Understand the Riester Pension plan in Germany. Explore this state-subsidized private pension scheme’s benefits, eligibility criteria, and tax advantages. Learn whether Riester pension insurance is the right choice for you.

Key Takeaways

- Riester pension is a private pension scheme with state subsidies.

- You get 175€ basic allowance, 300€ child allowance per child (born after 2008), 185€ child allowance per child (born before 2008), and 200€ joining bonus for young professionals.

- You can deduct up to 2100€ from taxes.

- You can also use Riester pension insurance to buy a house in Germany.

- Riester pension is worth it for low earners with 2 or more kids.

- You can cancel or switch your Riester pension provider anytime. However, you must pay administrative fees.

This is how you do it

- Check if you are eligible to take a Reister pension insurance. Everyone compulsorily insured under a statutory pension can take a Reister pension plan.

- Check which type of Riester pension product fits your needs.

- Before deciding, explore other pension schemes like company pension plans, private pension schemes, Rürup pension, etc.

- Take advice from a fee-based advisor on how to save for your retirement provisions.

- Compare the Riester pension offers on the comparison portal Check24*.

- You can also start saving in an ETF savings plan. It offers better returns and high flexibility. You can open a free depot account with Scalable Capital* and start investing.

Table of Contents

What is Riester pension in Germany?

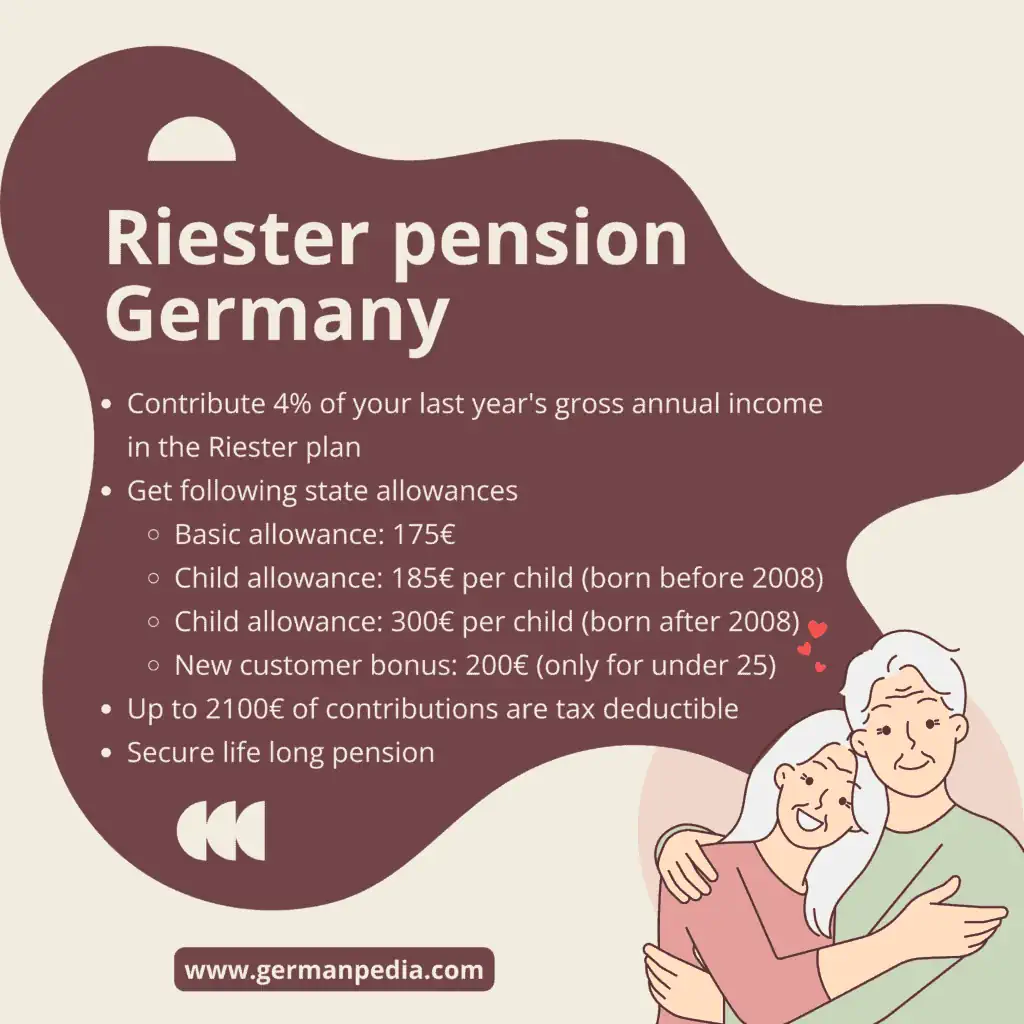

The Riester pension is a form of private pension insurance subsidized by the state. The state subsidies include a basic allowance of 175 € annually (since 2018) and a child allowance of 300 € per child (born after 2008).

German state also offers tax benefits to Riester pension holders. However, the tax office capped the tax-deductible sum to 2100 €.

To be eligible for the state subsidies, you must pay 4 percent of your last year’s gross annual income in the Riester plan.

In the Riester pension plan, you contribute either monthly or yearly. You’ll receive your entire savings plus allowances as a pension after retirement.

You can use the amount saved in the Riester plan in two ways. You can either get a lifelong monthly pension payment in your old age. Or you can use it to buy real estate in Germany.

Riester pension providers guarantee monthly pension after retirement

One of the benefits of the Riester pension is the premium guarantee. Under the premium guarantee, insurers must pay you at least your savings contributions and state allowances.

Insurance providers invest your money in low-risk funds and bonds to offer a pension guarantee. It results in low to no returns on your Riester pension scheme. Thus, making the Riester pension plan unattractive for many.

Administrative fees on the Riester pension plan

You pay a contract and administration fees on your Riester pension insurance. The insurer deducts the fees from your pension contributions. The insurer spreads the Riester contract costs over the first five years.

Here is a breakdown of your total fees for the Reister pension fund.

- The pension contract conclusion costs around 3 to 6% of your contributions. The costs include sales, commission, contract conclusion, etc.

- An additional 1.5 to 3% of your contributions as a deposit administration fee.

- On top of it, you pay fees if you change Riester pension provider.

State allowances and tax benefits in Riester pension scheme

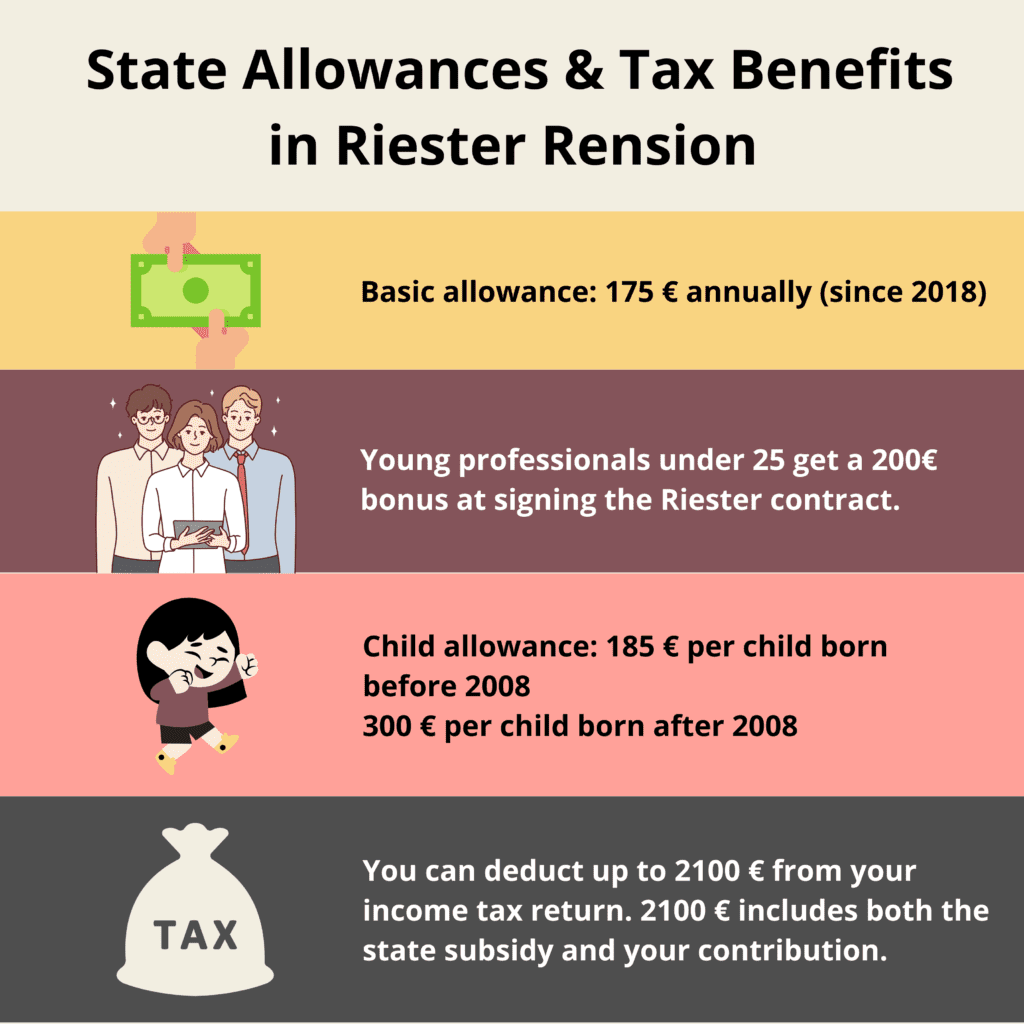

- Basic allowance: 175 € annually (since 2018).

- Child allowance: 185 € per child born by the end of 2007. 300 € per child born after 2008. Child allowance is for every child eligible for child benefit. You’ll receive the child allowance till your child is 25 years old.

- Young professionals under 25 get a 200€ bonus at signing the Riester contract.

- Tax advantage: You can deduct up to 2100 € from your income tax return. 2100 € includes both the state subsidy and your contribution.

You must contribute at least 60€ annually to your Riester contract. But you must contribute at least 4% of your gross annual income from the last year to enjoy the Riester pension allowances.

For example, suppose you have an annual gross income of 50,000 €. You must contribute at least 2000 € (4% of 50k) in the Riester pension insurance. 2000€ includes the state subsidy and allowances.

The state subsidy is 175 € for single individuals without kids. Hence, you contribute 1825 € out of 2000 € from your pocket.

Is Riester pension insurance worth it?

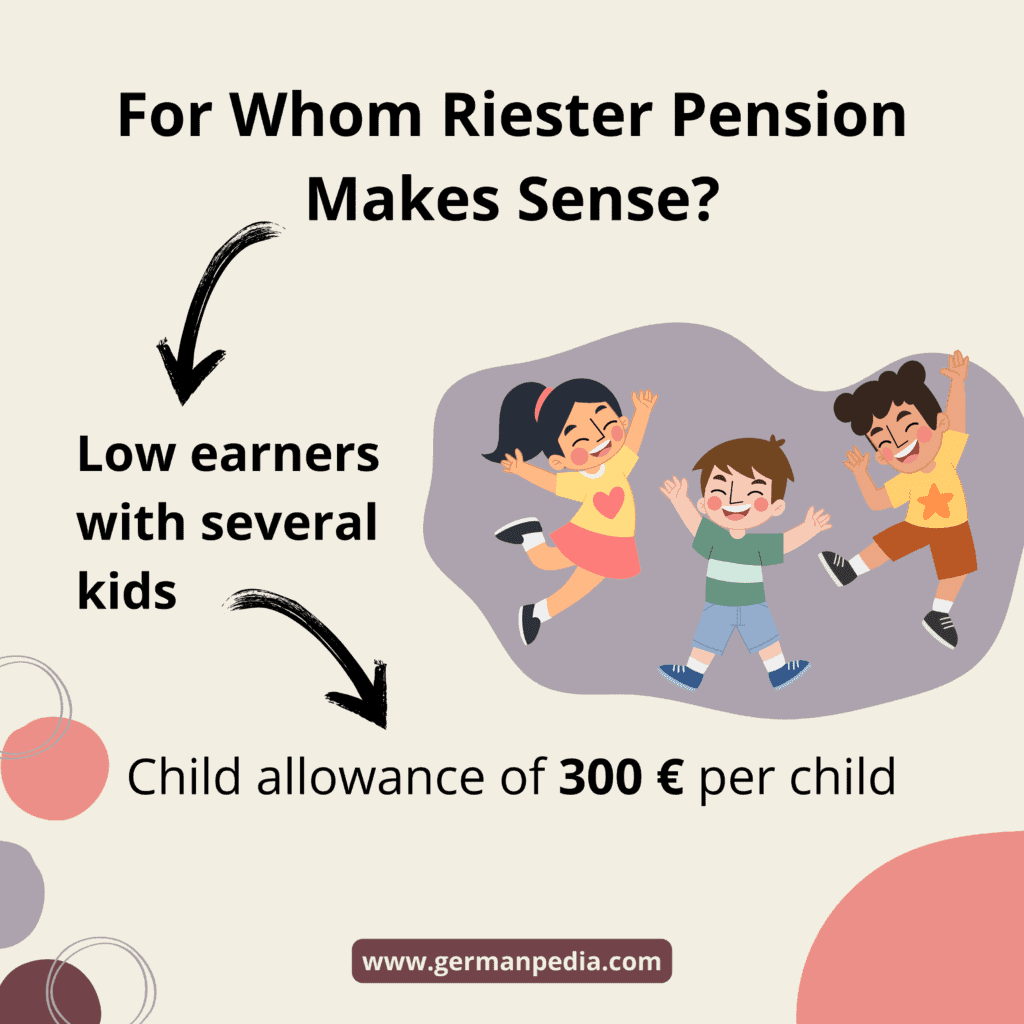

Riester pension insurance is worth it for low earners with several kids. However, it’s not worth it for high earners or people without children.

Here is why.

Riester pension for low earners with several kids

Of all the pension schemes in the German pension system, the Riester pension is worth it for low earners with several kids.

Riester pension insurance is worthwhile for families with two or more kids as you get a child allowance of 300 € per child.

The table below shows the total state subsidies and tax benefits in different scenarios.

| Gross annual income | Kids | State allowances | Minimum contribution (4% of the gross income = 1200€)Your share | Maximum tax-deductible contribution = 2100€ Your share |

|---|---|---|---|---|

| 30,000 € | 0 | 175 € | 1200 – 175 = 1,025 € | 2100 – 175 = 1,925 € |

| 30,000 € | 1 | 475 €(175 + 300) | 1200 – 475 = 725 € | 2100 – 475 = 1,625 € |

| 30,000 € | 2 | 775 €(175 + (300*2)) | 1200 – 775 = 425 € | 2100 – 775 = 1,325 € |

| 30,000 € | 3 | 1075 €(175 + (300*3)) | 1200 – 1075 = 125 € | 2100 – 1075 = 1,025 € |

As you can see, low-earning families with three kids have to pay 125 € only to contribute 1200 € to their Riester pension fund. Moreover, they can deduct 125 € as a special expense from their annual income tax return.

It doesn’t seem like a big amount. But you can save much money with minimal contributions over time.

In this example, a family with three kids will get 32,250 € (1075*30) over 30 years in state funding. To get the state allowance, the family has to contribute only 3750 € (125*30) from their pocket.

As you can see, the state allowance is almost nine times the family’s own capital.

You can compare Riester pension plans on the comparison portal Check24*.

Compare Riester Pension Plans

- Compare offers and prices.

- Comparison calculator to find suitable Riester pension policies.

- Compare the insurance providers and their ratings.

Riester pension for high earners

Riester pension insurance doesn’t make sense for high earners. Here, you can see why.

The table below shows the return on Reister pension schemes in Germany.

| Example case(gross income) | Net deposits over 30 years* | Riester pension balance after 30 years | Return from funding per year |

|---|---|---|---|

| Married couple, one earns €26,000, three children (born 2017, 2018, 2019) | 3600 € | 41,100 € | 13,8 % |

| Average earner with 43,142 euros, no children | 36.720 € | 52.470 € | 2,18 % |

| High earners with 70,000 euros, no children | 39.662 € | 64.292 € | 2,89 % |

*Net deposits after offsetting the allowances and tax refunds over 30 years

Source: [1]

You can also use Riester pension calculators to check the Riester pension benefits.

Due to a 4% minimum contribution, high earners end up saving a lot of their own money in a low-return Riester contract.

Moreover, the tax benefits are also not attractive as the tax office limited the tax-deductible sum to 2100 €.

Thus, investing in a flexible ETF savings plan makes more sense for high-earners instead.

For example, MSCI world ETF has offered an average 9% annual return since 1975. On the other hand, Riester’s contract offered a 2.89% return only. And the return will decrease with an increase in the annual income.

Moreover, you can access the money invested in an ETF savings plan anytime.

You can open a free depot account with Scalable Capital* and start investing.

If you are self-employed with a high income and don’t contribute to statutory pension insurance, you should consider taking Rürup pension insurance.

Is taking any pension scheme in Germany worth it?

German pension system offers several pension schemes. Though not every pension plan fits all, you must get at least one.

Employees are compulsorily insured under the statutory pension system. But others must take care of their retirement provisions themselves.

Of course, everyone can become part of a state pension. But you should explore private pension schemes before signing the state pension contract.

Who can take Riester Pension insurance in Germany?

Anyone compulsorily insured under the statutory pension scheme can take Riester pension insurance. It includes

- Employees

- Trainees

- Self-employed people subject to state pension insurance, i.e., craftsmen, teachers, midwives, or artists.

- Civil servants

- Recipients of unemployment benefits or citizen’s benefit

- Parents on parental leave

- Mini-jobbers who contribute to the state pension insurance

Advantages of the Riester pension in Germany

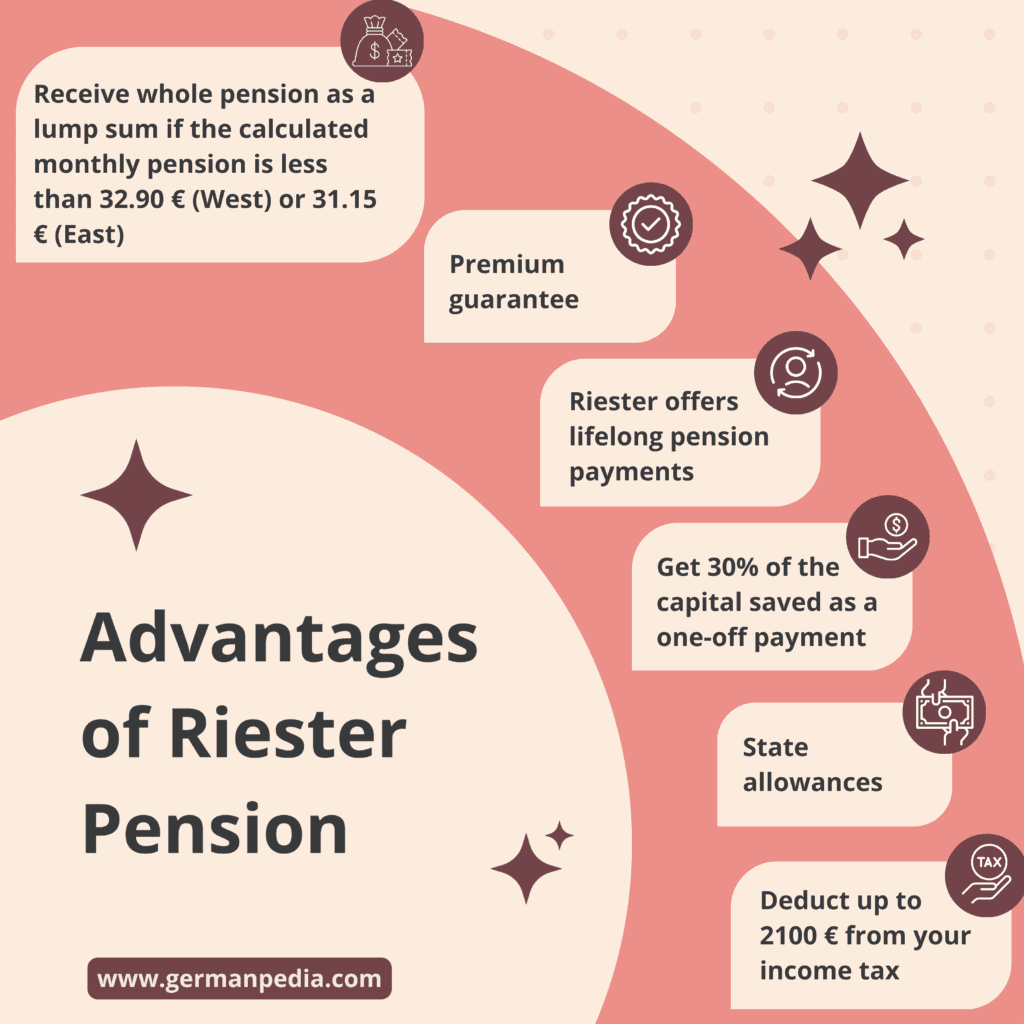

- Premium guarantee: As per German law, Riester pension providers must offer a premium guarantee. It means you’ll at least receive your contributions and state allowances after retirement.

- Riester offers lifelong pension payments. You can start getting a Riester pension from the age of 60 (contract signed before 2012) and 62 (contract signed after 2012).

- One-off payment: You can get 30% of the capital saved in Riester pension as a one-off payment. The lump sum payment ensures you get much of your money at the beginning of retirement.

- You receive your whole pension as a lump sum (as per Section 18 SGB IV ) if the calculated monthly pension is less than 32.90 € (West) or 31.15 € (East). It is called a small amount pension (Kleinbetragsrente in German).

- Tax benefit: You can deduct up to 2100 € of Riester contribution as special expenses from your income tax.

- State allowances: 175 € of basic allowance, 185 € (before 2008) or 300 € (after 2008) of child allowance per child, 200 € of joining bonus for people under 25.

- Insolvency proof: Like the Rürup pension plan, the Riester pension scheme remains unaffected in the event of unemployment (Hartz IV) or bankruptcy.

- You can use a Residential Reister contract to pay off the mortgage quickly.

NOTE: You should postpone your one-off payment until a year in which you receive only pension and no salary. It is because the Riester pension is taxed based on your personal tax rate. And your tax rate is higher when you receive salary as compared to when you don’t.

You can compare Riester pension plans on the comparison portal Check24*.

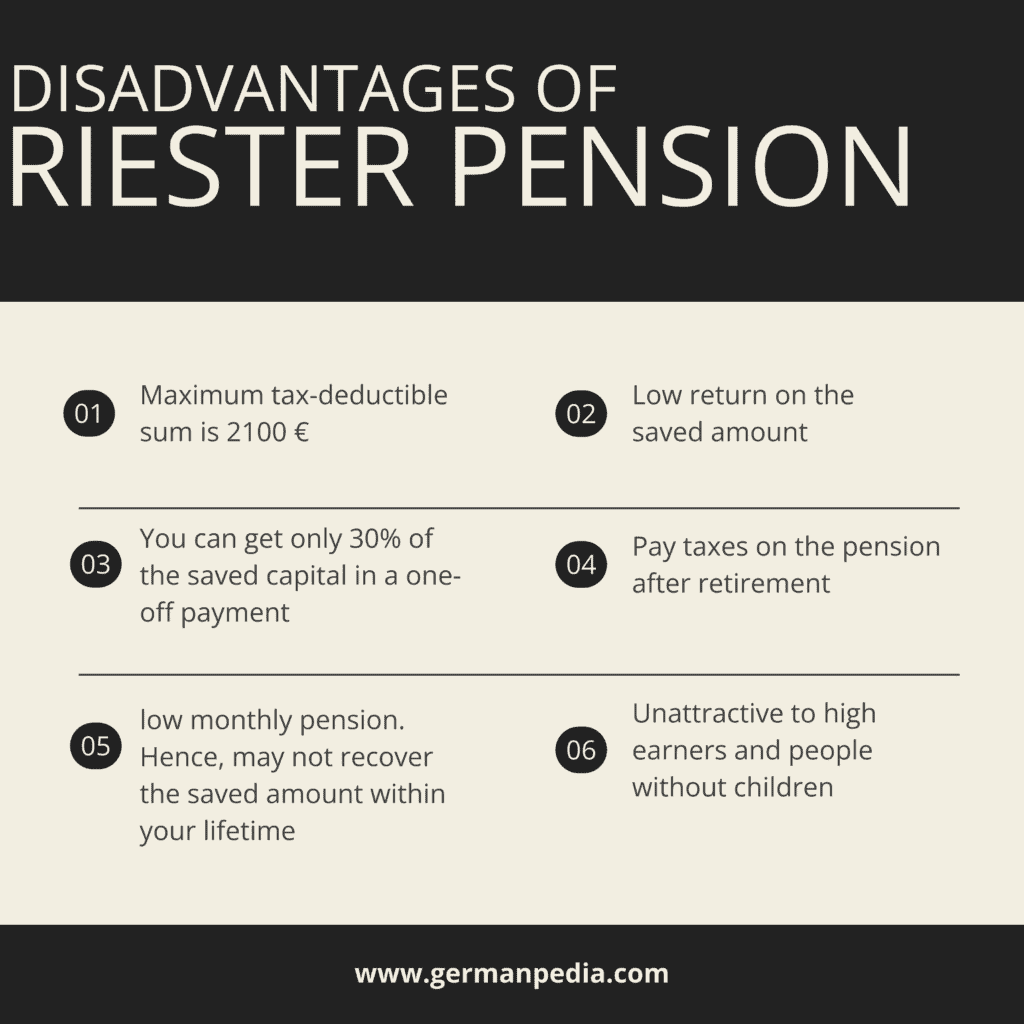

Disadvantages of the Riester Pension Plan in Germany

- The tax office capped the tax-deductible sum to 2100 €. It makes Riester pension unattractive for high earners.

- Low return on the saved amount. As Riester pension providers must offer a premium guarantee, they invest your money in safe investments offering low returns.

- You can get only 30% of the saved capital in a one-off payment.

- State subsidies and tax benefits are unattractive to high earners and people without children.

- You pay taxes on the pension after retirement. The tax rate is based on your personal income tax rate.

- The Riester insurance providers calculate the monthly pension based on long life expectancy. It results in a low monthly pension, and you may not recover the saved amount within your lifetime.

- According to a study by DIW Berlin, women receive an average of 55 € Riester-pension per month. And men receive an average of 100 €.

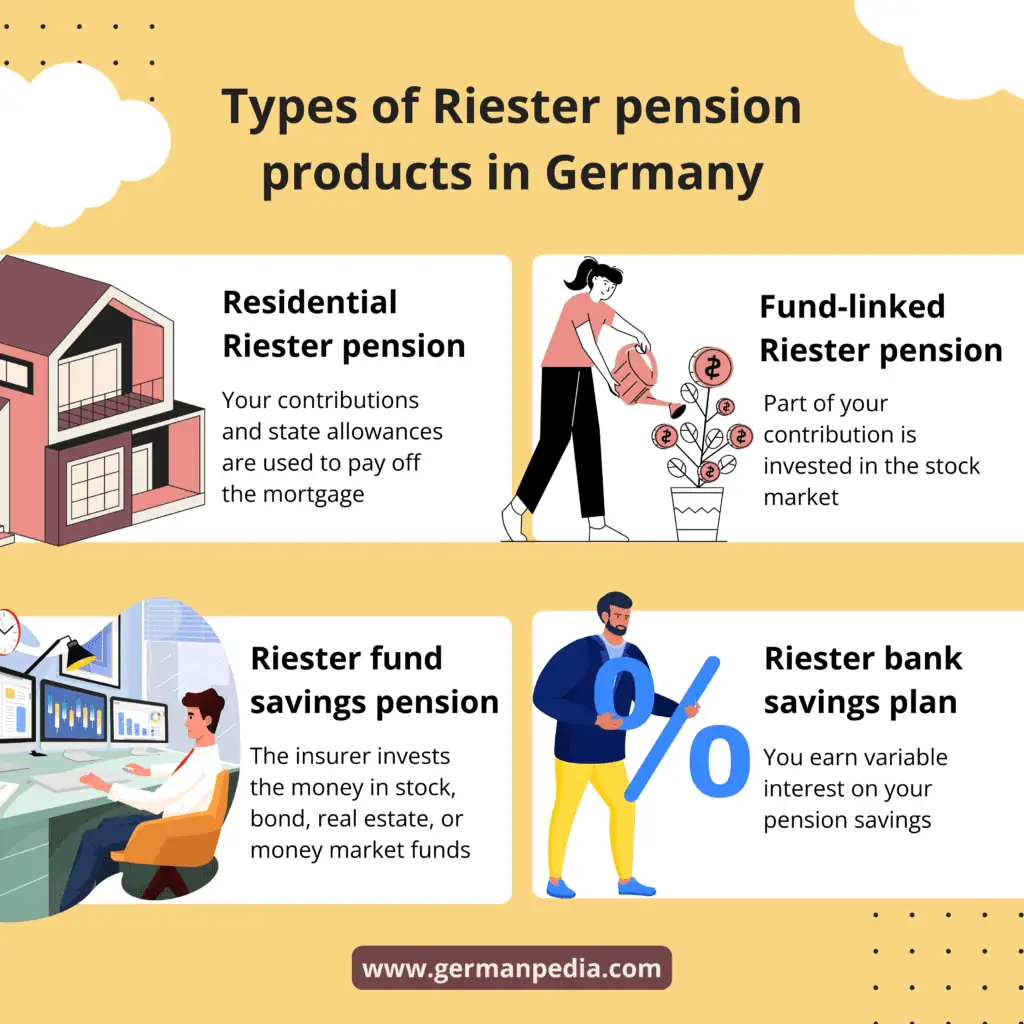

Types of Riester pension products available in Germany

All types of Riester products have the following in common

- State subsidy and tax benefits

- The insurer must offer a premium guarantee

- Lifelong pension

- Option of 30% one-off payment at the start of retirement

Let’s check how they vary from one another.

Classic Riester Pension Plan

Classic Riester is what we learned in this guide. You contribute at least 4% of your gross annual income to the Riester pension. You get state allowances and tax benefits during the savings phase.

In return, the insurer guarantees a lifelong pension after retirement. As per German law, the insurer must also provide a premium guarantee.

You can compare Riester pension plans on the comparison portal Check24*.

Fund-linked Riester pension insurance (Fondsgebundene Riester-Rentenversicherung)

In the Fund-linked Reiester pension, part of your contribution is invested in the stock market. Hence, you can expect better returns than with the Classic Riester.

However, as insurers must give premium guarantee, they invest conservatively. Thus reducing the returns compared to money invested in an ETF savings plan.

Riester savers pick the fund (stocks portfolio) where their money should be invested. But it’s a double-edged sword.

On the one hand, you decide where your money should be invested. On the other hand, it’s risky if you don’t know what you are doing.

Moreover, you must change the funds based on their performance.

There are additional tax advantages in the Fund-linked Riester pension plan. You pay tax on only 50% of the capital gains if the pension policy runs for at least 12 years and the money goes to the insured person.

For example, Suppose 20k increases to 25k after twelve years. You pay tax on 2,500 € ((25k – 20k) / 2) instead of 5000€.

Your tax rate is based on your personal income tax rate.

Riester fund savings pension plan (Riester-Fondssparplan)

In the Riester fund savings pension, the insurer invests the money in stock, bond, real estate, or money market funds. Thus offering better returns than the classic Reister product.

The insurers offer two types of Riester fund savings plans:

The dynamically managed model

In this model, funds managers actively manage your retirement provision. Fund managers invest heavily in the stock market as long as the stock market is doing well.

However, fund managers shift the money into safe pension funds if the stock market is not performing well.

The disadvantage of this pension model is the losses due to a stock market crash shortly before retirement cannot be compensated.

Moreover, the higher the pension provision invested in the stock market, the higher the Riester pension management costs.

The life cycle model

As the Riester saver nears their retirement age, the share of the pension fund invested in the stock market reduces.

The insurer does it to prevent the Riester saver from losing money shortly before retirement.

But simultaneously, it reduces the return if the stock market does well.

Riester bank savings plan (Riester-Banksparplan)

In the Riester bank savings plan, you earn variable interest on your pension savings. The interest rate depends on the current savings interest rates.

However, most German banks stopped selling Riester bank savings plans in 2017. Hence, it’s tough to find one nowadays.

Residential Riester pension insurance scheme (Wohn Riester)

The Residential Riester pension policy is for people planning to buy or build a house in Germany. Your contributions and state allowances in the Residential Riester are used to pay off the mortgage.

But the annual contribution to the Residential Riester is limited to 2100 €. And the Riester contribution to the total mortgage is usually small.

Many insurance providers and brokers sell Residential Riester pension schemes, claiming low mortgage interest rates. But the low-interest benefits diminish as you must pay taxes on the Riester pension.

You must pay taxes on the Riester pension after retirement. Usually, the amount on which you pay tax is more than the Riester sum used to pay the mortgage.

Taxation on Residential Riester Pension

As you don’t get a pension in Residential Riester, the legislature created a “housing support account” to calculate taxes.

The state uses the “housing support account” to note all the subsidized repayments and allowances.

Moreover, the legislature charges a 2% annual interest on the allowances. It means the amount on which tax must be paid is more than the amount used to repay the loan.

For example, suppose you have 20 years until retirement and use 10k from your Riester contract for loan repayment. The state will charge 2% interest on 10k for 20 years.

Thus, 10k increases to approximately 15k after 20 years. And you must tax on 15k after retirement.

So, assuming a tax rate of 20%, the tax you must pay is 3k (20% of 15k). In other words, to use a 10k Riester pension, you must pay 3k in taxes.

Conclusion

Don’t sign a Residential Riester blindly. Ask the insurance provider about the total benefits during the saving phase and the taxes you must pay after retirement.

Compare the benefits and taxes to decide if a Residential Riester contract makes sense.

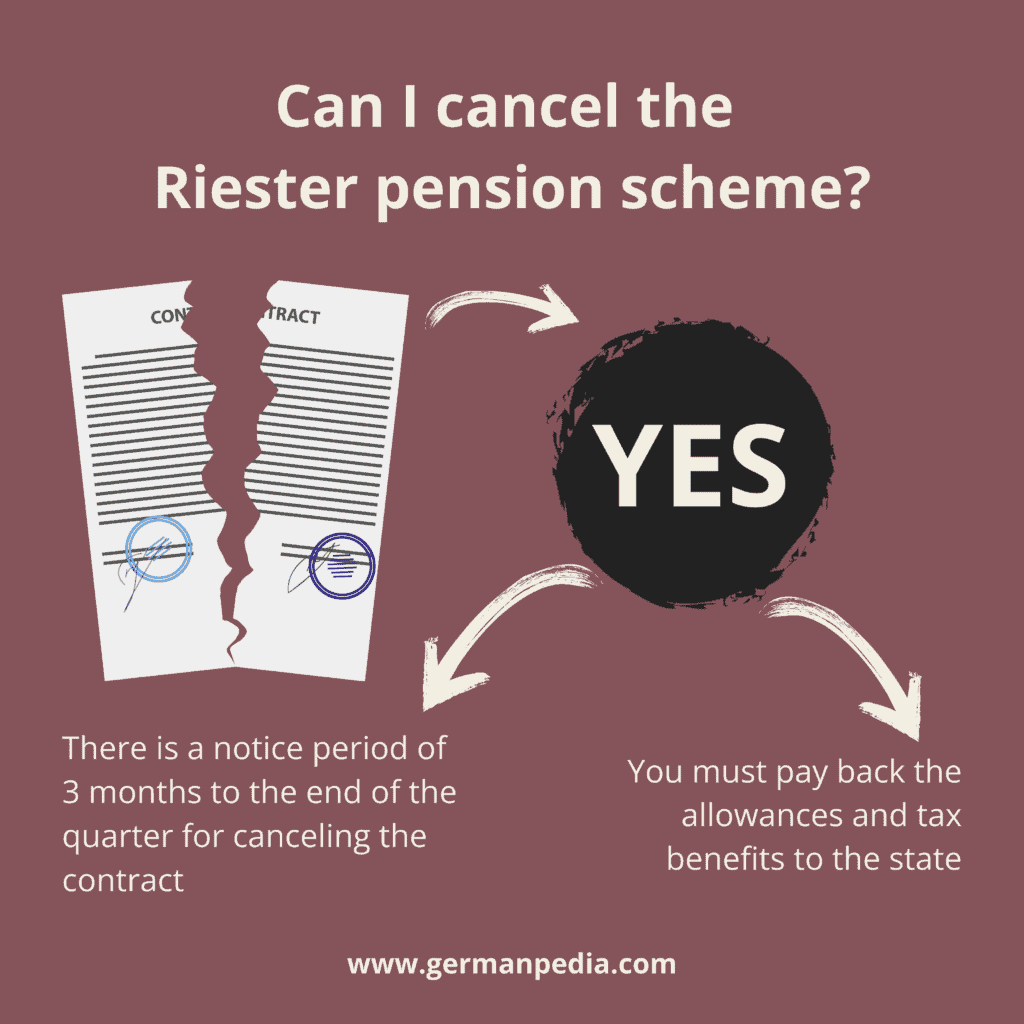

Can I cancel the Riester pension scheme?

Yes, you can cancel the Riester pension plan anytime. Once you cancel the contract, you get back the saved capital.

However,

- there is a notice period of three months to the end of the quarter for canceling the contract,

- and you must pay back the allowances and tax benefits to the state.

So, it doesn’t make sense to cancel the Riester pension plan. However, you can put the pension contract on hold.

It means you stop contributing to the Riester contract and don’t receive the state funding. But the allowances you received already will not be lost.

On top of that, you can start contributing to the Riester pension again any time you desire.

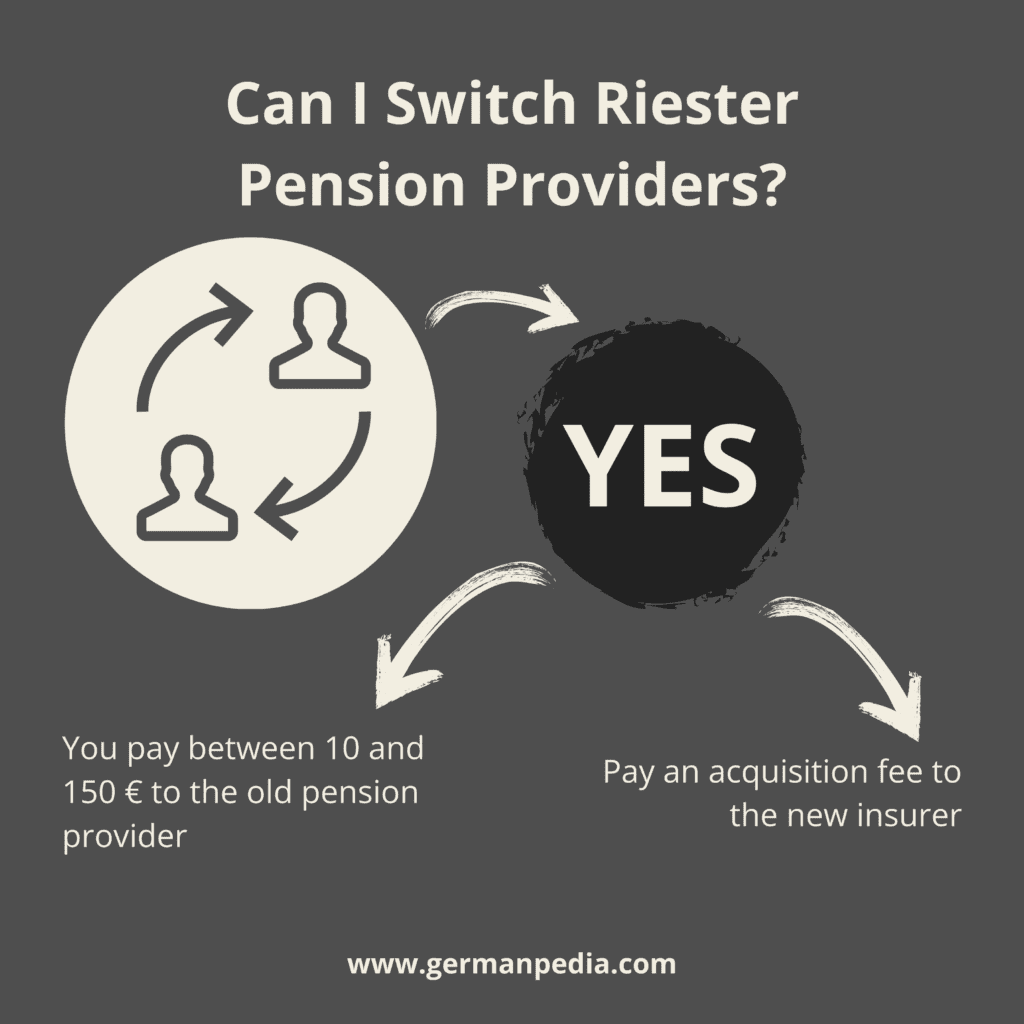

Can I switch Riester Pension Providers?

Yes, you can change your Riester pension provider. However, you must pay fees to both old and new insurers.

Depending on the contract, you pay between 10 and 150 € to the old pension provider. And pay an acquisition fee to the new insurer.

Moreover, you may incur losses in fund-linked and fund-savings Riester plans if you change the providers at the wrong time. The premium guarantee comes into play at the retirement age.

So, changing the insurer before retirement can lead to losses you must bear.

What is the return on the Riester pension plan?

The table below shows the return on the Riester pension plan in different scenarios.

| Example case (gross income) | Deposits* after 30 years | Account balance after 30 years | Return from funding per year |

|---|---|---|---|

| Average earner with 43,142 euros, no children | 36,720 € | 52,470 € | 2.18 % |

| High earners with 70,000 euros, no children | 39,662 € | 64,292 € | 2.89 % |

| Low earner with €26,000, one child (born 2017) | 19,034 € | 31,376 € | 3.26 % |

| Single parent with €12,000, three children (born 2014, 2016, 2017) | 4,005 € | 26,955 € | 13.64 % |

| Married couple, one earns €43,142 gross, three children (born 2014, 2016, 2017) | 24,810 € | 53,730 € | 5.59 % |

*These are the net deposits after offsetting the allowances and tax refunds over 30 years

Source: Finanztip

You can also use Riester pension calculators to check the Riester pension benefits.

You can see in which circumstances Riester’s pension makes sense by playing with the calculator.

If you are looking for high returns and flexibility, investing in an ETF savings plan is a good option.

You can open a free depot account with Scalable Capital* and start investing.

NOTE: Investing involves risk of loss.

References

- https://www.finanztip.de/riester/

- https://www.sparkasse.de/pk/produkte/altersvorsorge/riester-rente.html

- https://www.ihre-vorsorge.de/altersvorsorge/riester-rente#welche-riester-formen-gibt-es

- https://www.ihre-vorsorge.de/altersvorsorge/riester-rente/riester-fondssparplan#so-funktioniert-der-riester-fondssparplan

- https://www.finanztip.de/riester/wohn-riester/

- https://www.dieversicherer.de/versicherer/altersvorsorge/riester-rente#welche-riester-vertr-ge-gibt-es-