Reviewed by experts

Reviewed by:

Key takeaways

- Private health insurance is cheaper than public health insurance for young high earners (up to 37 years). If you plan well, private insurance can be cheaper even after retirement.

- Private insurance costs have increased by 3.2% per annum for the last ten years. Premiums usually increase abruptly due to German laws regarding premium adjustment.

- The future of the German health system doesn’t look very good due to the aging population and fewer earners.

- Private health insurance is better prepared for the future than the public system, with its aging provisions of 344 billion euros (as of Feb 2025).

This is how you do it

- If you are a high earner and believe you’ll continue to earn high in the future, you should consider moving to private health insurance.

- Private health insurance is a complicated product. You should consult a fee-based advisor or an insurance broker for a personalized advice. You can book a free call with one of the experts we recommend here.

- Insurance brokers and advisors are liable for their advice. So, if they didn’t recommend a plan per your wishes, they are liable to pay for the damages.

Table of Contents

What is private health insurance in Germany?

Every resident in Germany must have health insurance. The German health insurance system is divided into two groups: private health insurance and public health insurance.

As the name suggests, private companies offer private health insurance.

The German government regulates private insurers. However, they don’t have as much control as they do on public health insurance.

How much does a private health insurance policy cost?

The cost of private health insurance depends on your tariff, age, and health at the time of taking the policy. The private insurance costs for people in different age groups and professions if they take it in 2025.

- Children insured by their parents: between €98 and €200 per month. Your employer also contributes to your child’s premium, but there is a maximum limit.

- Young employee: starting from €250 per month (after deducting the employer’s contribution).

- 35-year-old employee: between 301 € and 430 € per month (after deducting the employer’s contribution)

- Self-employed: between 563 € and 830 € per month

- Civil servant (Beamter in German) with 50% subsidy: between 325 € and 440 € per month

- Civil servant (Beamter in German) with 70% subsidy: between 256 € and 330 € per month

- Not working: It doesn’t matter if you are not employed; private health insurance premiums do not depend on your income.

You can learn more about the costs in our guide on health insurance costs in Germany.

German Healthcare Demystified – Free eBook

- The German healthcare system is complex. This is why we wrote this book to help you navigate it.

- Choosing health insurance is a life-long decision. If you pick the wrong plan, it may cost you dearly in the future.

- Learn what is covered in public and private health insurance and what is not.

- What supplement health insurance plans must you get based on your personal situation?

Break up of private health insurance premium

Private health insurance premium consists of the following components

Up to 60

- Risk portion (Riskioanteil / Risikozuschlag): Your premium’s “Risk portion” is based on the statistical medical costs of people in your age group. It’s different for each insurance provider.

- Cost portion (Kostenanteil): This covers the insurance company’s administrative costs, such as taking out insurance, settling claims, etc.

- Savings portion (Sparanteil): The insurance company saves part of your premium to compensate for the increased medical costs as you age. Every insurance provider saves a different percentage of your premium. The more an insurer saves, the better. Insurers like Hallesche, Universa, R+V, etc., have stable premiums for a long time because they save a higher percentage of your premium.

- 10% statutory surcharge (Gesetzlicher Zuschlag): The 10% statutory surcharge is required by law. Every private insurer must charge this to its customers. The amount is saved and invested. It’s used to keep the premium stable in old age. The surcharge complements the saving portion (Sparanteil) made by the private insurer.

The savings portion (Sparanteil) plus the statutory surcharge (Gesetzlicher Zuschlag) together are called aging provisions (Alterungsrückstellung in German).

Additionally, you also pay for

- Long-term nursing care insurance: It’s mandatory by law. You pay the same amount as in the statutory long-term nursing care insurance.

- Sickness benefits insurance: It’s optional but highly recommended. It pays sick pay after the 43rd day of your long-term sickness.

- Risk surcharge: Lastly, the private health insurance company charges a risk surcharge based on your existing illnesses. You don’t pay any risk surcharge if you don’t have any existing diseases.

From 60 to 67 (until you retire)

- You stop paying a 10% statutory surcharge.

After retirement

- You stop paying for sickness benefits insurance.

- You stop paying a 10% statutory surcharge.

NOTE: When you switch your private health insurance provider, you can transfer part of your old age provisions to the new provider. The amount of old age provisions you can transfer to the new provider is called “transfer value (Übertragungswert).”

Every insurance company calculates the transfer value (Übertragungswert) differently. However, it’s around 70% of your total aging reserve.

So, you lose 30% of your savings if you change the private health insurance company. This is why you should get expert’s help when taking private health insurance in Germany.

Book a free call with a health insurance expert

- German health insurance is a complicated product. There are several factors that must be considered before deciding which health insurance is best for you. An expert can guide you and help you pick the best option for you.

- An Insurance broker is liable for their advice. This means if the policy they recommended doesn’t offer the coverage you requested, they are liable to pay the damages incurred in the future.

How do private health insurance providers in Germany calculate the monthly premium?

The private health insurance provider calculates your contribution based on

- the scope of services,

- your age,

- any pre-existing illnesses,

- life expectancy (statistically calculated), and

- medical expenses you may incur throughout the insured period (statistically calculated).

Additionally, private health insurance companies segregate people into groups based on their tariffs and age when taking the insurance.

Private insurers create a pool of funds for each group. It saves part of the contributions of the insured in this fund.

The funds saved by the group over time cover

- the medical costs of sick people in the group and

- compensate for the increased medical expenses in the future.

Private insurance providers aim that the total premium collected over the entire insurance period is enough to cover all expected insurance benefits throughout the insured person’s life.

So, in younger years, larger parts of your monthly contribution are saved and invested. These savings are called retirement provisions or aging provisions.

Private insurance companies use the aging provisions to

- cover higher medical expenses in the future

- and keep the premiums stable as you grow old.

Unlike public health insurance, which relies on young professionals to pay the increased medical expenses, private insurance builds up a savings cushion.

Difference between public and private health insurance premium calculations

| Private health insurance | Public health insurance |

| Premium has increased on average 3.9% per annum between 2015 and 2025 and 3.1% per annum between 2005 and 2025 | Premium has increased on average 4.1% per annum between 2015 and 2025 and 3.8% per annum between 2005 and 2025 |

| Private insurance is usually cheaper for high earners throughout their life. | Public insurance is usually expensive for high earners throughout their life. |

| Premium depends on age, existing illnesses, and tariff | Premium depends on your gross income |

| Creates an aging provision to cover the increased medical expenses in the future | No aging provision |

| It calculates the premium for each individual to cover the medical services benefits from the start of insurance to the insured person’s death. | Public insurance is always hand-to-mouth. It pays for the bills now and relies on young professionals to cover the costs. |

| Private insurers cannot change the contractually agreed services. | Public insurance is reducing medical services almost every year. |

| A 35-year-old with a top private health insurance plan pays around 800€ per month (as of 2025). | A 35-year-old high-earner with public health insurance pays around 1174€ per month (as of 2025) |

| Based on the current trend of increasing medical expenses and insurance premiums, the 35-year-old individual from above will pay between 2000€ per month and 2520€ per month after 30 years (65 years old or in 2055). | Based on the current trend of increasing medical expenses and insurance premiums, the 35-year-old individual from above will pay between 3594 € per month and 3919€ per month after 30 years (65 years old). |

| Based on the current trend and subsidies, you’ll pay between 1600 € and 2120 € per month after retirement (67 years old or in 2057). NOTE: We have calculated the future premium based on a 3.1% and 3.9% increase in the premium. | People insured under public health insurance for retirees (KVdR) will pay a monthly subsidized premium of 1200 € per month after retirement (67 years old or in 2057). NOTE: We have calculated the future premium based on a 4.1% increase in the premium. |

Price development source: WIP-PKV

Conclusion

Private health insurance is cheaper for high earners. Moreover, it’s better prepared for the rise of medical expenses in the future and Germany’s growing older population.

So, if you are a high earner and believe you’ll continue to earn high in the future, you should consider moving to private health insurance.

Besides that, everyone should save a cushion to cover their medical expenses in old age.

Private health insurance is a complicated product. So, we recommend consulting a fee-based advisor or an insurance broker for personalized advice.

Book a free call with a health insurance expert

- German health insurance is a complicated product. There are several factors that must be considered before deciding which health insurance is best for you. An expert can guide you and help you pick the best option for you.

- An Insurance broker is liable for their advice. This means if the policy they recommended doesn’t offer the coverage you requested, they are liable to pay the damages incurred in the future.

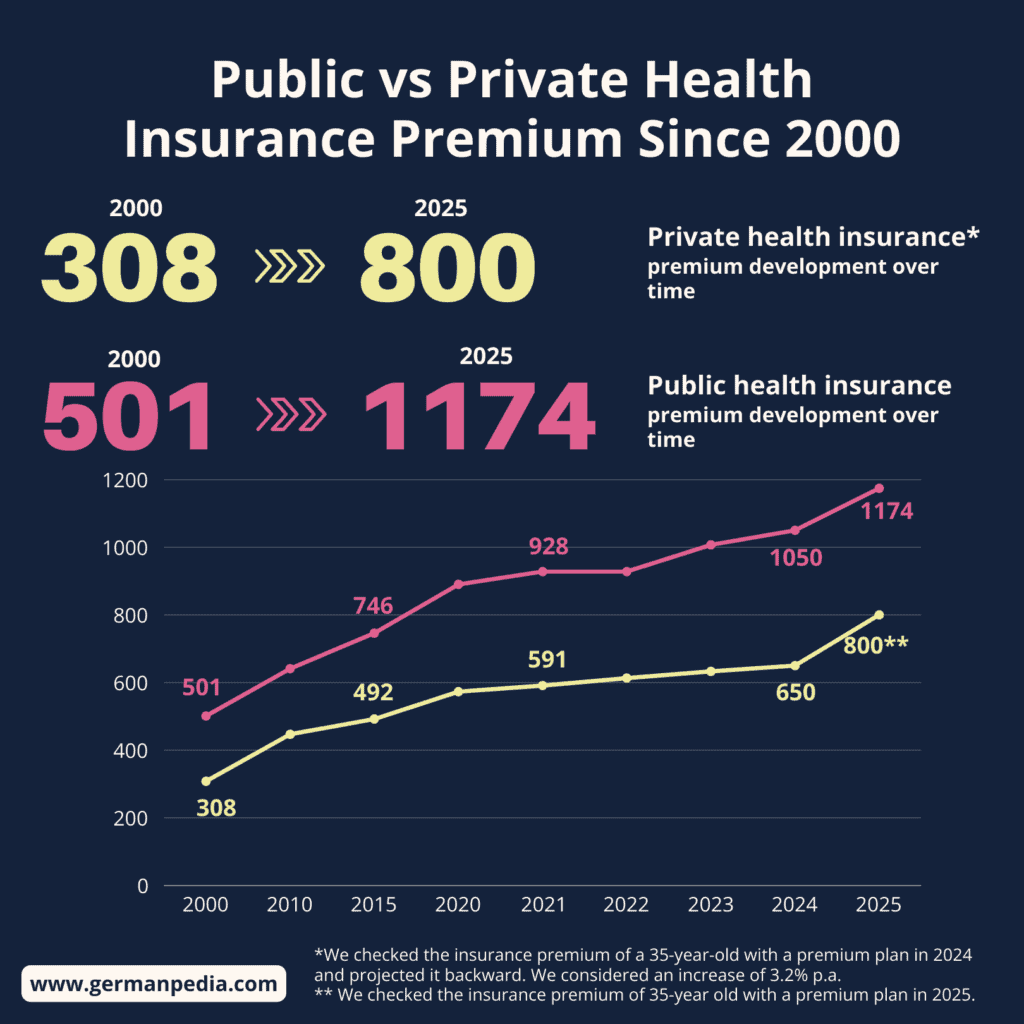

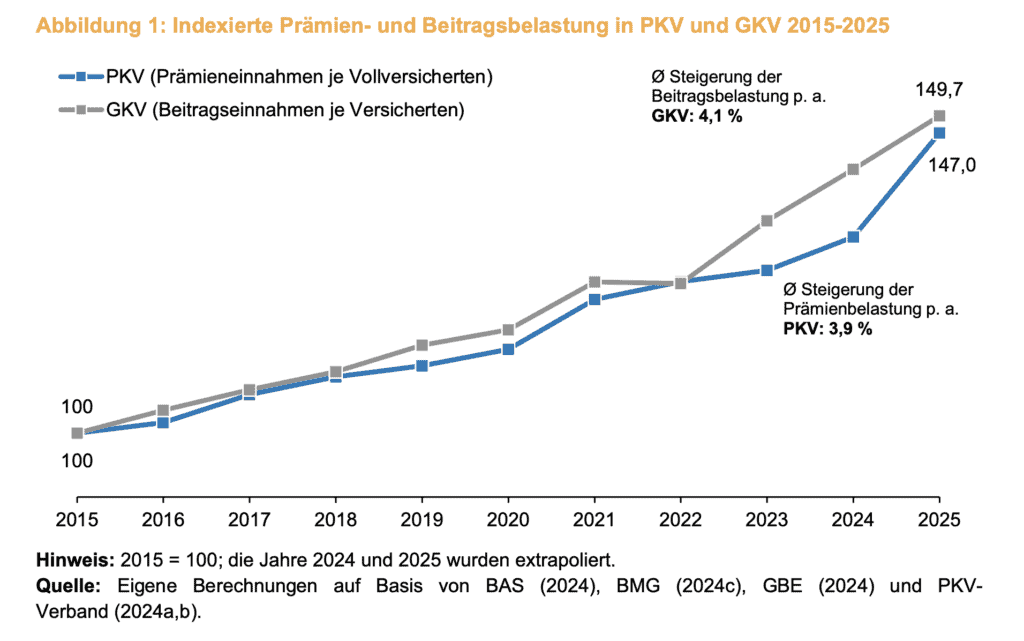

As the image above shows, private health insurance has been cheaper than public health insurance since 2000.

How much did the private health insurance premium rise in the past?

It’s one thing for your health insurance premium to rise 2% to 3% yearly. But if it grows abruptly more than 10% or 20%, it can affect your finances greatly.

Unfortunately, private health insurance premiums can rise more than 10% in one year.

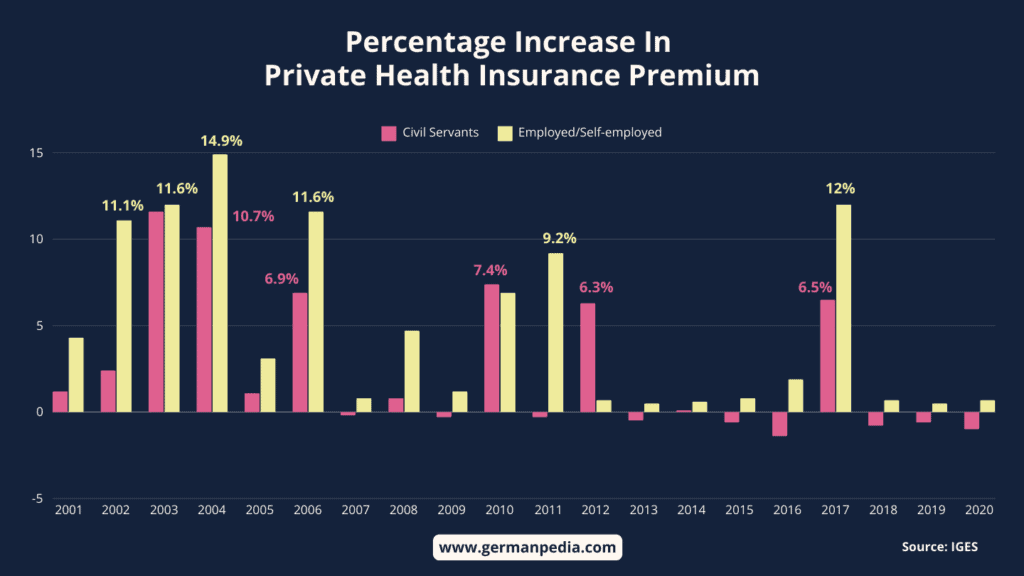

Abrupt rise of private health insurance premium

IGES studied the premium development of Debeka’s 800,000 private health insurance members between 2000 and 2020. In the study, researchers found that private health premiums rose abruptly

- at least twice 20% or more, or

- at least five times 10% or more

The researchers found that this sudden jump in the insurance premium affected 39% of the employed and self-employed. The percentage reduces to 13% for civil servants.

Debeka is the largest private health insurance company in terms of the number of privately insured members (2.5 million customers as of 2024). This is a quarter of the total privately insured people in Germany.

So, even if Debeka doesn’t represent the whole private health insurance industry, we can still get a good picture of the premium development.

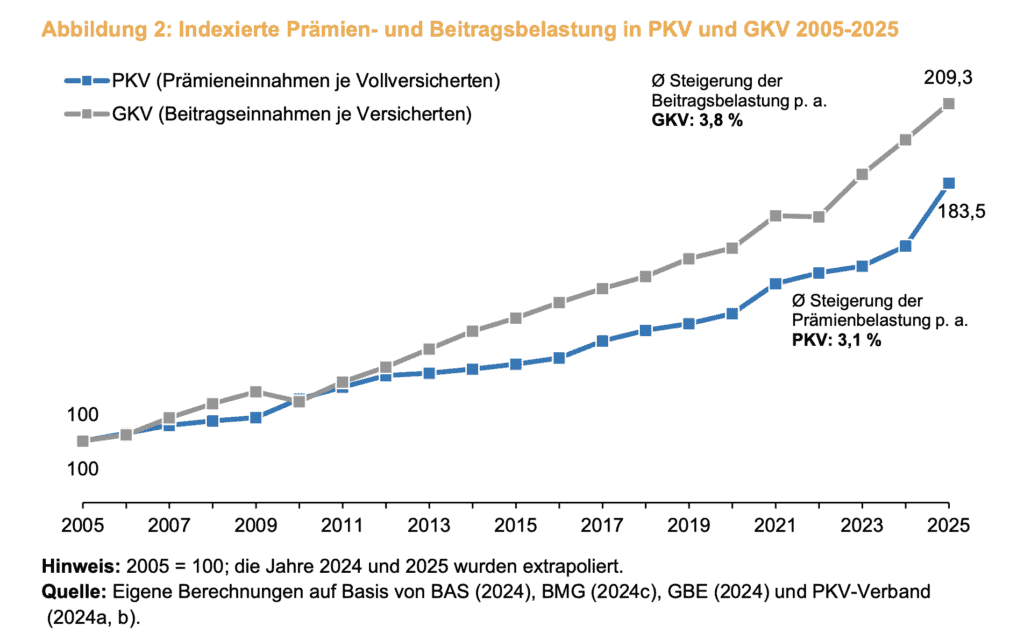

Average increase in private and public health insurance premiums over 20 years

Although private health insurance costs increase by a large percentage abruptly, the average increase in premiums over 20 years is 3.1% per annum between 2005 and 2025.

Conversely, public health insurance costs have increased by 3.8% per annum between 2005 and 2025.

Average private and statutory health insurance premium increase in over 10 years

Health insurance costs in Germany have increased faster in the last ten years (2015 to 2025) than in the last twenty years.

- Private health insurance costs increased by 3.9% per annum between 2015 and 2025.

- Public health insurance costs increase by 4.1% per annum between 2015 and 2025.

Why do private health insurance costs rise abruptly in Germany?

Private health insurance companies can only make a premium adjustment if the cost of insurance benefits in the tariff has increased by at least 10%.

This restriction on increasing insurance premiums is intended to protect consumers. However, it has a side effect, i.e., the abrupt increase in private health insurance premiums.

It’s because medical treatment costs are increasing continuously due to inflation and medical progress. However, the insurer cannot increase the premiums continuously.

Let’s understand it with an example.

Suppose the cost of insurance benefits in your tariff increases by 4% every year. So, it’ll take three years to cross the threshold of 10%.

You’ll continue to pay the same premium during these three years. However, the insurance company must cover the increased medical costs.

Thus, when the time comes to increase insurance premiums, the insurer compensates for the increased costs in the past years in one fell swoop. This leads to an abrupt rise in private health insurance premiums.

Reasons for the increase in private health insurance costs in Germany

- Low interest rate: Private health insurance companies must save part of the premium (retirement provision). The insurer invests this saved amount to earn interest. The insurer uses the saved amount plus the earned interest to keep the insurance cost stable in old age. However, due to the low interest rate in the past decade, insurers cannot earn good interest. Thus, they must charge higher premiums to compensate for the low interest.

- Inflation: Medical costs increase each year due to inflation. Private health companies transfer this increased cost to their members by increasing the premium.

- Medical science progress: Innovations in the medical field offer better and more treatment options to patients. This leads to increased medical spending and a cost burden on health insurance companies. Ultimately, the increased costs are passed on to the end customers.

- Longer life expectancy: Life expectancy in Germany is around 81 years [1]. Statistically, each year costs the health system about twice as much as the previous one.

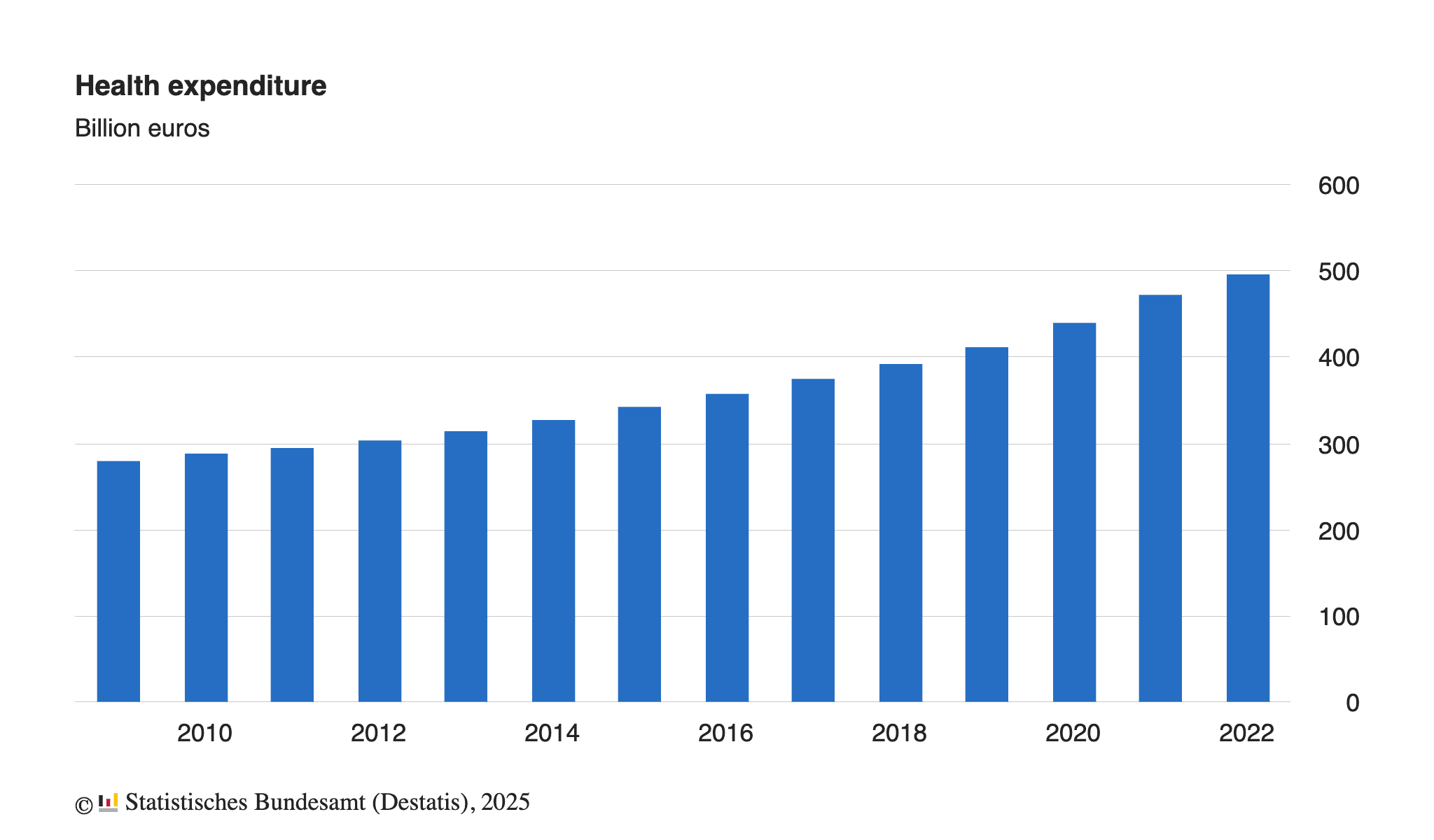

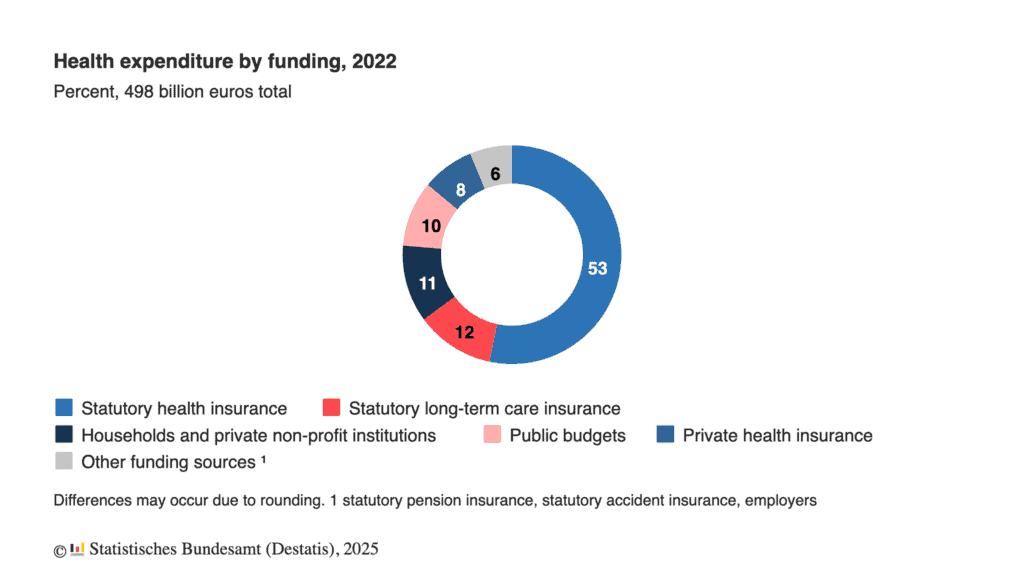

All the above factors are contributing to Germany’s increased medical expenditures. As you can see in the figure below, medical expenditures are rising consistently and were 497.7 billion euros in 2022.

German health insurance needs money to cover these medical expenditures. Current monthly health insurance contributions are not enough.

As a result, the German government has to fund around 10% of the medical expenditure.

Source: Destatis

In short, an increase in the cost of health insurance is inevitable in the future.

Is private health insurance unaffordable in old age?

One of the most common fears that prevent people from purchasing private health insurance is that the premiums will be unaffordable in old age. However, that’s not true.

The fear of unaffordable premiums emerged in the 1970s and 1980s. During this time, many young people bought private health insurance policies without or very low aging reserves.

No aging reserves made the insurance plans dirt cheap when young people bought them. However, insurance premiums rose drastically as people aged.

It’s because there were no aging reserves to compensate for the rising medical costs. This made premiums unaffordable for many people from the baby boomer generation.

The baby boomer generation passed on their negative experiences to the next generation. This is why so many people fear joining the private health system.

However, the German government and private health insurance companies learned from the past. The government made it mandatory for private insurance providers to save 10% (since 2000) of the premium as an aging reserve.

The insurers must use the saved mandatory surcharge to stabilize the health insurance premium after retirement.

Additionally, almost every private health insurance company nowadays saves part of your premium as an aging reserve. The percentage of the premium saved varies from insurer to insurer.

However, good private health insurance companies save between 30% and 45% of your premium as an aging reserve.

The aging reserves compensate for the rising medical expenses and keep the premiums stable.

How much do you pay for private health insurance before and after retirement?

Private health insurance premiums have increased on average 3.9% per annum between 2015 and 2025. So, assuming the premiums will continue to rise at this rate, we have created the table below.

Other assumptions

- You took private health insurance at the age of 35.

- You don’t have any pre-existing illnesses.

- You took a premium private health insurance plan.

| Projection created in 2025 | Projection created in 2024 | |

| Yearly increase in private insurance premium | 3.9% (2015 to 2025) | 3.2% (2014 to 2024) |

| Age (Nr. of years after taking private insurance) | Private health insurance premium per month | Private health insurance premium per month |

| 35 | 800€ | 650€ |

| 45 (10 years) | 1172€ | 890 € |

| 55 (20 years) | 1719€ | 1220 € |

| 65 (30 years) | 2520€ | 1672 € |

Once you turn 60, you stop paying the 10% statutory surcharge.

After retirement

A few things change once you retire.

- You don’t pay for the daily sickness allowance.

- Your saved retirement provisions are used to compensate for the increased medical costs.

- You get a health insurance subsidy from statutory pension insurance. The maximum subsidy you can get is around 200 € per month as of 2025.

- If you were employed, you wouldn’t get your employer’s contributions anymore. Thus, you pay the whole premium yourself.

After considering the above subsidies and deductions, your premium after retirement will be between 1600€ and 2120€ per month (in the year 2057).

Explanation

As you age, your medical expenses increase. However, your retirement provisions compensate for that increased medical cost. This way, you (65 years old) pay approximately the same premium as a 35-year-old individual would at that time.

For example, suppose you (35 year old) took private health insurance today in 2025. Your monthly premium is 800€ per month. You’ll retire in 2057 (when you are 67). Assuming premiums rise at 3.9% per annum, the health insurance premium for a healthy 35-year-old individual will be around 2721 € in 2057.

As you are insured for 32 years and have created enough retirement provisions, you (67 years old) pay approximately the same premium (2721 €) as the 35-year-old individual at that time.

After retirement, your premium decreases a bit as you get subsidies and don’t pay a 10% statutory surcharge and sickness benefit insurance.

How did we create this table?

We analyzed the actual health insurance premiums of people in different age groups. In our analysis, we found the following.

- A 70-year-old individual (insured for 35 years) pays approximately the same premium as a 35-year-old individual who just joined the insurer for the same services.

- After retirement, many people changed their tariffs to reduce the private health insurance premium.

- After retirement, many people increase their deductible considerably to reduce their premiums. However, they increase the deductible cleverly so that the effective premium (including the deductible) is still low.

You can check the actual private health insurance costs of 12 Universa’s customers here.

Conclusion

Private health insurance premiums will continue to rise. You can expect to pay approximately 2.5 times more after retirement.

The same is true for the public health insurance premiums. Moreover, experts predict that public insurance costs will rise even more in the future. However, this applies only to high earners.

So, you should check if you can afford private health insurance in old age.

You have the following options if you cannot afford private health insurance in old age.

- Every private health insurance provider is legally required to offer the “basic tariff.” The basic tariff offers the same services as public health insurance. Anyone who cannot afford private health insurance can go into the basic tariff.

- Change your private health insurance plan after retirement to reduce the costs.

- Increase your deductible to reduce the private health insurance costs.

- Save a cushion when you are young and working. Use it to pay the insurance premiums when you are old and retired. Based on our calculation if you save 200€ per month for 30 years, you can cover the premiums in old age via your savings alone.

In short, if the worst happens, you’ll still have ways to get affordable health insurance.

Book a free call with a health insurance expert

- German health insurance is a complicated product. There are several factors that must be considered before deciding which health insurance is best for you. An expert can guide you and help you pick the best option for you.

- An Insurance broker is liable for their advice. This means if the policy they recommended doesn’t offer the coverage you requested, they are liable to pay the damages incurred in the future.

Does private health insurance get more expensive than public over time?

Public health insurance premiums depend on your income. However, private health insurance premiums don’t.

Thus, if you earn less, you pay less for public health insurance.

So, to compare the costs of the two health systems meaningfully, we made the following assumptions.

- You are a high earner and pay maximum public health insurance premiums.

- You continue to earn high throughout your working life and even after retirement.

The answer is public health insurance costs more than private health insurance to high earners. Moreover, public health insurance costs have increased more than private health insurance over the past 20 years.

Here is a table that projects the cost of both health systems over time.

| Age (Nr. of years after taking private insurance) | Private health insurance | Public health insurance |

| Yearly increase in premium over the past 10 years (2015 to 2025) | 3.9% | 4.1% |

| Yearly increase in premium over the past 20 years (2005 to 2025) | 3.1% | 3.8% |

| Premium of a high-earner, self-employed individual | Premium increases by 3.9% per annum | Premium increases by 4.1% per annum |

| 35 (today) | 800 € (as of 2025) | 1174 € (as of 2025) |

| 45 (after 10 years) | 1172 € | 1754 € |

| 55 (after 20 years) | 1719 € | 2622 € |

| 65 (after 30 years) | 2520 € | 3919 € |

| After Retirement | ||

| 67 | 2320 € (you stop paying the sickness benefits) | 1400 € (if you stay in public insurance throughout your work life) |

| Maximum subsidy from pension insurance | 200 € (approx. as of 2024) | 200 € (approx. as of 2024) |

| Net premium you pay after retirement (67) | 2120 € (2320 – 200) | 1200 € (1370 – 200) |

| Total premium paid in 32 years | 588,000€ | 873,000€ |

As you can see, if you are a high earner, you’ll pay way more in the public system than in private throughout your work life. After retirement, the difference in the premiums is big only if you pay the subsidized public health insurance premium. However, there is no guarantee that the subsidy will stay even after 30 years.

You can reduce the cost of private health insurance by changing your plan or increasing the deductible. However, you have no way of reducing your public insurance premium.

You should also consider that the public health system is in financial trouble. So, the chances that the German government will get rid of the health insurance subsidy for retirees in the future is high.

Lastly, paying more in the public system doesn’t mean getting better services. On the contrary, good private health insurance plans offer better services than public insurance.

NOTE: Private health insurance is for people who expect a high income throughout their career. If you are a low-earner or expect a reduced income in the future, public health insurance is better.

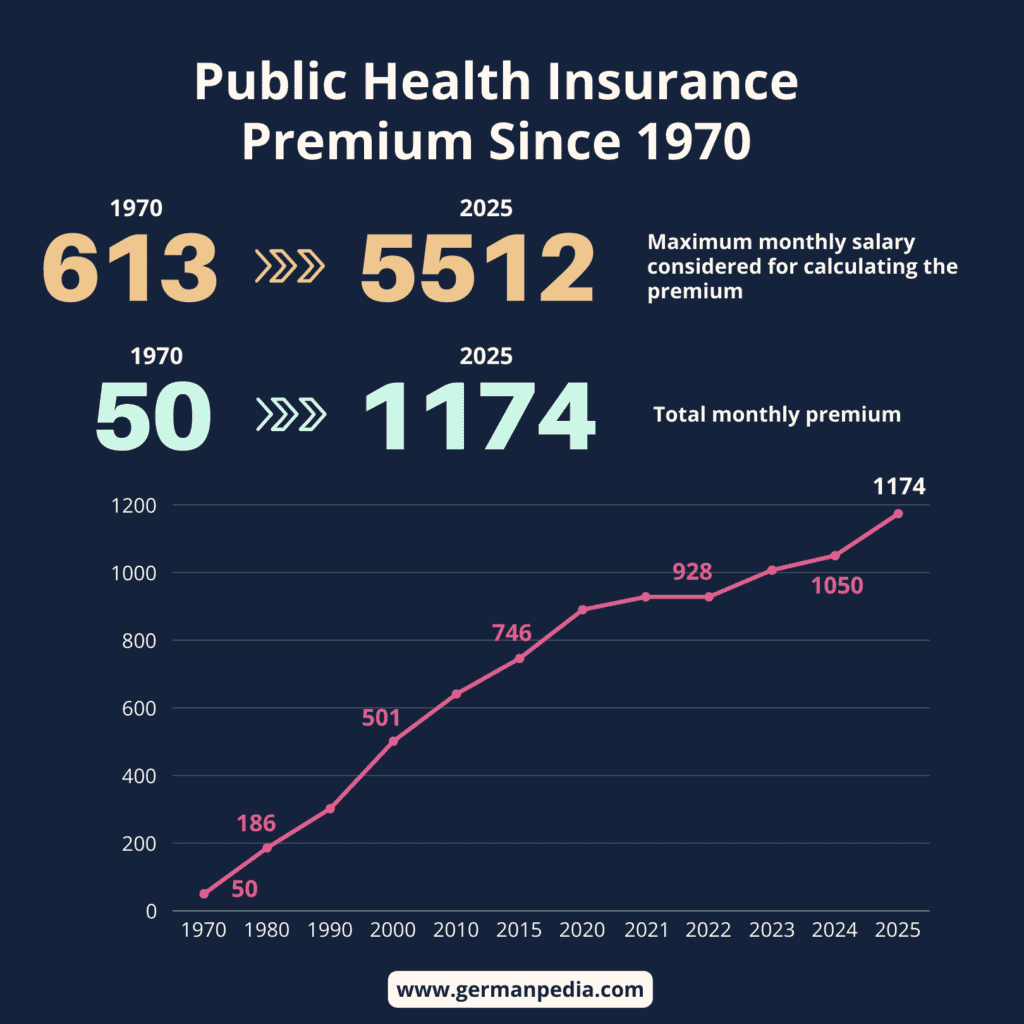

The image below shows the development of public health insurance premiums since 1970. As you can see, public insurance is 21 times more expensive in 2024 than in 1970.

How can private health insurance offer better services at a lower cost than public health insurance?

Private health insurance can offer better services at a lower cost than public health insurance for the following reasons.

- Private insurance accepts only healthy customers.

- Private insurance usually has people with better education and high income. Statistically, such people take care of their health more than others.

- Everyone pays for their health insurance. There is no free family insurance in the private system.

- Private health insurance saves part of the contributions (retirement provisions) to cover the increased medical costs in the future.

Future outlook of health insurance costs in Germany

As per health insurance and financial experts, the cost of both health systems will increase drastically. The public health system will be affected the most.

Future outlook of public health insurance costs in Germany

The public health insurance system works according to the backward distribution system. This means it first spends the money and relies on the young to pay the premiums.

However, by 2050, one-third of the German population will be 60 or older. Thus, Germany won’t have enough earners to cover the medical expenditures of the public health system.

As there will be more old people in Germany by 2050, the cost burden on the public health system will increase.

On the other hand, the earning population will decrease. This will lead to a drastic increase in public health insurance costs.

Additionally, public health insurance removes or limits medical coverage almost every year. The public health system is expected to further limit the medical services it covers in the future.

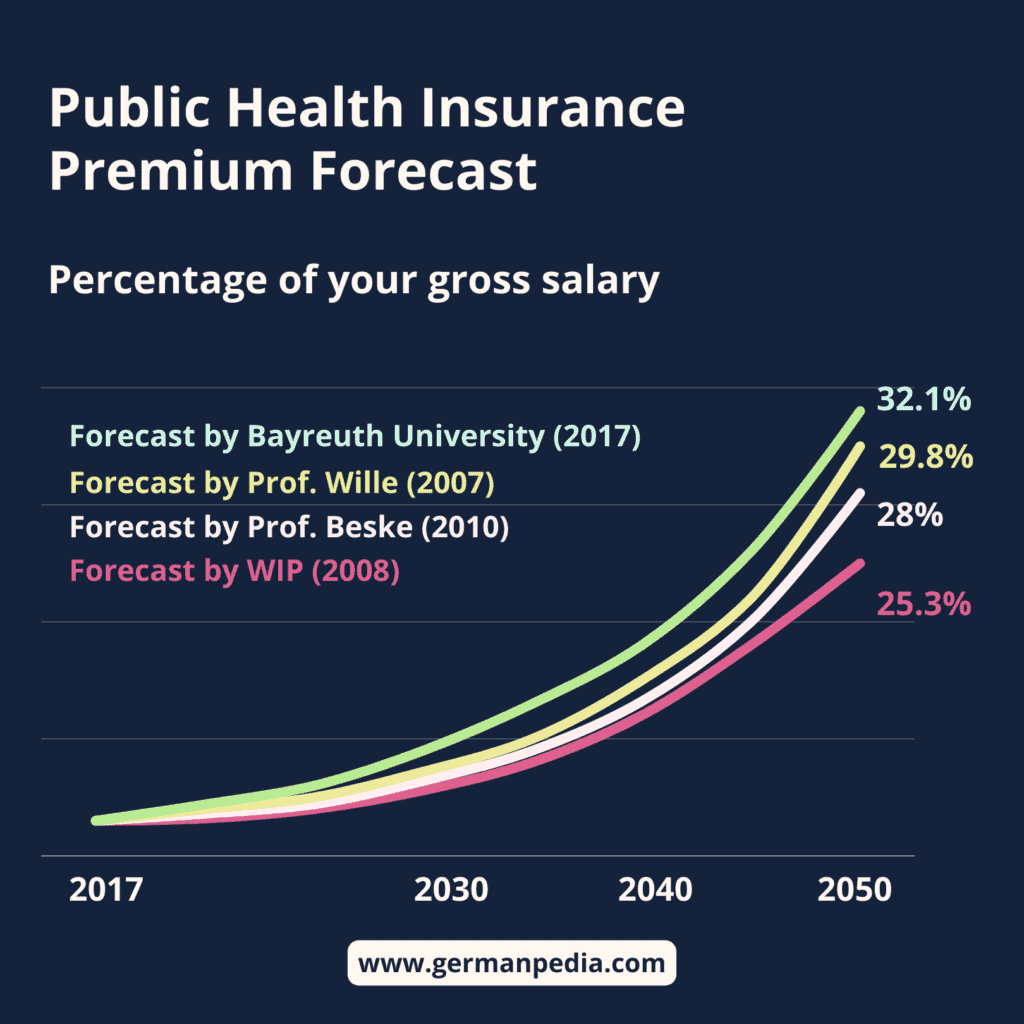

Experts’ view on public health insurance costs in the future

Various experts predicted an increase in public health insurance costs by 2050. According to them, the public health insurance premium will be between 25% and 32% of your gross salary by 2050.

Currently, you contribute 17.1% (14.6% + 2.5% (additional contribution)) (as of 2025) of your gross salary in the public system.

The image below shows the experts’ prediction of increasing public health insurance costs by 2050.

Future outlook of private health insurance costs in Germany

Both private and public health systems rely on each other. If one of them collapses, the other cannot survive alone.

So, you can expect a similar increase in private health insurance premiums. However, private health insurance doesn’t work like public health insurance.

This is how the private health system works.

Private health insurance companies create a group of individuals in the same age range. This group has its own pool of funds.

Everyone in the group pays for the medical coverage they contractually agreed. The private health insurance provider saves part of these contributions to the group’s pool of funds.

The funds the group saved collectively over the years will cover the increased medical expenses. Hence, private insurance companies do not rely on someone else (young earners) to pay the increased medical expenses.

However, if the number of old and sick people in this group increases, the premium of individuals in this group will also increase.

You can check the live amount saved in Germany’s private healthcare system here. When writing this guide, the total saved amount was 344 billion euros (Feb 2025).

Conclusion

The private health system is better prepared than the public system for the future.

- Private health insurance already has 344 billion euros saved to cover the increased medical expenses in the future.

- Private health insurance companies save part of your monthly contributions to compensate for future increases in medical costs.

So, if you are a high earner and believe you’ll continue to earn high in the future, you should consider moving to private health insurance.

Besides that, everyone should save a cushion to cover their medical expenses in old age.

Private health insurance is a complicated product. So, we recommend consulting a fee-based advisor or an insurance broker for personalized advice.

More topics

- Is private health insurance worth it?

- Private health insurance benefits that you don’t get public health insurance

- Minimum coverage your private health insurance plan should offer

- Private health insurance costs in Germany

- Private vs public health insurance

- Why is private health insurance cheaper than public?

- How do you choose private health insurance deductible?

- German healthcare expenditure

- Private health insurance for the unemployed in Germany

- Private health insurance for students in Germany

- Private health insurance for children in Germany

- Family health insurance in Germany

References

- https://www.kv-fux.de/private-krankenversicherung/uebertragungswert/

- https://www.versicherung-vergleiche.de/private_krankenversicherung/lexikon/beitrag_pkv.htm

- https://www.axa.de/pk/gesundheit/s/beitragsentwicklung-ruhestand

- https://www.iges.com/kunden/gesundheit/forschungsergebnisse/2020/beitragsentwicklung-in-der-pkv/index_ger.html

- https://www.wip-pkv.de/fileadmin/DATEN/Dokumente/WIP-Kurzanalysen/WIP-Kurzanalyse-2023-Beitragseinnahmen-GKV_PKV_2023_2024.pdf

- https://www.pkv.de/wissen/beitraege/warum-die-beitraege-steigen/

- https://schlemann.com/krankenversicherung/ist-eine-private-krankenversicherung-im-alter-zu-teuer/