Reviewed by experts

Reviewed by:

Key takeaways

- Private health insurance is a cheaper and better option for high earners only.

- Unlike public health insurance, private health insurance costs don’t depend on your income.

- Private health insurance premiums rose 3.2% per annum between 2004 and 2024. On the other hand, public health insurance costs rose 3.3% per annum during the same time.

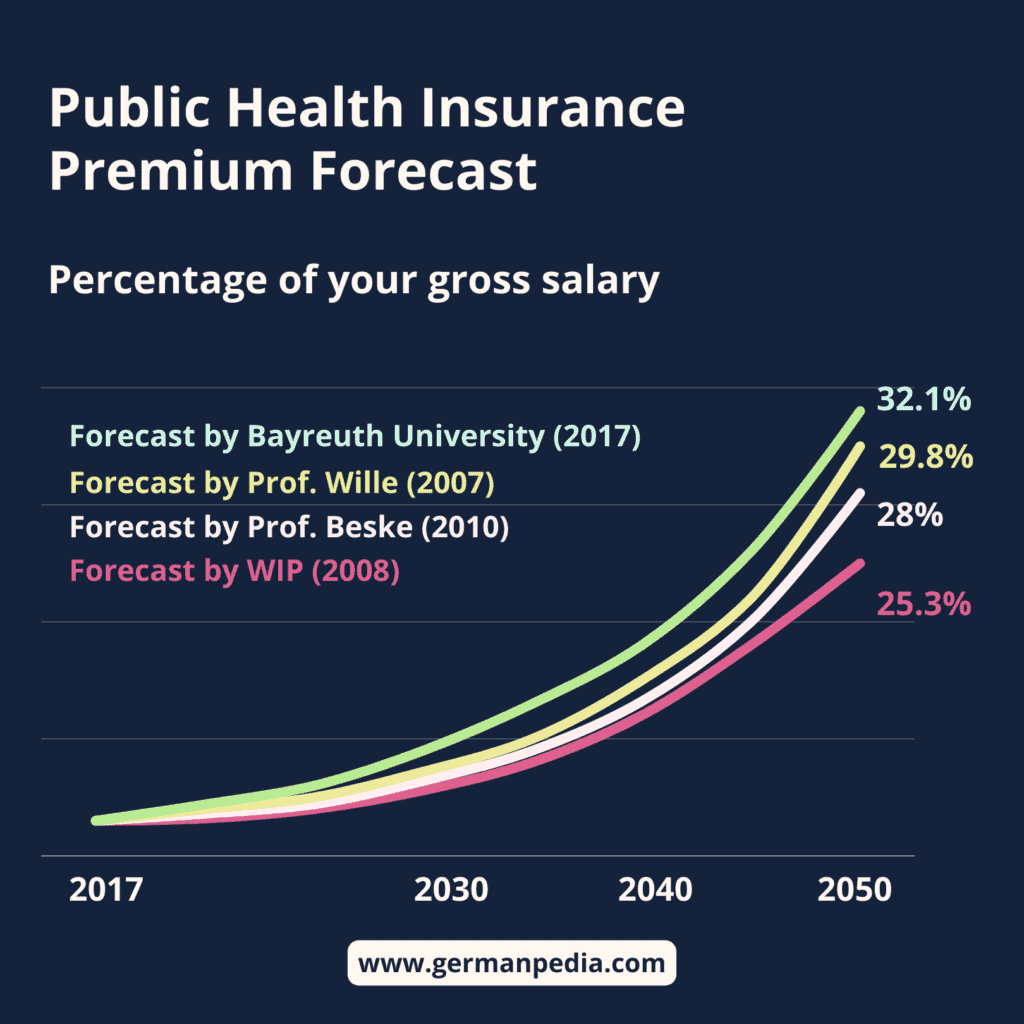

- Experts predict you’ll pay between 25% and 32% of your gross salary in public health insurance by 2050.

This is how you do it

- Educate yourself about the private health insurance system in Germany.

- Use our “Health Insurance Finder” tool to see which health insurance makes sense for you and why.

- Consult a fee-based advisor or an insurance broker for personalized advice. You can use this form to ask your query to the insurance brokers we recommend for free.

Table of Contents

Private health insurance offers better coverage than public health insurance, yet it’s cheaper. You may ask how that is possible.

Note that private health insurance is cheaper for high earners only. Low earners cannot afford private health insurance in Germany.

Here are the reasons why private insurance is cheaper for high earners.

- Every insured member of private health insurance pays a contribution

- Private health insurance companies accept only healthy individuals

- Private health insurance providers save part of the monthly contribution to keep the premium stable in old age.

- Only high-paid individuals can join the private healthcare system.

- The increasing aging population in Germany

Let’s understand each point in detail.

#1 Every insured member of private health insurance pays a contribution

Private health insurance does not offer free coverage for your non-working partner or children. Everyone must make contributions to get services.

On the other hand, with statutory health insurance, you can insure your non-working spouse and children for free. The statutory system has 16 million (as of 2023) people insured for free.

However, the public system needs money to run. So, its only option is to collect money from those with income.

The earning population of the public health system must contribute enough to cover

- their medical expenses and

- the medical costs of freely insured members.

Additionally, public health insurance premiums depend on your income. So, the higher you earn, the more the health insurance cost.

On the other hand, with private health insurance, you only pay the premium for yourself. The insurance company calculates the premium based on your

- health condition,

- age, and

- your estimated total medical expenses throughout life.

This makes private health insurance premiums lower than public health insurance premiums for high earners.

#2 Private health insurance companies accept only healthy individuals

Private health providers have the right to choose their customers. So, they accept only healthy and young individuals as their customers.

As you can imagine, young and healthy individuals don’t get sick often. This keeps the expenses of the private health insurance system low.

On the other hand, public health insurance cannot choose their customers. So, unhealthy people who cannot get private insurance must join the public health insurance system.

So, the expenses per insured member of public health insurance are higher than those of private health insurance for similar services. This leads to higher public health insurance premiums than private.

#3 Aging provisions

Medical expenses increase as you age, and Germany has an aging population. So, the medical expenses of the German population are growing.

The two German healthcare systems tackle the aging problem differently. Their approach to solving it significantly affects insurance premiums.

How does the public healthcare system solve the aging problem?

Public health insurance relies on young professionals to pay for the increased medical expenses of retired insurance members. In other words, the current generation pays for the previous generation.

This is why Germany’s aging population threatens the survival of the statutory healthcare system.

There won’t be enough young professionals to pay for the retired. Hence, it’ll lead to unaffordable insurance premiums in the future.

The situation worsens as public health insurance does not have a concept of aging reserves.

How does the private healthcare system solve the aging problem?

In the past, private health insurers also didn’t save for old age. No aging provisions led to unaffordable insurance premiums in old age.

This is why many baby boomers have bad experiences and stories about private health insurance. However, private health insurance companies and the German government learned from their past mistakes.

Since 2000, every private health insurance company has been legally required to save part of the monthly premium. The insurer uses this saved amount to compensate for increased medical costs in your old age. Thus, it keeps the premium stable in old age.

This saving is called aging provisions (Altersrückstellungen in German).

The aging provisions have a successful track record of tackling the challenge of increased medical costs in old age.

Conclusion

Aging reserves make a massive difference in keeping premiums stable in old age. We can learn from the past about how high premiums can rise without an aging reserve.

So, no aging reserve and a decreasing young population mean unaffordable public health insurance premiums in the future.

#4 30% of the people in Germany are 60 or above

Germany has an aging population. 30% of the German population is 60 and above and 45% is 50 and above.

Only 31% of the population is between 25 and 49 [4]. This poses a huge threat to the German economy and to keep the country running.

Many experts forecast that public health insurance contributions will rise from 16.3% of your gross salary (as of 2024) to 30% by 2050.

By 2035, you can expect to pay around 20% of your gross salary as a public insurance premium. This is due to not enough young professionals to pay for the retired.

Private health insurance is also affected by the German aging population. However, it’s creating aging reserves to fight the aging population challenge.

So, for high earners, the insurance premium in the private system is expected to increase at a lower rate than in the public system.

In the past (2004 to 2024), private health insurance costs rose by 3.2%, and public health insurance costs increased by 3.3% [5].

#5 Only high-paid individuals can join the private healthcare system.

To be eligible for private health insurance, you must earn above 69,300 € gross per annum. This limit applies to employed individuals only.

Self-employed and civil servants with lower incomes can also join private health insurance. However, as per experts, private health insurance is not a good option for low earners.

Statistically, high-paid employees are also highly educated and spend more on their health than low-earning employees. Thus, one can deduce that high-earners are healthier than low-earners and, ultimately, less expensive to the health system.

This also supports the private healthcare system in keeping the premiums lower than the public healthcare system.

Public and private health insurance costs in Germany

Public health insurance costs depend on your income. On the other hand, private health insurance costs depend on your age and health.

When comparing public and private insurance costs, we’ll assume you are a high earner. This is because private health insurance makes sense only for high earners.

| Age (Nr. of years after taking private insurance) | Private health insurance | Public health insurance |

| Yearly increase in premium over the past 10 years (2015 to 2025) | 3.9% | 4.1% |

| Yearly increase in premium over the past 20 years (2005 to 2025) | 3.1% | 3.8% |

| Premium of a high-earner, self-employed individual | Premium increases by 3.9% per annum | Premium increases by 4.1% per annum |

| 35 (today) | 800 € (as of 2025) | 1174 € (as of 2025) |

| 45 (after 10 years) | 1172 € | 1754 € |

| 55 (after 20 years) | 1719 € | 2622 € |

| 65 (after 30 years) | 2520 € | 3919 € |

| After Retirement | ||

| 67 | 2320 € (you stop paying the sickness benefits) | 1400 € (if you stay in public insurance throughout your work life) |

| Maximum subsidy from pension insurance | 200 € (approx. as of 2024) | 200 € (approx. as of 2024) |

| Net premium you pay after retirement (67) | 2120 € (2320 – 200) | 1200 € (1370 – 200) |

| Total premium paid in 32 years | 588,000€ | 873,000€ |

As you can see, if you are a high earner, you’ll pay way more in the public system than in private throughout your work life. After retirement, the difference in the premiums is not big.

You can reduce the cost of private health insurance by changing your plan or increasing the deductible. However, you have no way of reducing your public insurance premium.

You should also consider that the public health system is in financial trouble. So, the chances that the German government will reduce or cut the public health insurance subsidy for retirees in the future is high.

Lastly, paying more in the public system doesn’t mean getting better services. On the contrary, good private health insurance plans offer better services than public insurance.

Should high-earners switch to private health insurance in Germany?

Yes, high earners should consider switching to private health insurance. Here are the reasons.

- Private health insurance offers better services at a lower cost to high earners.

- Germany’s aging population is putting a strain on its public healthcare system.

- Public health insurance is continuously reducing its medical coverage and increasing the costs.

- Experts predict that public health insurance in Germany will cost between 25% and 32% of your gross salary by 2050.

However, before you make the switch, you must do the following

- Educate yourself about the private health insurance system in Germany.

- Use our “Health Insurance Finder” tool to see which health insurance makes sense for you and why.

- Consult a fee-based advisor or an insurance broker for personalized advice. You can use the form below to ask your query to the insurance brokers we recommend for free.

Once you have completed all these steps, you can decide.

Consult an health insurance broker

NOTE: Insurance brokers are liable for giving you advice. This means that if you asked for a particular coverage and the insurance policy recommended by them didn’t cover it, they are liable to pay for the damages