Explore Rürup pension insurance in Germany. Understand the unique features, tax advantages, and eligibility criteria of the Rürup pension scheme. Whether you’re self-employed or looking for tax-efficient retirement planning, our guide covers the intricacies of the German pension system.

Key Takeaways

- Rürup pension (basic pension) is a private pension subsidized by the state.

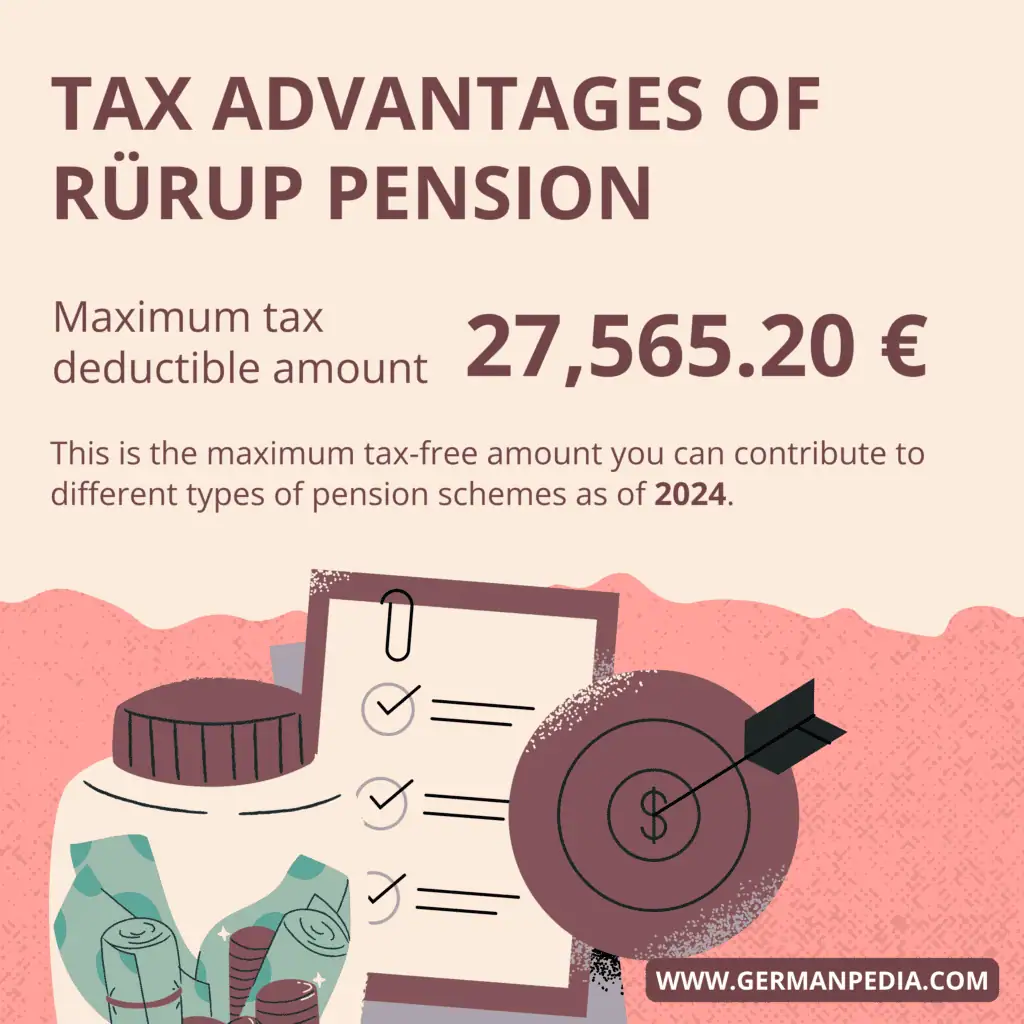

- The maximum amount you can deduct from taxes as pension expenses is increased from 26,528 € in 2023 to 27,565.20 € in 2024.

- As there is no maximum limit on the Rürup pension contributions, you can contribute the maximum tax-deductible amount (i.e., 27,565.2 €) to save taxes.

- You cannot cancel a Rürup contract. You can only reduce or stop paying the contributions.

- Creditors cannot access the capital saved under Rürup pension in bankruptcy. Hence, your money is safe.

This is how you do it

- Employees are part of compulsory statutory pension insurance. Hence, Rürup’s pension plan on top is not so attractive. It’s better to invest in ETFs tracking broad market indices.

- You can open a free depot account with Scalable Capital* or Finanzen.net Zero and start investing.

- Rürup contract is worth considering for self-employed and freelancers who don’t have any other pension plan in Germany.

- You can compare different Rürup plans on the comparison portals Check24*.

Table of contents

How does the Rürup pension work in Germany?

Rürup pension is also called the basic pension. Rürup pension is a form of private pension that offers tax advantages.

Rürup pension is useful for self-employed or freelancers in Germany who don’t contribute to statutory pension insurance. You can compare the Rürup pension with statutory pension insurance or a company pension plan.

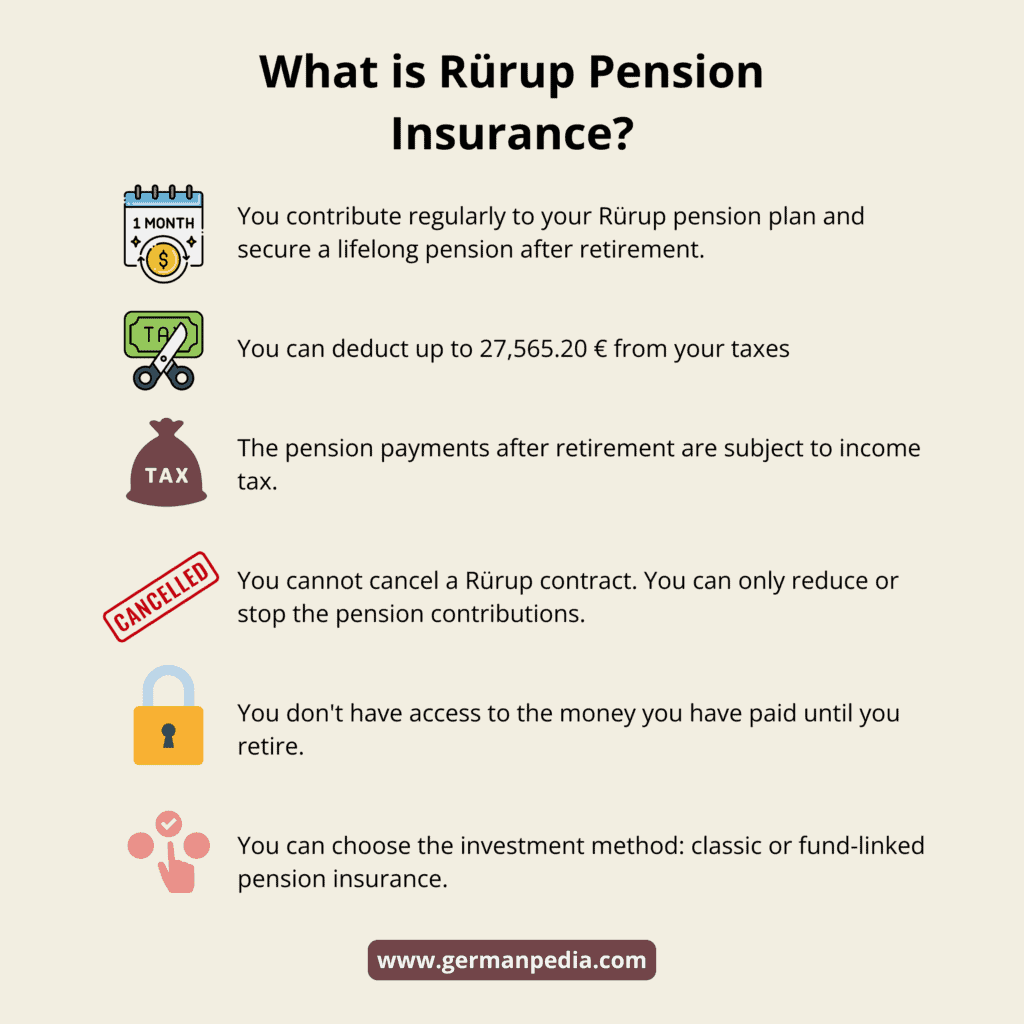

Here is how the rürup pension plan works.

- You contribute regularly to your Rürup pension plan and secure a lifelong pension after retirement.

- The contributions to the pension insurance are tax deductible. You can deduct up to 27,565.20 € (as of 2024) from your taxes as special expenses (retirement savings expenses).

- The pension payments after retirement are subject to income tax.

- You cannot cancel a Rürup contract. You can only reduce or stop the pension contributions. But you must continue paying the annual Rürup contract fee.

- You don’t have access to the money you have paid until you retire.

- You can choose the investment method: classic or fund-linked pension insurance.

As of 2021, there are around 2.5 million Rürup contracts. You can compare different Rürup plans on the comparison portal Check24*.

NOTE: The maximum tax-deductible amount (27,565.2 € as of 2024) includes the contributions to all type of pension insurance. More on this later in this guide.

Is Rürup pension (Basic Pension) worth it?

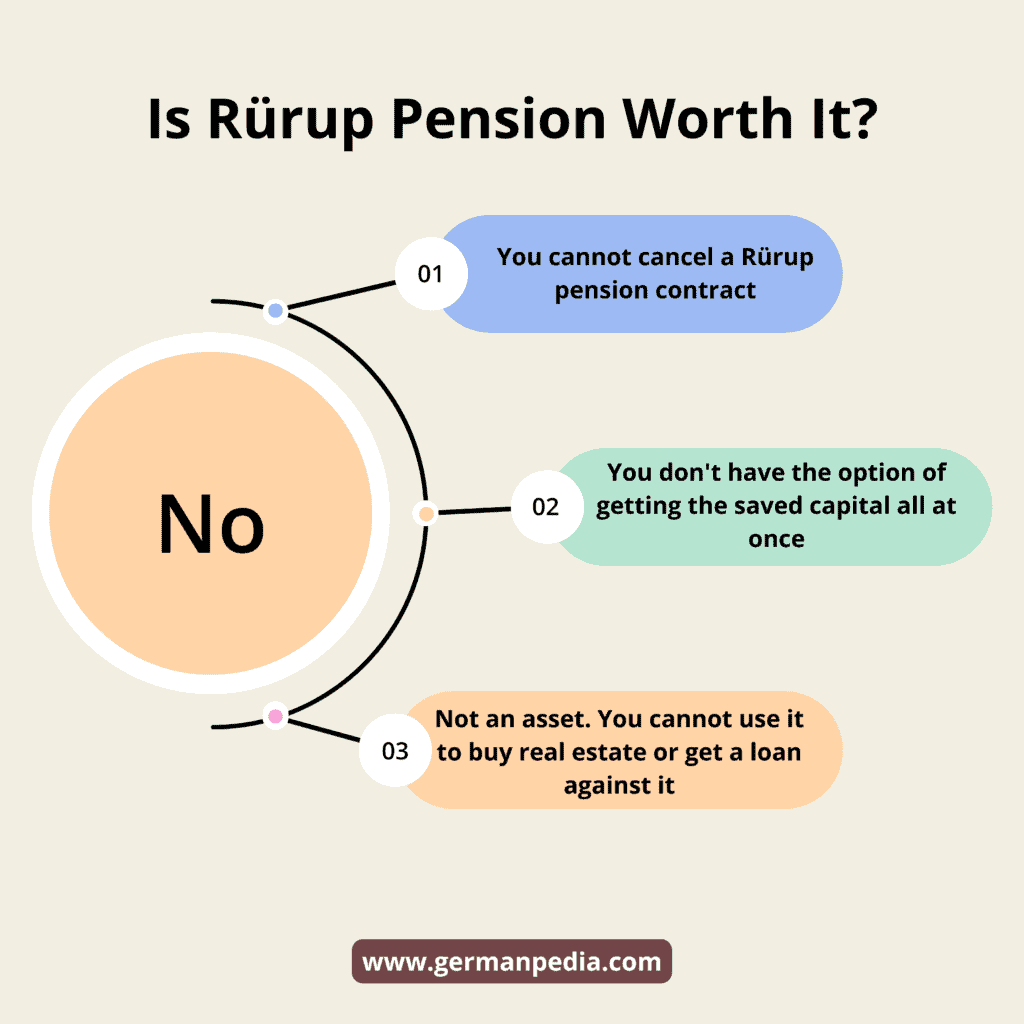

For most people, Rürup pension is not worth it for the following reasons.

- You cannot cancel a Rürup pension contract. You can reduce the contribution or stop paying them. But you must continue to pay the administration costs from your contract balance every year until you retire.

- In Rürup pension, you don’t have the option of getting the saved capital all at once. It will be paid as a monthly pension after you retire.

- Rürup pension is not considered as an asset. Hence, you cannot use it to buy real estate or get a loan against it.

- If you die during the savings phase, your dependant survivors will not get any money from the Rürup pension scheme. However, many Rürup pension providers now offer survivor protection.

For whom does the Rürup pension insurance make sense?

Unfortunately, the German pension system doesn’t offer attractive pension schemes. The same goes for the Rürup pension.

However, Rürup pension insurance might interest people in one of the following two categories.

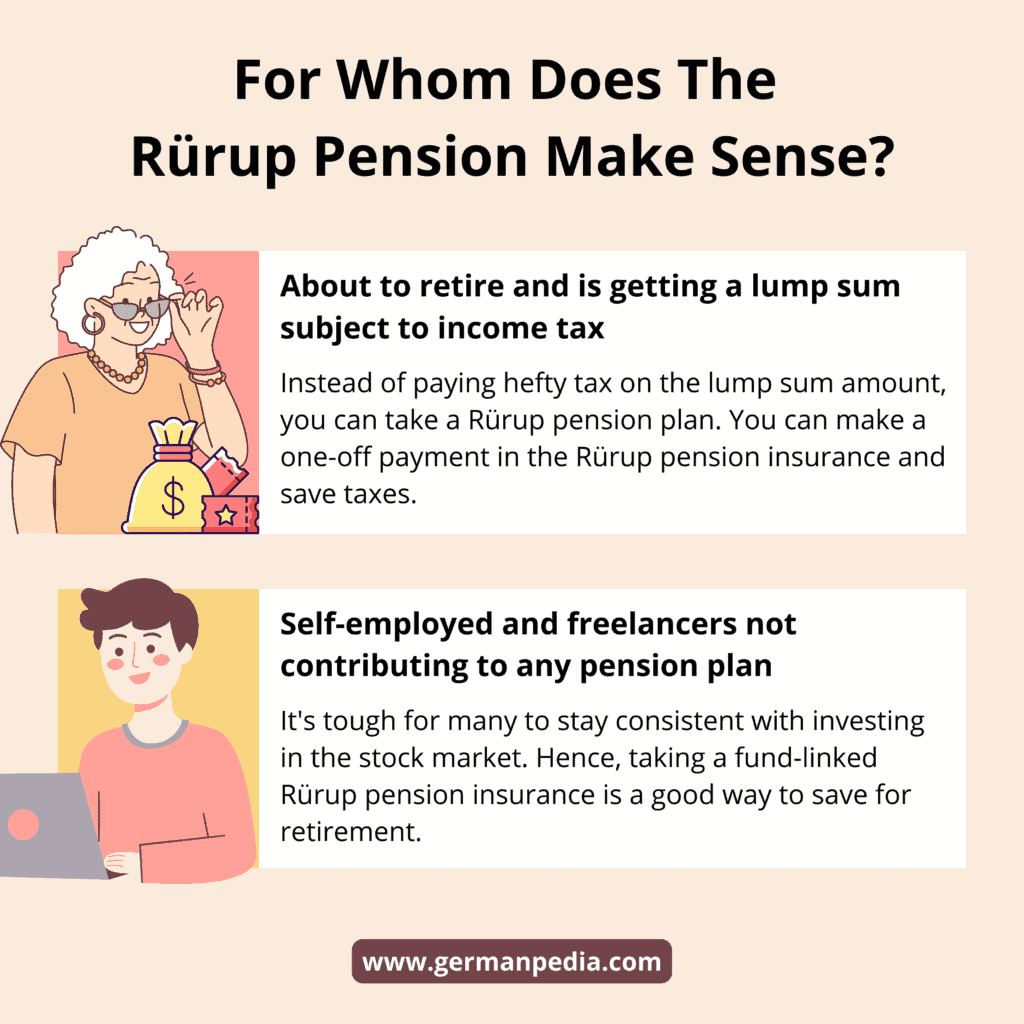

About to retire and is getting a lump sum subject to income tax

Rürup pension insurance might be interesting for someone

- about to retire

- and is getting a lump sum subject to income tax.

Instead of paying hefty tax on the lump sum amount, you can take a Rürup pension plan. You can make a one-off payment in the Rürup pension insurance and save taxes.

As you are about to retire, investing the lump sum in the stock market is not the best idea. So, you save tax and secure a lifelong pension after retirement by taking Rürup pension insurance.

Of course, you must pay tax on your pension after retirement. However, the tax is usually lower as the taxable income after retirement is lower.

Moreover, not 100% of the amount saved in the Rürup pension is taxable. If you retire in 2024, only 84% of the saved amount is taxable.

Thus, you pay no taxes on 16% of the total savings.

However, the percentage of the taxable amount increases by 0.5% every year [1]. So, by 2058, 100% of the saved amount will be taxable.

This means that young people who retire after 2058 will pay tax on all their savings in the Rürup pension plan.

Self-employed and freelancers not contributing to any pension plan

Rürup pension plan is also for self-employed and freelancers who don’t contribute to any pension plan.

Many find it challenging to stay consistent when investing in the stock market. Hence, taking fund-linked Rürup pension insurance is a good way to save for retirement.

You can compare different Rürup plans on Check24*.

Compare Rürup Pension Plans

- Compare offers and prices.

- Comparison calculator to find suitable Rürup pension policies.

- Compare the insurance providers and their ratings.

For whom does the Rürup pension plan NOT make sense?

Rürup pension is not for young students and entrepreneurs for the following reasons.

- You’ll retire after 2058; hence, you pay tax on all your savings under the rürup pension scheme.

- You cannot cancel the rürup contract. Thus, you’ll be stuck with it even if your life situation changes. For example, you quit your business and get a job.

It’s better to invest in ETFs tracking broad market indices instead.

Alternatives to Rürup pension in Germany

You should be in control of your money and future. Hence, investing in ETFs tracking broad market indices is one alternative to the Rürup pension scheme.

You can open a free depot account with Scalable Capital* or Finanzen.net Zero* and start investing.

Another alternative is to invest in real estate. You can rent the property and secure a monthly income source.

Moreover, you can sell your property after retirement to get a lump sum. You can learn more about how to buy a house in Germany in our guide.

Advantages of a Rürup pension insurance

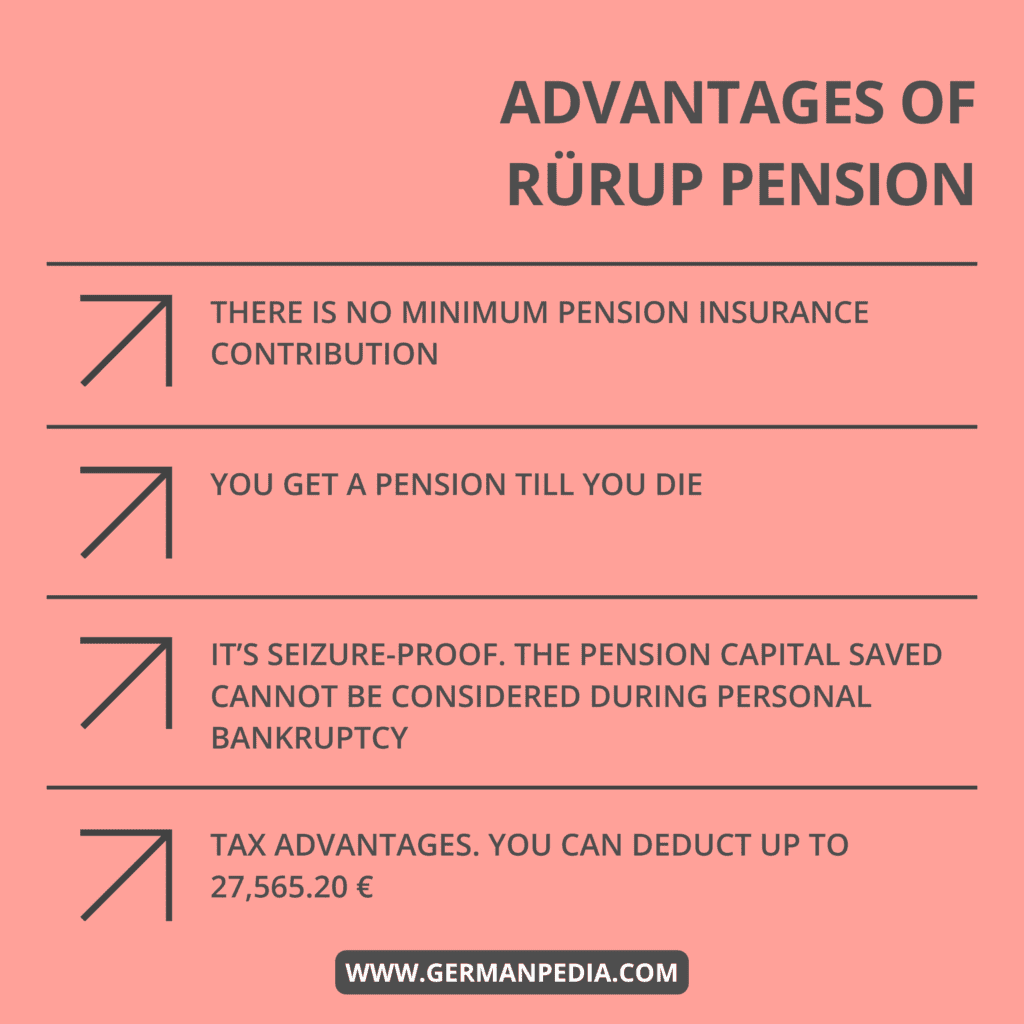

- There is no minimum pension insurance contribution. You can choose any amount you want to contribute to the Rürup pension.

- You get a pension till you die under the Rürup pension scheme.

- Rürup pension plan is seizure-proof. This means that the pension capital saved under the Rürup pension cannot be considered during personal bankruptcy or when applying for unemployment benefit II. In other words, creditors cannot access the Rürup pension in case of personal bankruptcy. On the other hand, investments like ETFs must be diluted in case of bankruptcy.

- Rürup pension offers tax advantages. You can deduct up to 27,565.20 € (as of 2024) from your taxes as retirement savings expenses. Married couples can deduct up to 55,130.4 € from their taxes. However, you pay taxes on the pension you receive after retirement.

You can compare different Rürup plans on Check24*.

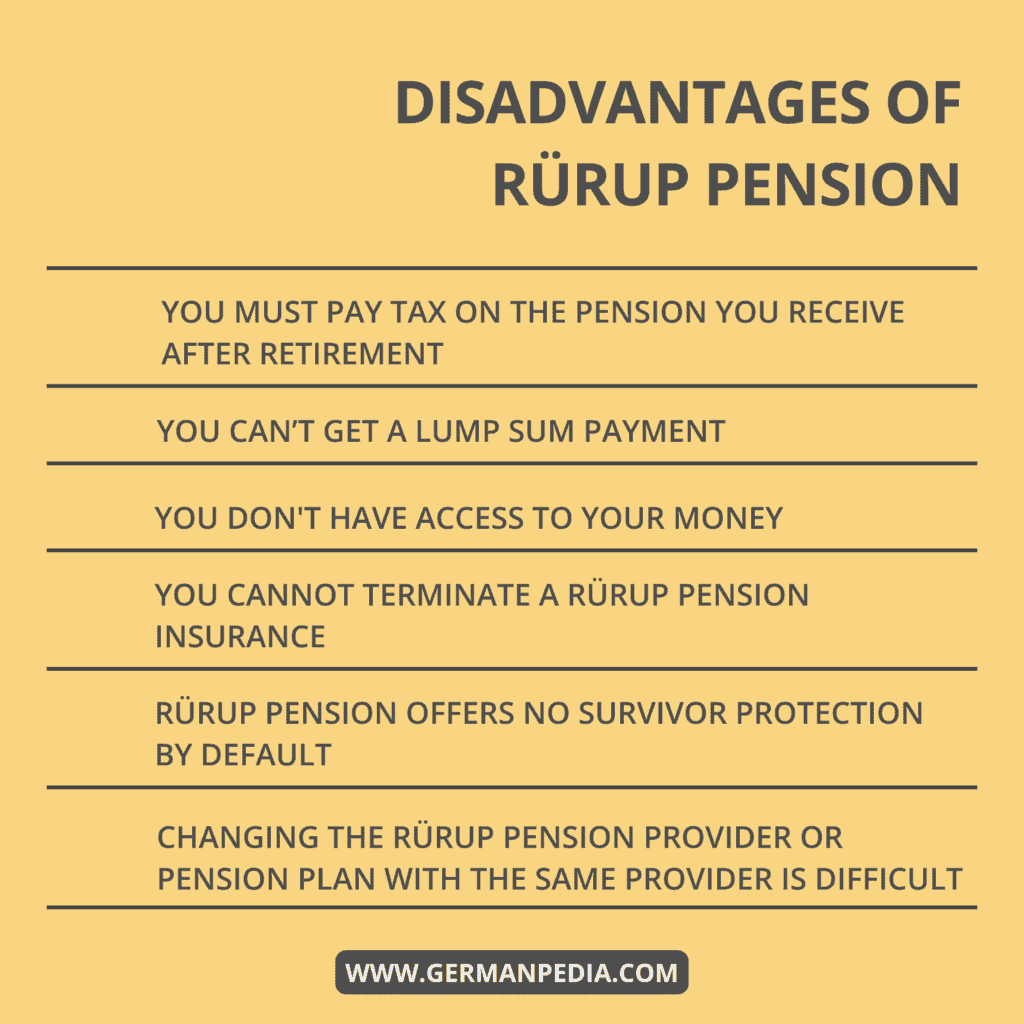

Disadvantages of Rürup pension in Germany

- Changing the Rürup pension provider or pension plan with the same provider is difficult. The pension provider may refuse to change the Rürup pension plan or charge fees to make the change.

- In Rürup pension plan, you don’t have access to your money. You start getting a monthly pension when you are 62.

- You cannot terminate Rürup pension insurance. You can only reduce or stop paying the contributions. But you must continue paying the yearly fee until retirement.

- Rürup pension doesn’t offer survivor protection by default. In the event of death, the saved capital goes to the pension provider. However, some providers offer survivor protection. Hence, check the terms and conditions of the pension contract carefully.

- The Rürup pension is paid out like a monthly pension throughout life after retirement. You don’t have the option to get a lump sum payment.

- You must pay tax on the pension you receive after retirement. Hence, this offsets the tax benefits you enjoyed during the savings phase.

Different types of Rürup pension schemes

There are three types of Rürup pension plans in Germany.

- Classic basic pension

- Immediate pension

- Fund-linked basic pension and Fund savings plan

Classic basic pension with or without survivor protection

- Under a classic basic pension plan, you pay monthly pension contributions.

- You set a guaranteed pension when the contract is concluded. However, it’s very low due to low-interest rates.

- By default, there is no survivor protection. It means no payout to the surviving relatives in the event of the insured person’s death. Thus, you should ensure that your Rürup pension contract offers survivor protection.

Immediate pension

- The insured person makes a one-off payment to the Rürup pension. Hence saving taxes.

- In return, the Rürup pension pays you a lifelong pension after retirement.

Fund-linked basic pension

- You pay a monthly pension contribution. Unlike the classic pension, your pension contributions are invested in the stock market and ETFs. Thus, find-linked pension offers higher return and risk.

- The insurance provider guarantees a factor for determining the lifelong pension after retirement. This factor tells how much pension you’ll get for every 10,000€ pension capital saved. The insurer determines the factor at the time of pension contract conclusion.

- At the beginning of retirement, the insurer determines the total value of the invested capital. The insurer uses the capital saved and the factor to determine your pension.

- The actual value of the invested capital can only be known at the time of retirement. Thus, the pension amount can only be determined at retirement.

- The future pension amount depends on the stock market performance.

Many insurers offer additional plans on top of Rürup pension insurance. The most common is the occupational disability insurance.

Occupation disability insurance kicks in if you cannot work due to an occupational disability. The insurance pays your future Rürup contributions.

NOTE: As per the association of insured persons (Bund der Versicherten), you should never link occupational disability insurance with Rürup pension insurance. Always take occupational disability insurance as a separate module.

Rürup pension for the self-employed and freelancers

Unlike employed people, self-employed and freelancers must care for their pension provisions.

You should either contribute to statutory pension insurance, take a private pension plan, or open an ETF savings account. But you must build your private provision for old age.

Of all the pension plans available in the German pension system, Rürup is the best for self-employed and freelancers for the following reasons.

- There is no limit to Rürup pension contributions. Thus, you can contribute the maximum tax-deductible amount (i.e., 27,565.20 € as of 2024) to the Rürup pension contract. Hence saving taxes.

- Like private pension insurance, fund-linked Rürup pension offers better returns with high risks. But you enjoy tax benefits in the Rürup pension. There are no tax advantages in the private pension plan.

Of course, opening an ETF savings plan is the best option for anyone to save for their old age. However, very few people have consistently invested for decades in the stock market.

Thus, consider contributing to at least one pension plan of your choice. And top it with an ETF savings plan or/and a real estate investment to secure your older self.

Compare Rürup Pension Plans

- Compare offers and prices.

- Comparison calculator to find suitable Rürup pension policies.

- Compare the insurance providers and their ratings.

Tax advantage in a Rürup pension scheme

The maximum tax-free amount you can contribute to different types of pension schemes is 27,565.20 € (as of 2024). Thus, the self-employed person who does not pay into German pension insurance can contribute the maximum tax-free amount (27,565.20 €) to the Rürup contract.

NOTE: Contribution to the public pension plan reduces the tax-free amount for the Rürup pension.

For example, you pay 10k € in the state pension. Then, the maximum tax-free amount left for Rürup pension is 17,565.2 € (27,565.20 – 10,000).

How high are the taxes on the Rürup pension after retirement?

The taxation on the pension from the Rürup insurance is based on the personal income tax rate. But how much pension you must tax depends on the year you retire.

If you retire in 2024, 83% of Rürup pensions will be taxed. Hence, you will receive 17% of the money tax-free.

However, the taxed portion for Rürup pensions will rise by 0.5% every year [2]. So, the entire Rürup pension is subject to tax if you retire in 2058 or later.

Percentage of rürup savings to be taxed by year

| Retirement year | Percentage of Rürup savings to be taxed | Tax-free share (in %) |

|---|---|---|

| 2023 | 82.5 | 17.5 |

| 2024 | 83 | 17 |

| 2025 | 83.5 | 16.5 |

| 2026 | 84 | 16 |

| 2027 | 84.5 | 15.5 |

| 2028 | 85 | 15 |

| 2038 | 90 | 10 |

| 2048 | 95 | 5 |

| 2058 | 100 | 0 |

Source: EStG Paragraph 22

How much of a monthly pension can you expect in the Rürup pension scheme after retirement?

The pension you’ll get from Rürup pension insurance depends on

- Your monthly contributions or the one-off payment.

- How long have you been paying into the pension insurance?

- Type of Rürup contract you signed.

- Performance of the fund (stock market and ETF) in case of fund-linked Rürup contract.

- How much tax advantage do you enjoy during the savings phase?

Thus, it’s difficult to say how much monthly pension you’ll get in the Rürup pension scheme.

References

- https://www.finanztip.de/ruerup-rente-basisrente/

- https://www.weltsparen.de/altersvorsorge/ruerup-rente/vorteile-nachteile/

- https://www.allianz.de/vorsorge/ruerup-rente/#basissofortrente-so-funktionierts

- https://www.weltsparen.de/altersvorsorge/ruerup-rente/

- https://www.sparkasse.de/pk/produkte/altersvorsorge/ruerup-rente.html

- https://www.gesetze-im-internet.de/estg/__22.html