Key takeaways

- Publicly insured people can insure their dependents for free in public health insurance if they meet specific criteria.

- Privately insured people can’t get free family insurance for their dependents. They must get a separate private health insurance policy for each family member.

- You can insure your spouse, life partners, children, step-children, and grandchildren for free in family insurance.

This is how you do it

- Check if you and your family member meet the free family health insurance requirements.

- If you meet the conditions, contact your public health insurance provider to insure your dependents.

- You can also take supplementary private health insurance on top of free family insurance. This way, you can access health services that are not part of public health insurance.

- Public health insurers increase their monthly premium every year. You can switch to a cheaper public insurance company if your insurer increases the premium. Use our public health insurance cost calculator to check how much you can save by switching to a cheaper health insurer.

- We find TK the best public health insurance provider for expats. Its website, mobile app, and customer service are in English. You can register with TK online.

The AI overview and answers are as good as the sources it uses.

To ensure you get AI answers from a deeply researched, maintained, and up-to-date source, add GermanPedia to your preferred sources.

Table of Contents

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

What is family insurance (Familienversicherung)?

Having health insurance in Germany is mandatory by law. Thus, you must get health insurance for your spouse and children.

There are two types of health insurance in Germany: public (Gesetzliche Krankenversicherung) and private health insurance (Privat Krankenversicherung).

You can cover your family members under your public health insurance at no cost. In this case, your family members’ health insurance is called family health insurance (Familienversicherung in German). You must meet specific requirements to get free family health insurance (§ 10 SGB V). You’ll learn about them later in this guide.

Best public health insurance in Germany ->

If you have private health insurance, you cannot insure your dependents for free. You must get a separate private health insurance policy for your children and spouse.

Best private health insurance in Germany ->

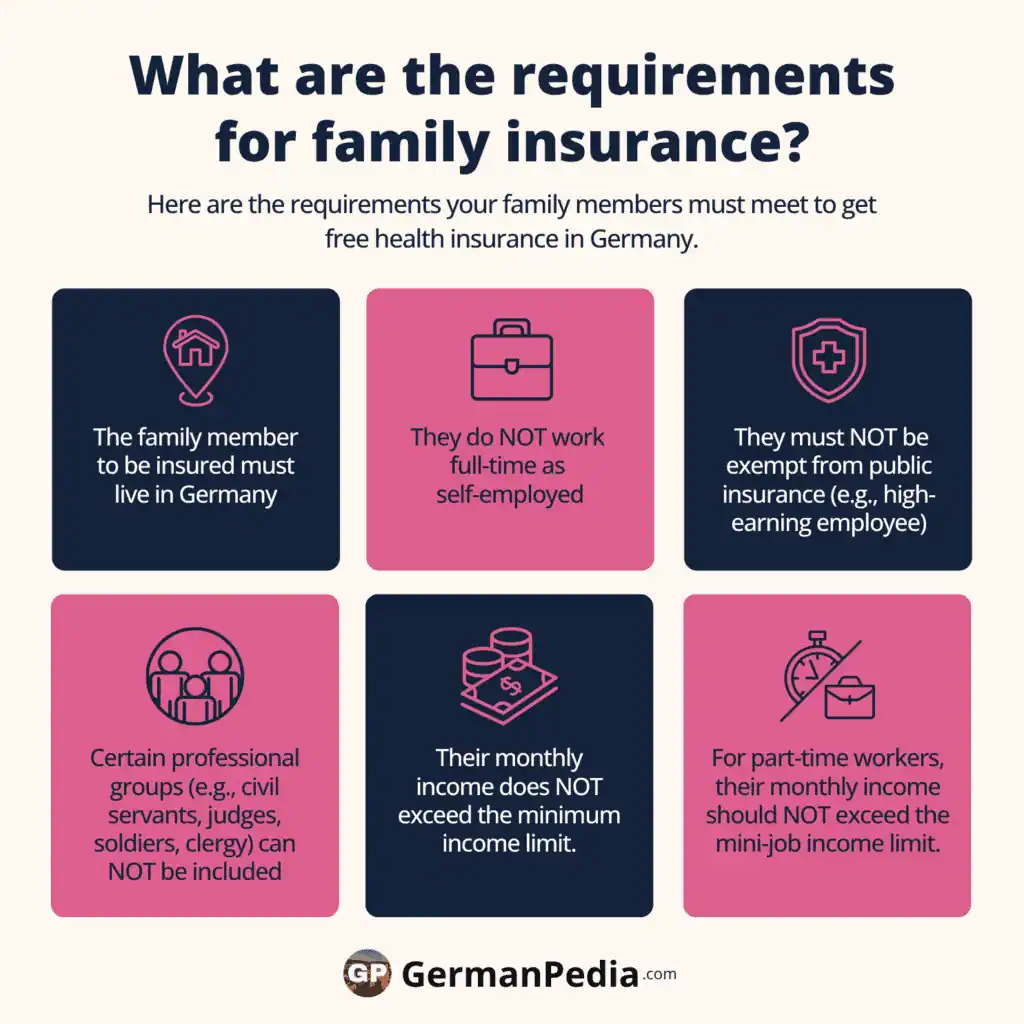

What are the requirements for family insurance?

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

Here are the requirements your family members must meet to get free health insurance in Germany.

- The family member to be insured must live in Germany.

- They do not work full-time as self-employed.

- The family member must not be exempt from public insurance. For example, they are a high-earning employee or civil servant.

- People from certain professional groups, such as civil servants, judges, soldiers, or clergy, cannot be included in family insurance.

- Their monthly income doesn’t exceed the minimum income limit. The income limit is 565€ per month (as of 2026).

- The income shouldn’t exceed the mini-job income limit for family members working part-time. It’s 603 euros per month (as of 2026).

TIP: You can exceed the income limits up to twice a year.

For example, suppose you earned 650€ in August and September each. And for other months, your income was below the income limit.

In this case, you remain insured for free in family health insurance. But if you exceed the income limit by more than twice a year, you must pay for health insurance.

NOTE: Only people part of the public health insurance system can insure their family members for free in family insurance. People with private health insurance must get a private insurance policy for their relatives.

We find TK the best public health insurance provider for expats. It offers its website, mobile app, and customer support in English.

You can register with TK online for free in 2 minutes using our “TK registration service.“

Register with TK

- Biggest public health insurance company in Germany based on number of members.

- Enjoy low premiums

- Get English customer support, website, and mobile app.

- Complete the application process in English.

Who can be insured under family health insurance for free in Germany?

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

The following people can have a free statutory health insurance plan if they meet the requirements (§ 10 SGB V).

- Spouses or life partners

- Both spouses or life partners can remain insured in family insurance until the divorce is finalized, even if they live separately.

- Children can be insured free of charge under public insurance until age 18. It also applies to foster and stepchildren. You can also insure your grandchildren if you primarily support them. You can even insure your child up to 23 for free if they are not employed. And up to 25 if they are in training or studying.

- If the training is interrupted by military service, voluntary service, or work as a development worker, an extension of twelve months is possible.

- Children who cannot look after themselves due to a disability remain insured for free in family insurance for an unlimited period.

NOTE: Suppose you earn more than the income limit as a student or work more than the allowed weekly hours. In this case, you cannot be insured in free family insurance.

Health insurance for students in Germany ->

How do you apply for health insurance for families?

You can insure your spouse and children with your public health insurer as follows.

- Fill out the form “Fragenbogen zur Aufnahme in die Familienversicherung” online on your insurer’s website. Here is the link to the TK form. You must log in to complete the form.

- Submit the form and the requested documents to your public health insurance provider. Typical documents you need are proof of identity (passport or ID), birth certificates for children, a marriage certificate (if applicable), and proof of the family member’s income or proof of no income.

Your public insurer will validate the form and the documents. If your family member meets the requirements, your insurance company will send a confirmation letter and a health insurance card.

What are the income limits to get free family health insurance in Germany?

Children and partners who want free family insurance must have a low income. If your family member’s earnings exceed the applicable limit, they cannot be insured for free in family insurance.

The income limit depends on the type of employment. Here are the income limits for the common professions.

Regular employees

A regular Employee is one who works on a full-time or part-time basis on regularly scheduled shifts of a continuing nature.

The income limit is 565€ per month (as of 2026) if your family member is a regular employee. However, the family member can deduct income-related expenses or the flat rate amount from their gross income. This increases the monthly amount you can earn while staying insured for free.

To calculate the increased amount, add the flat rate for income-related expenses (i.e., 1230€ (as of 2026) per annum) to the minimum income limit.

Suppose your relative has higher income-related expenses than the flat rate. In this case, the income limit can be higher.

Note: As mentioned earlier, income is assessed monthly. You can exceed the monthly limit up to twice per year.

Self-employed

The income limit for self-employed family members is also 565€ per month (as of 2026). However, they should be self-employed part-time to qualify for free family health insurance.

The income used to determine health insurance eligibility is profit from self-employment and not the revenue.

Mini job

Your family members can be insured free of charge if they earn up to 603 euros per month (as of 2026) in a mini-job.

What do German health insurance companies consider as income for family insurance?

Public health insurance providers consider the income from the following sources for family insurance.

- Income from wages and salaries.

- Profits from business.

- Income from renting and leasing.

- Pension payments

- Interest and dividend income from investments.

- Capital gains from selling the investments.

NOTE: You can deduct the saver allowance of 1000€ (from 2024) from income from investments. Thus, up to 1000€ (from 2024) of investment income doesn’t impact the health insurance income limit.

All the tax allowances and flat rates you get in Germany to reduce your tax burden ->

What to do if your income exceeds the income limit later?

You must inform your public health insurance provider once your total income exceeds the income limit.

If you keep the change in income secret, the health insurance company will terminate your free family health insurance retroactively. The insurer may also demand the unpaid contributions retroactively.

When can children not be insured in free family insurance?

In the following cases, children cannot be insured for free in family health insurance.

- Both parents have private health insurance. You must get a separate private health insurance policy for the child. Your child cannot be insured in statutory health insurance.

- Both parents have public health insurance. Your child is automatically insured in your public health insurance or family insurance for free. You can still get full or supplementary private health insurance for your child.

- One parent has private, and the other has public health insurance. You can take private or public health insurance for your child. However, you won’t get FREE family insurance if you meet all of three conditions:

- The parents are married or life partners under the Civil Partnership Act.

- The privately insured parent earns more than the publicly insured parent.

- The total monthly income of the privately insured parent exceeds the income threshold (77,400€ (as of 2026)).

Read our guide on health insurance for children to learn more.

What happens when family insurance ends?

Once your child is older than 25, they must get their own health insurance. Children aged 25 and older have the following options.

- If your child is a student, they can take discounted student health insurance. However, discounted student health insurance is available to students under 30.

- Students aged 30 or older should obtain a regular health insurance policy.

- Children who have full-time jobs must get a regular health insurance policy. They can choose between private or public health insurance depending on their income.

Student health insurance via a public insurer costs around 148€ per month (as of 2026). This includes additional contributions (Zusatzbeitrag) and long-term care insurance (Pflegeversicherung).

Every public health insurer independently sets the additional contribution percentage. The Germany-wide average is 2.9% (as of 2026). TK’s additional contribution is 2.69% (as of 2026)

More topics

- Best private health insurance as per the top rating agencies

- Private health insurance costs in Germany

- Private vs public health insurance

- Private health insurance costs in old age

- Why is private health insurance cheaper than public health insurance?

- Employer’s contribution to private health insurance

- Private health insurance for self-employed

- Health insurance for students

- Health insurance for children

- Healthcare in Germany

- Best public health insurance in Germany

References

- https://www.verbraucherzentrale.de/wissen/gesundheit-pflege/krankenversicherung/familienversicherung-in-der-krankenkasse-wer-kostenlos-mit-rein-kommt-28982

- https://www.tk.de/techniker/leistungen-und-mitgliedschaft/informationen-versicherte/leistungen/entlastung-fuer-familien/versichert-als-familie-in-der-familienversicherung-2000760

- https://www.finanztip.de/gkv/familienversicherung/

- https://www.finanztip.de/krankenversicherung/krankenversicherung-student/

- https://germanpedia.com/german-health-insurance-international-students/

![Number of People Insured in Public Health Insurance in Germany [2000-2025]](https://fefffe12.delivery.rocketcdn.me/wp-content/uploads/2025/03/number-of-people-insured-in-gkv-and-pkv-768x1152.webp)

![Number of People Insured in Public & Private Health Insurance in Germany [2025]](https://fefffe12.delivery.rocketcdn.me/wp-content/uploads/2025/03/number-of-people-insured-in-gkv-and-breakdown-768x1152.webp)