions. So, high earners can maximize the tax benefits by contributing more from their monthly gross salary.

Direct commitment by a company (“Direktzusage eines Unternehmens” in German)

Your employer finances the direct commitment pension insurance plan. Depending on how your employer has set up the pension provision, you may not have to contribute anything to the pension scheme.

So, your employer invests the money, which later finances your pension.

Employers may promise an exact pension amount after retirement or that you’ll receive at least the contributions made by you.

But lately, very few employers in Germany offer direct commitment pension schemes. It’s because the risk of being unable to fulfill the pension benefits promise is too great.

Still, you should check with your employer about the company pension provisions they offer. And if your company offers a fully financed pension plan, definitely take it.

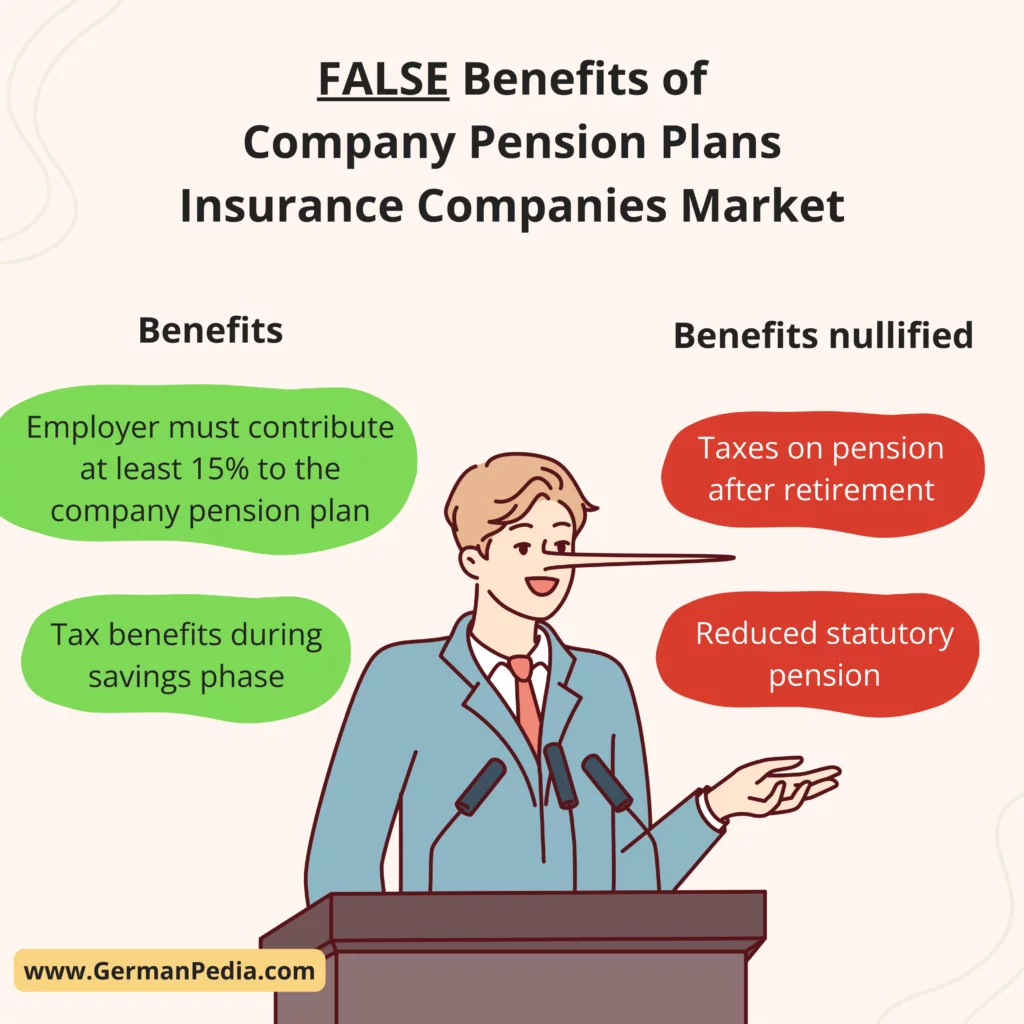

Advantages of the company pension scheme Germany

- Tax and social security benefits as you pay the contributions from your gross salary. But the tax and social security benefits are limited to 584 € and 292 € per month, respectively.

- As per German law, every employer in Germany must contribute at least 15% to the company pension scheme.

But you must pay tax and social security on your monthly pension after retirement. Unfortunately, it eliminates all the benefits you enjoyed during the saving phase.

So, it would be fair to say these are the false benefits of company pension schemes that insurance companies market.

Not only company pension plans, but most pension schemes in the German pension system are not worth joining, e.g., private pension plans.

Alternatives to company pension schemes in Germany?

There are two alternatives to occupational pension provision.

- Invest in broad-market ETFs

- Invest in real estate

ETF saving plan

You can open a free ETF savings plan with a broker in Germany and invest in low-cost broad-market ETFs.

Investing yourself allows you to use your money how you want. Moreover, the capital gain tax you must pay when selling your investment is flat at 25%.

In the case of a pension, you pay income tax and social security contributions on your monthly pension, which add up to more than 25%.

You can open a free ETF savings plan with Scalable Capital*.

Scalable Capital

- Free savings plans for all ETFs

- Invest from 1 euro savings amount

- Flexible execution dates and frequencies

Finanzen.net Zero

- Very low fees

- Free savings plans

- The account and securities custody are held by Baader Bank

Real estate investment

Another proven alternative to pension insurance is buying a property. You can rent the property or live in it yourself. Either way, it’s better than the company pension schemes.

You can sell the property when you retire for a lump sum payout. Moreover, you don’t pay any taxes on your profit if you sell the property after 10 years.

Other options are to live rent-free in your property or rent it out to supplement your pensions from statutory pension insurance.

You can learn more about buying a house in Germany in our guide.

Buy a house in Germany – eBook

- The process of buying a house in Germany.

- Understand mortgage process, property documents and evaluation, and more.

- Tips and tricks to save thousands of euros.

- Average renovation costs in Germany.

How to get a company pension plan in Germany?

Every employee in Germany has the right to company pension insurance.

You can ask your employer if they offer any occupational pensions. If yes, you can participate in it. Otherwise, you can take a company pension policy yourself.

Moreover, since 2019, employers in Germany must add at least 15% to the employee’s pension contributions on top.

FAQs

Is a company pension scheme mandatory in Germany?

No, taking a company pension plan is not mandatory in Germany.

You have the right to a company pension plan. Whether you execute that right is your choice.

What happens to my company pensions when I switch jobs?

The amount you saved in the occupational pension provision isn’t lost when you switch jobs.

There are four main options in this situation.

- You can continue the old company pension plan on your own. It means you’ll be contributing from your net income instead of gross. Hence, you won’t benefit from the social security and tax incentives.

- Your new employer takes over the old company pension policy. However, it’s rare for new employers to do so as they don’t want to manage pension contracts from different providers.

- Transfer your existing saved capital to the company pension scheme of your new employer. There are transfer fees involved, which may reduce your saved capital.

- Lump sum payoff as part of the severance package. You can request your employer to pay off the capital saved in the company pension plan as part of the severance package. But you have to repay the saved taxes and social security contributions.

What happens to my company pensions if the employer files for bankruptcy?

You don’t have to worry about losing your company pension, even if your company goes bankrupt.

Pension Insurance Association (Pensionssicherungsverein (PSV)) takes over your company pension payments.

References

- https://www.weltsparen.de/altersvorsorge/betriebliche-altersvorsorge/

- https://www.sparkasse.de/pk/produkte/altersvorsorge/betriebliche-altersvorsorge.html

- https://www.finanztip.de/betriebliche-altersvorsorge/

- https://www.destatis.de/EN/Themes/Economy/Short-Term-Indicators/Labour-Market/karb811_x13a.html

- https://www.destatis.de/EN/Themes/Society-Environment/Population/Deaths-Life-Expectancy/_node.html

- https://www.destatis.de/EN/Themes/Labour/Labour-Market/Employment/_node.html#sprg482884

- https://www.bmas.de/SharedDocs/Downloads/DE/Rente/alterssicherungsbericht-2020.pdf?__blob=publicationFile&v=1