Key takeaways

- You need a valid German visa to get a mortgage in Germany, preferably permanent residence.

- A low interest rate or borrowing rate is not always the best offer. Therefore, it is essential to understand how your bank calculates the interest rate before signing the mortgage contract.

- Real estate investors prefer low monthly installments.

- In Germany, you don’t have to repay the entire mortgage within the loan tenure. You (the borrower) can refinance the remaining principal once the tenure ends.

This is how you do it

- The first step is to contact your home bank in Germany to enquire about the mortgage conditions.

- Contact different banks to explore various mortgage options.

- Contact mortgage brokers like Dr. Klein*, and InterHyp* to find the right mortgage product.

- Negotiate the mortgage terms with the banks. Bidding banks against one another is the best way to negotiate a mortgage offer.

- Once you find the right home loan, sign the deal 14 days before signing the purchase contract.

- We have written a book on buying a house in Germany. It explains the complete buying process, how to invest in German real estate, and offers expert tips that'll save your thousands of euros.

Table of contents

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

You found your dream house and want to get a mortgage against it. But you don’t know how to apply for a mortgage in Germany.

This guide explains how to apply for, receive, and evaluate a mortgage offer in Germany.

Buying a home in Germany is time-consuming and involves a lot of money. There are a lot of things you must know before buying a property.

Thus, we wrote a book on buying a house in Germany to make it simple for you. Read it to learn everything there is about buying a property in Germany.

Master German Home Buying Process

in 12 Days For FREE

- Learn complete process of buying a house in Germany and how to invest in German real estate.

- Understand mortgage process, property documents and evaluation, and more.

- Expert tips that’ll save you thousands of euros.

- Know average renovation costs in Germany to plan and negotiate better.

Process of getting a mortgage in Germany

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

Here are a few steps you have to follow to get a mortgage.

- Check if you qualify for a mortgage in Germany

- Find out the maximum mortgage you can get in Germany as an expat.

- Prepare the documents banks in Germany need to issue a mortgage.

- Contact different banks and brokers to explore your mortgage options.

- Negotiate the mortgage terms with the banks.

- Finalize a bank and submit the required documents.

- Wait for the bank to create a draft of your mortgage contract.

- Check the mortgage contract draft. If everything looks good, sign the contract.

Let’s understand each step in detail.

#1 Can expats get a loan in Germany?

Yes, you get a home loan in Germany as a foreigner. But you must fulfill the following requirements.

- You have a valid German resident permit. It’s tough for Blue Card holders to get good mortgage rates in Germany.

- You are living and working in Germany.

#2 How do you determine the maximum mortgage you can get?

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

Knowing the maximum mortgage you are eligible for is critical. This gives you a budget for finding your dream house in Germany.

You can determine the maximum mortgage you can get in two ways.

- By contacting banks and brokers

- By calculating yourself

Contact your home bank to explore mortgage products

The home bank is where you have a salary account. Ask your bank consultant, “What is the maximum mortgage you can get to buy a property in Germany?”

The reasons for starting with the home bank are

- You have a history with your home bank.

- They have most of your details.

Thus, taking out a mortgage from your home bank is easier.

Contact other banks for mortgage possibilities.

You should contact at least two more banks for mortgage offers. The reasons for contacting other banks are:

- Different banks offer different mortgage conditions.

- Few banks may reject your mortgage application. But that doesn’t mean you cannot get a mortgage elsewhere.

- You get an idea of the current home loan market.

- You can bid one bank against another to get the best German mortgage rates.

Contact mortgage brokers for further mortgage offers

The mortgage brokers are middlemen who have relations with several banks. They connect banks and potential clients. They can help you find the right mortgage product.

Mortgage brokers offer free consultation. The bank pays them after a successful mortgage contract.

There are many mortgage brokers in Germany. The major players are Dr. Klein* and InterHyp*.

You must work with a good bank consultant or mortgage broker. Buying a house is a long process that takes several months. You’ll have a lot of questions during the process.

Thus, you need someone who is available for you and can answer your doubts.

Interhyp – Mortgage brokers in Germany

- Offer support in finding the right mortgage product.

- Help you understand the process of buying a property in Germany.

- A mortgage broker can find mortgage options from several banks within minutes.

Dr. Klein – Mortgage brokers in Germany

- Offer support in finding the right mortgage product.

- Help you understand the process of buying a property in Germany.

- A mortgage broker can find mortgage options from several banks within minutes.

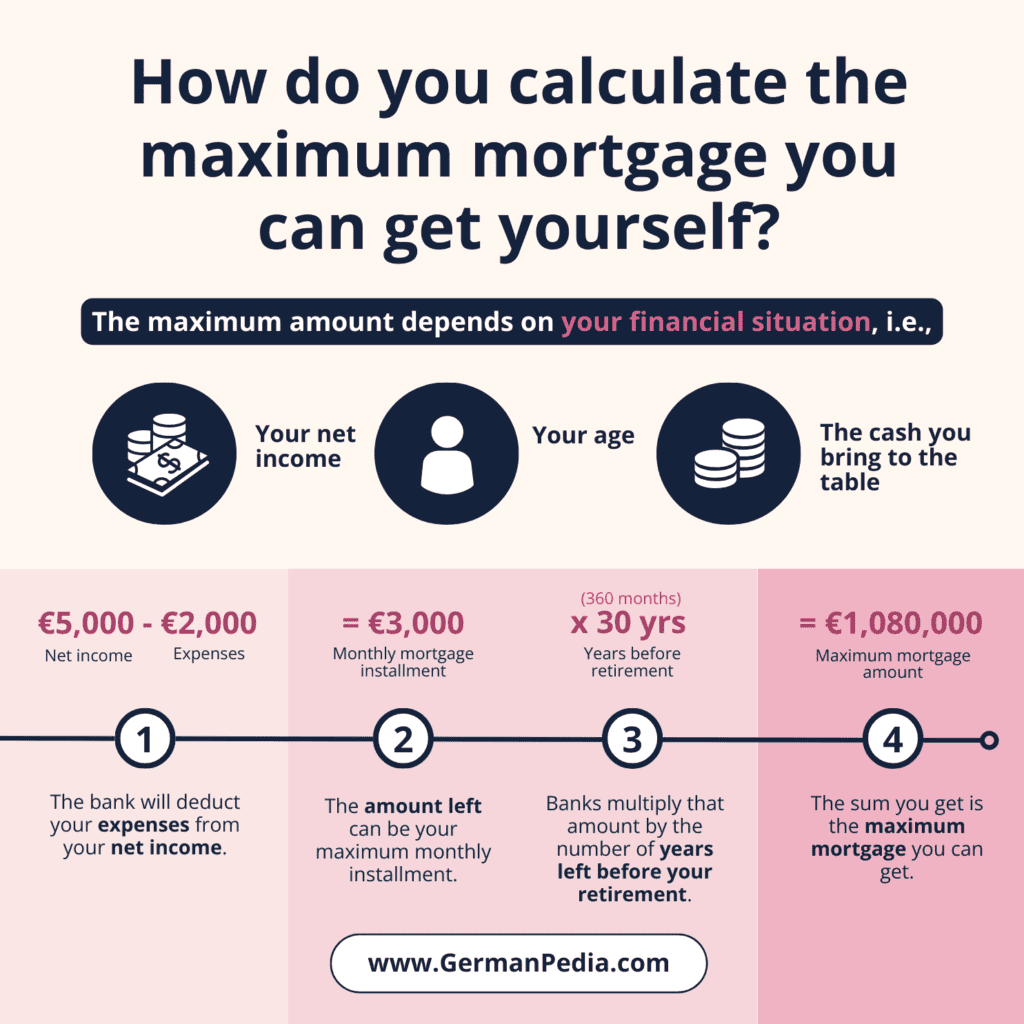

How do you calculate the maximum mortgage you can get yourself?

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

The maximum amount of mortgage you can get depends on your financial situation, i.e.,

- Your net income

- Your age

- The cash you bring to the table

Here are the steps to calculate the maximum mortgage amount.

- The bank will deduct your expenses from your net income.

- The amount left can be the maximum monthly installment you can pay.

- Lastly, banks multiply that amount by the number of years you can work until retirement.

- The sum you get is the maximum mortgage you can get.

⚠️ NOTE: You must cover the cost of buying the property (Nebenkosten) from your own pocket to be eligible for the mortgage. The cost of buying a property in Germany is approximately 7% to 12% of the property’s purchase price.

For example, suppose you want to borrow 700,000€ from the bank. In this case, you must bring at least 70k € to 84k € from your pocket.

Do not confuse “Nebenkosten” with the down payment. As of September 2024, banks in Germany offer 100% financing, so you don’t have to make a down payment.

#3 List of documents you need to apply for a mortgage in Germany

Banks will need your and the property’s documents to offer a mortgage.

Your (borrower) documents to apply for a mortgage in Germany

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

If you’re employed:

- Last 2 or 3 months’ salary slips

- December salary slip of the previous year

- Lohnstuerbescheid/Einkommenstuerbecheid: It summarizes the salary you received in a particular year. You get this document from your employer every year.

- Job contract: Banks prefer to give a mortgage to someone with a permanent (Unbefristet ) working contract.

If you are self-employed, the bank would like to see a stable source of income. To prove it, you have to show:

- Financial statement of your business, i.e., Balance sheet, Income statement, and Cash flow statement.

- 2 or 3 years of business tax returns

- 2 or 3 years of your tax returns

The bank may ask for other documents based on your business or the nature of your work.

Other documents:

- Insurance contracts, if any. E.g., life insurance, Car insurance, etc. Banks want to know what portion of your income goes into paying insurance premiums.

- Proof that you can pay Nebenkosten. You can prove that by showing one or a combination of the following.

- Account statements

- Bauspar konto, if any

- Stock trading account

- Any other mortgage-friendly scheme.

- Retirement account statements (Rentenversicherung): The document shows the amount in your retirement fund and the approximate monthly income after you retire.

- For banks, it’s preferable that you pay back the mortgage before retirement. But, if it’s not possible, this statement helps banks decide whether the borrower can repay the mortgage after retirement. So the younger you are, the better it is. You receive this document automatically once per year.

- You can also request the document online from Deutsche Rentenversicherung’s website.

- Personal identification documents: Passport and Permanent residence card (Niederlassungerlaubnis).

⚠️ Note: If you do not have a permanent residence or citizenship, getting a mortgage could be difficult.

Lastly, if you are applying with your spouse, the same documents would also be required for your spouse. Applying together with a spouse doesn’t improve the interest rate, but it increases the amount of credit you can get.

Property documents you need to get a loan in Germany

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

- Property expose: Expose contains the basic information about the property

- Property address

- Construction year

- Purchase or Ask price

- Broker’s commission, if any

- Property’s images, etc.

- Living area calculation (Wohnflächenberechnung): The document shows the size of every space/room of the property.

- Floor plan (Grundriss): A type of drawing that shows the property’s layout from above.

- Site plan (Lageplan): The document shows a large-scale drawing of the full extent of the site for an existing or proposed development.

- Land register papers (Grundbuchauszug): The document shows the names of the current and previous owners, third-party rights (e.g., mortgage), and the description of the property.

- Energy efficiency certificate (Energieauweis): The document shows the energy efficiency of the property or property building.

- Declaration of division (Teilungserklärung): As the name suggests, it documents how the property is divided. So, which portion of the property building belongs to you, and which comes under the House Union?

- Rent contract (Mietvertrag): The bank will also require this document if you buy a rented property.

The above list covers the minimum set of documents a bank may request. Banks may ask for further documents depending on your situation and the property you plan to buy.

Read our guide on German property documents to learn more.

#4 How do you negotiate with German banks to get the best mortgage offer?

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

Contact banks and mortgage brokers like Dr. Klein* and InterHyp* to explore mortgage possibilities.

Different banks will present different mortgage offers. You can use these offers to bid banks against each other. This is the best way to negotiate mortgage offers.

Don’t hesitate to negotiate or bargain with banks. You will be surprised by how flexible banks can be.

You can negotiate with banks on the following terms of the mortgage contract.

- Effective interest rate (Effectivzins): The lower, the better. But keep an eye on how banks calculate interest.

- Monthly installment: Investors prefer a lower monthly installment to achieve maximum positive cash flow.

- Fixed vs. variable interest rate: A Fixed interest rate means the borrowing rate will remain fixed throughout the mortgage tenure. A variable interest rate means the borrowing rate may change during the mortgage tenure. During the low-interest period, the longer the fixed interest, the better.

- Mortgage tenure: Length of the mortgage contract. The interest rates increase with the length of the mortgage tenure. You pay a higher interest rate for a 20-year mortgage tenure than 10. So, find the right balance based on your situation. In Germany, you don’t have to repay the mortgage by the end of the mortgage tenure. You can refinance the remaining principal instead.

- Insurances or other schemes on top of the mortgage: Some banks make taking residual debt insurance or term life insurance mandatory. You don’t have to take these insurance or any other schemes. Even if you decide to take one, you don’t necessarily have to take it from the bank. You can find better insurance plans at better rates on comparison portals Check24* and Verivox*.

#5 Finalize the bank and submit all the required documents

Once you have found the best mortgage offer, finalise it. You must submit all the required documents to the bank.

#6 Mortgage contract

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

The bank will evaluate all the documents and the property. They may even send a property evaluator to inspect the property. If everything is fine, the bank will prepare the mortgage contract.

You should proofread the contract to check if everything looks right. If yes, then you are good to sign it.

💡TIP: We recommend signing the mortgage contract a week before signing the purchase contract (Kaufvertrag).

As per German law, you get 14 days to cancel the mortgage contract without giving any reason. It is called “Widerrufsrecht” in German.

So, if something goes wrong and you don’t buy the property, you can cancel the mortgage contract without penalty. The 14-day period includes weekends and public holidays. So, don’t confuse it with business days.

Things to keep in mind while contacting banks and brokers to get a loan offer

- Wait till the bank approves the mortgage offer. Mortgage brokers can present you with different mortgage options. But these mortgage offers are tentative. Mortgage brokers must send your profile to the banks for approval. Thus, the mortgage terms may change until you have approval from the bank. In the worst-case scenario, a bank may reject your home loan application even if the broker thought you were eligible.

- Kredit Anfrage vs Konditionen Anfrage. Submitting a loan request (Kredit Anfrage) affects your SCHUFA score. But, requesting mortgage conditions (Konditionen Anfrage) doesn’t. It’s a small thing, but it has a significant impact. Thus, confirm with your bank that the request should not affect your SCHUFA score.

Understanding important German mortgage terms and conditions

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

There are four essential mortgage conditions you should be aware of.

- The mortgage interest rate offered by the bank.

- Fixed interest rate vs variable interest rate

- How does the bank calculate the mortgage interest?

- Possibility of special repayments (Sondertilgung).

The mortgage rate offered by the bank in Germany

It’s a no-brainer that the lower the mortgage interest, the better. However, you should not decide solely based on the interest rate.

You must also consider other factors, such as monthly installments, how banks calculate interest, etc. Additionally, you should check the “effective interest rate.”

The effective interest rate is the sum of the interest rate and bank costs (such as processing fees, commissions, etc.). For example, if your interest rate is 3%, after adding the bank costs, the effective interest rate is 3.1%.

Fixed interest rate vs variable interest rate

A fixed interest rate means your interest rate won’t change during the loan term. In a variable interest rate, your interest changes with the market during the loan term.

Usually, a fixed interest rate is better in most cases. However, if you think the interest rates will fall in the future, variable interest rates are advantageous.

Your interest rate also varies with the fixed interest period. The longer the fixed interest period, the higher the interest rate.

During a low-interest period, you should prefer a fixed interest rate and get it fixed for at least 10 years.

Possibility of special repayments (Sondertilgung) in your mortgage contract

- Special repayment (Sondertilgung) is an option to repay a certain amount once every year in addition to monthly installments.

- The amount you repay is deducted directly from your loan’s Principal. Hence, you can use it to repay your loan early and pay less interest.

- Banks define Sondertigung as a percentage of the loan amount. Normally, it’s 3% or 5%.

For example, if the Sondertilung is 5% and your loan amount is 100k €. Then, you can repay up to 5k€ once every year without any penalty.

💡 TIP: It’s recommended having Sondertilgung as an option in your mortgage contract.

Having the Sondertilung option in your contract does not imply that you must pay it yearly. You can decide to pay 2k, 4k, or nothing.

How does the bank calculate the mortgage interest?

The borrowing rate offered by various banks can be the same, but how banks calculate interest may vary.

How banks calculate the interest rate can significantly affect the total interest you pay over the loan tenure. There are two ways banks in Germany calculate the mortgage interest.

- Interest on the principal left

- Fixed interest throughout the loan term

Calculate the interest rate on the principal left.

The principal reduces over time as you repay the mortgage. Thus, the interest part of the monthly installment also reduces with time.

For example, you took a mortgage of 100k€ at a 1% borrowing rate per annum. You chose a monthly installment of 1000 €, consisting of a principal (916 €) and interest (84 €).

You’ll pay a total interest of 4457 € to repay the entire mortgage. The image shows the borrower’s repayment plan.

Fixed interest throughout the loan term (also called an annuity loan)

In this case, the bank calculates the interest on the issued loan (i.e., $100k) and not the principal left. This means that the interest portion of the monthly installment is the same throughout the loan term (i.e., $84).

In this scenario, you’ll pay TWICE the interest you paid in the previous case.

The borrower will take approximately nine years (100k / (916*12)) to repay the mortgage. Thus, interest paid in 9 years will be 9072 € (9*12*84). It’s twice the interest paid in the previous scenario.

Thus, always check how the bank is calculating the interest.

Financial terms used in a mortgage contract

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

Darlehensbetrag (Loan amount or Principle)

It means how much credit you want to take from the bank. If you take less than the property’s purchase price, you must prove that you can finance the remaining amount.

You can even take a higher loan. For example, a loan to renovate the property. You can also check home renovation loan offers on Finanzcheck*, Tarifcheck*, and Verivox* online brokers.

Nebenkosten (Property purchase cost)

Nebenkosten is the amount that covers home-buying costs in Germany. It’s the sum you need on top of the property’s purchase price.

Nebenkosten is around 7% to 12% of the real estate purchase price.

So, for example, you want to buy a property whose sale price is €250k. Then, you need to bring 17.5k (7% of 250k) to 30k (12% of 250k) from your pocket.

Thus, the total cost to buy the apartment is 250k € + (17.7k to 30k) €.

Nebenkosten percentage depends on two factors:

- Land transfer tax in the province where you buy a property

- Real estate agent commission.

Different provinces in Germany have different land transfer taxes. For example, as of 2024, the land transfer tax in Bayern is 3.5% and 5% in Baden-Württemberg.

Different real estate agents charge different commissions. You’ll save some money if you don’t buy the property via a real estate agent.

Tilgung (Monthly installment)

Tilgung is your monthly installment. You don’t have to repay your mortgage within the loan term. You can refinance the remaining mortgage at the end of the loan term.

Banks ask you how much Tilgung/monthly rate you prefer. You can answer it in 2 ways.

- You can tell them the amount in euros. For example, 600 € every month.

- You can tell them in percentages. For example, you want to repay 2% of the mortgage principal annually.

Sollzinssatz (Interest Rate)

Sollzinssatz means the interest rate. It is the interest that you will pay on your loan. The lower, the better.

Dauer der Sollzinsbindung (Mortgage period)

It means the mortgage period (10, 15, 20 years).

Usually, the longer the mortgage period, the higher the interest rates. So, you need to strike a balance between the mortgage period, the monthly installment, and the interest rate.

Sondertilgung (Special repayment)

Sondertilgung is an optional payment once every year on top of monthly installments.

Restschuld (Pending debt)

It is the amount left after your mortgage term ends. You can refinance the Restschuld with the same or different bank.

Kredit Anfrage (Request a loan)

It means to request a loan from a bank. This request affects your SCHUFA score. Hence, you should request loan conditions (Konditionen Anfrage) instead.

You can also tell the bank consultant that the loan inquiry shouldn’t affect your SCHUFA score.

Konditionen Anfrage (Request for loan conditions)

It is the request to know the loan conditions a bank offers. It doesn’t affect your SCHUFA score.

FAQ

Is it possible to get a loan that is more than the property’s purchase price?

Yes, you can get a higher loan than the property’s purchase price. The typical scenario is getting a renovation and a mortgage loan.

Can you repay the mortgage before the mortgage tenure ends?

Yes, you can repay the mortgage before its tenure ends. But you may have to pay a penalty. Whether you must pay a penalty depends on the mortgage terms.

You can repay the mortgage after three years penalty-free if you live on the property. And after ten years, if you don’t.