Key takeaways

- Private health insurance is cheaper for high earners and offers better coverage than public health insurance.

- Read our book on German healthcare to understand the German health system.

- Private insurance premiums increased on average by 3.9% per annum between 2015 and 2025. On the other hand, public health insurance costs increased on average by 4.1% per annum between 2015 and 2025

- Switching from private to public health insurance is tough and virtually impossible after 55.

This is how you do it

- Consider the criteria in this guide to decide if private health insurance is the right choice. You can also use our “Health Insurance Finder” tool to check which health insurance (Public or Private) makes sense and when.

- Consult a fee-based advisor or an insurance broker before choosing between private or public health insurance.

- In our comparison and test, we found Haellesche and Signal Iduna’s private health insurance plans to be the best.

Table of contents

What is private health insurance (Private Krankenversicherung) in Germany?

Every resident in Germany is legally required to have health insurance.

The German health insurance system is divided into two groups: private health insurance and public health insurance.

As the name suggests, private companies offer private health insurance.

The German government regulates private insurers. However, they don’t have as much control as they do on public health insurance.

As of 2023, 90% of the German population is insured under public health insurance. If you look further, 95% of the employed and 59% of the self-employed people living in Germany are insured under public health insurance (Statutory health insurance). [1]

Why does only 10% of the German population have private health insurance?

To qualify for private health insurance, you must earn above 73,800€ (as of 2025). This is called the income threshold, which was 69,300€ (as of 2024).

Around 85% of the German population earn below the income threshold. Thus, they don’t qualify for private health insurance. This is the main reason why 90% of German residents are insured under public health insurance.

German Healthcare Demystified – Free eBook

- The German healthcare system is complex. This is why we wrote this book to help you navigate it.

- Choosing health insurance is a life-long decision. If you pick the wrong plan, it may cost you dearly in the future.

- Learn what is covered in public and private health insurance and what is not.

- What supplement health insurance plans must you get based on your personal situation?

Who can take private health insurance in Germany?

You can use our “Health Insurance Finder” tool to check which health insurance (Public or Private) makes sense and when. We recommend getting advice from a fee-based advisor or health insurance broker before deciding.

Civil Servants

Civil servants can choose between private and public health insurance. However, private health insurance is more lucrative for civil servants as their employer covers 50% to 70% of the medical costs.

Thus, civil servants need private health insurance to cover the rest of the costs. This makes private insurance very cheap for them.

On the other hand, the state doesn’t offer any aid if the civil servant is insured by public health insurance. Only a few federal states contribute 50% of the public insurance premium.

Self-employed

Full-time self-employed people can also choose between private and public health insurance. Unlike employees, how much you earn doesn’t matter.

Only the freelancers pursuing artistic or journalistic work are the exception. They are subject to compulsory statutory health insurance under the Artists’ Social Insurance Fund (Künstlersozialkasse (KSK) in German).

Check out our guide on private health insurance for self-employed to learn more.

Employee

Employees earning below the income threshold are insured under compulsory public health insurance. The income threshold is 73,800€ (as of 2025).

Employees earning above the income threshold can choose between private or public health insurance. The income threshold is called Beitragsbemessungsgrenze in German. The German government sets this limit, which is revised every year.

The income threshold includes

- your gross salary,

- vacation bonus (Urlaubsgeld),

- and Christmas bonus (Weihnachtsgeld).

The income threshold doesn’t include special payments such as profit distributions.

Students

Students must decide on their health insurance at the start of their university studies.

You can choose private health insurance or public health insurance at the start of your study. However, you cannot change it during your study period.

You can change your health insurance again when

- you get full-time employment for the first time after graduation.

- you turn 30 during your studies

Suppose you had private health insurance during your studies and became self-employed immediately after graduating. In this case, you must remain privately insured, regardless of how much you earn.

Private health insurance is worth it for students whose parents are civil servants. This is because children of civil servants who have private health insurance receive up to 80% of medical aid.

But you receive civil servant aid till you are 25 or till your parents get child support.

Book a free call with a health insurance expert

- German health insurance is a complicated product. There are several factors that must be considered before deciding which health insurance is best for you. An expert can guide you and help you pick the best option for you.

- An Insurance broker is liable for their advice. This means if the policy they recommended doesn’t offer the coverage you requested, they are liable to pay the damages incurred in the future.

For whom private health insurance makes sense?

Private health insurers offer more comprehensive medical services than statutory health insurers. However, one must be aware of a few things before taking private health insurance.

- Unlike public health insurance, private health insurance premiums don’t depend on your income. So, even if your income decreases, the insurance premium will continue to rise. The private health insurance premium has increased on average by 3.9% per annum between 2015 and 2025

- Switching from private to public health insurance is tough.

- Switching private health insurance providers is expensive.

You can use our “Health Insurance Finder” tool to check which health insurance (Public or Private) makes sense and when. We recommend getting advice from a fee-based advisor or health insurance broker before deciding.

Health insurance finder

Determining which health insurance is right for you can be confusing. So, we created this tool to help you decide.

Answer a few questions, and the tool will tell you which health insurance best suits your current situation.

Here are some criteria that can help you decide between private and public health insurance.

Both you and your partner are high-earners

If your partner and you earn a high income, private health insurance is a better choice. You get better services and pay less than public health insurance.

Are you under 40?

Private health insurance premiums depend on your age and health at the time of taking the insurance. Thus, experts recommend getting private health insurance when you are young and healthy.

Retirement provisions

To keep the private health insurance premiums stable, part of your contributions go into so-called retirement provisions. The retirement provisions ensure the insurance premium doesn’t get too high in old age.

However, you must contribute to the retirement provision long enough for it to make a difference. Thus, enrolling in private insurance when you are young is critical.

You should only consider private health insurance in old age if you can afford a high monthly premium after retirement.

Are you self-employed with a high income?

Employers pay 50% of the employees’ health insurance contributions. However, the self-employed must pay the whole contribution themselves.

Thus, self-employed people end up paying approximately 50% more in insurance premiums than employees with the same income. Hence, self-employed people with a private health insurance policy can save a couple hundred euros monthly.

But again, consider other factors, such as your family status, health condition, and age, before choosing private health insurance.

Do you have health problems?

Private insurers have the right to choose their customers. Hence, they either reject the applicants with prior health problems or charge a high premium.

It’ll be difficult to get a cheap private health insurance if you have one or more of the following illnesses:

- High blood pressure,

- Cardiovascular problems,

- Diabetes,

- Asthma,

- allergies,

- back problems,

- spinal diseases,

- physical or mental disabilities.

Are you a civil servant?

The state covers 50% to 70% of the medical bills of privately insured civil servants in Germany. Hence, civil servants need a health insurance policy to cover the rest. This makes private health insurance very cheap for them.

This is why civil servants can save hundreds of euros every month with private health insurance.

Are you planning to have a family in the future?

Private health insurance doesn’t cover your family, i.e., spouse and children, for free. You have to take their health insurance separately.

On the other hand, public health insurance covers your family for free.

Moreover, you must continue to pay the private health insurance premium during parental leave. In the public system, however,

- your partner’s insurance will cover you during the parental leave,

- or the insurance premium will decrease during the parental leave.

Thus, public health insurance makes sense if you are the sole earner in the family.

Conclusion

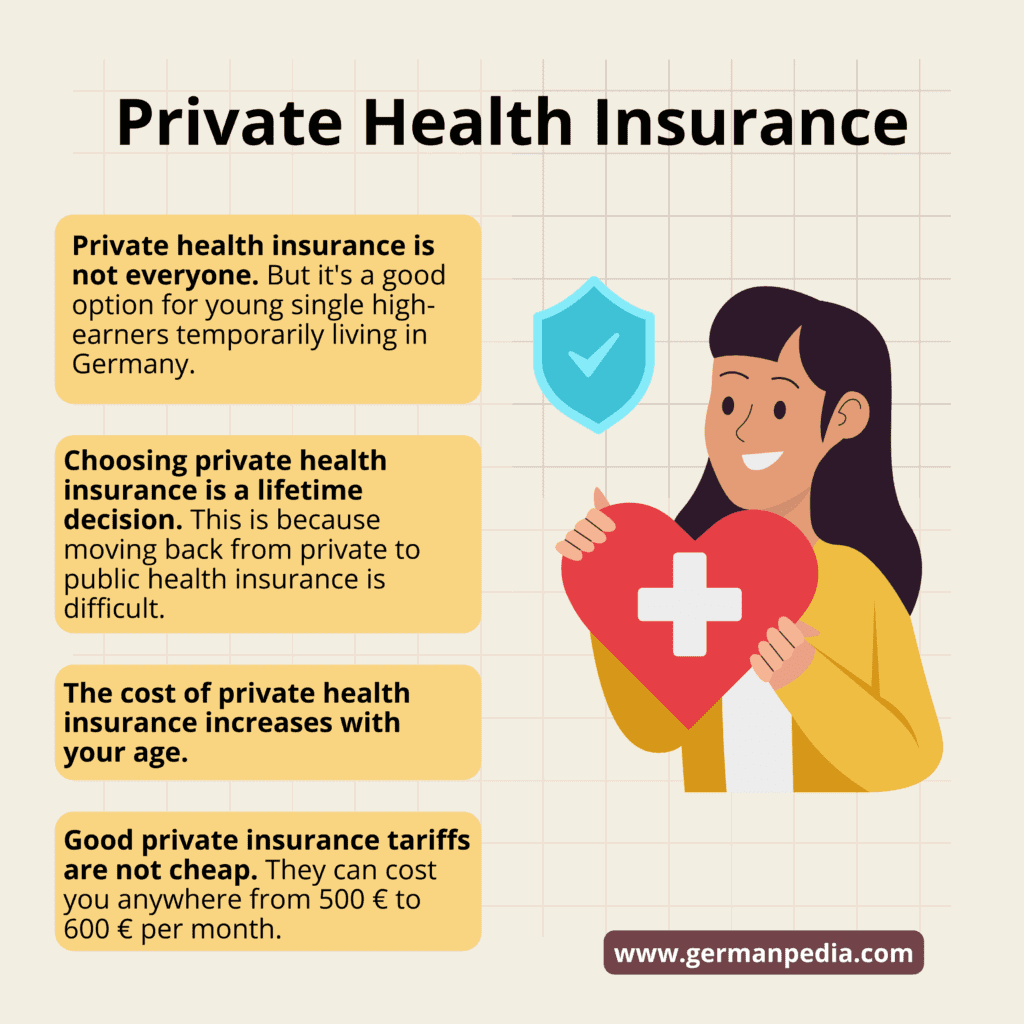

- Private health insurance is not for everyone. But it’s the only option if you seek the best medical coverage in Germany.

- Choosing private health insurance is a lifetime decision. This is because moving back from private to public health insurance is difficult.

- Good private insurance tariffs are not cheap. They can cost you anywhere from 500 € to 600 € per month. Additionally, you pay for each family member’s health insurance.

- The cost of private health insurance increases with time. The private insurance premiums increased 3.2% per annum during the savings phase and 2.3% after retirement between 2014 and 2024. So, a 35-year-old whose insurance premium starts at 650 € per month (as of 2024) will pay 1670 € per month by the time they are 65 (as of 2054). The premium will continue to increase and will be more than 2000 € per month by the time you are 85 (as of 2074). However, it’s the same with public health insurance. Moreover, you’ll pay more in the public system if you are a high earner (even after retirement). Read more about health insurance premium development here.

- Reduce private health insurance costs. If you can no longer afford your private health insurance premiums, you can switch to a cheaper tariff offered by your insurer. Read our guide on how to reduce private health insurance costs to learn more.

Advantages of private health insurance

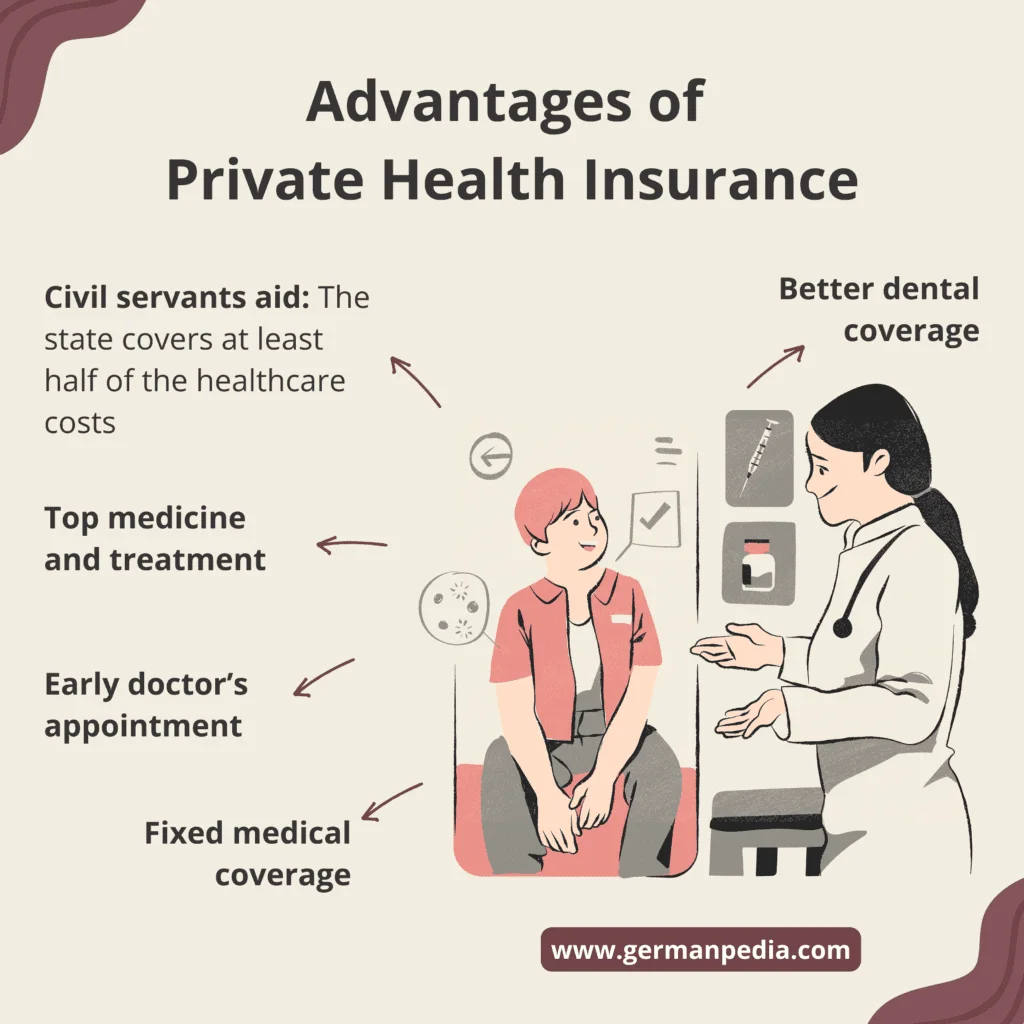

- Civil servants aid. The state covers at least half of the healthcare costs for civil servants with private health insurance, even after retirement. You need private health insurance to cover the remaining costs. It is also called residual cost insurance. This makes private insurance very cheap for civil servants.

- Top medicine and treatment: Good private insurance tariffs cover the cost of top medicine and treatment by a specialist in a private clinic or abroad.

- Early appointment: Privately insured patients receive appointments on the same day or within a week. On the other hand, publicly insured patients wait between 4 and 7 months to get a specialist’s appointment. This is because doctors often receive more money for the same treatment from a private patient than from a statutory health insurance patient.

- Fixed medical coverage: You agree on the services your private health insurance policy will provide initially. Health insurance companies cannot change the services agreed upon later. However, public health insurers can reduce or cancel some of the services covered, as seen in the past.

- Better dental coverage: Private insurance tariffs usually offer better dental care than public insurance. Usually, privately insured individuals don’t need supplementary dental insurance. However, experts recommend publicly insured individuals to get supplementary dental insurance.

You can learn more in our guide on services private health insurance offers that you don’t find in statutory health insurance.

Disadvantages of private health insurance

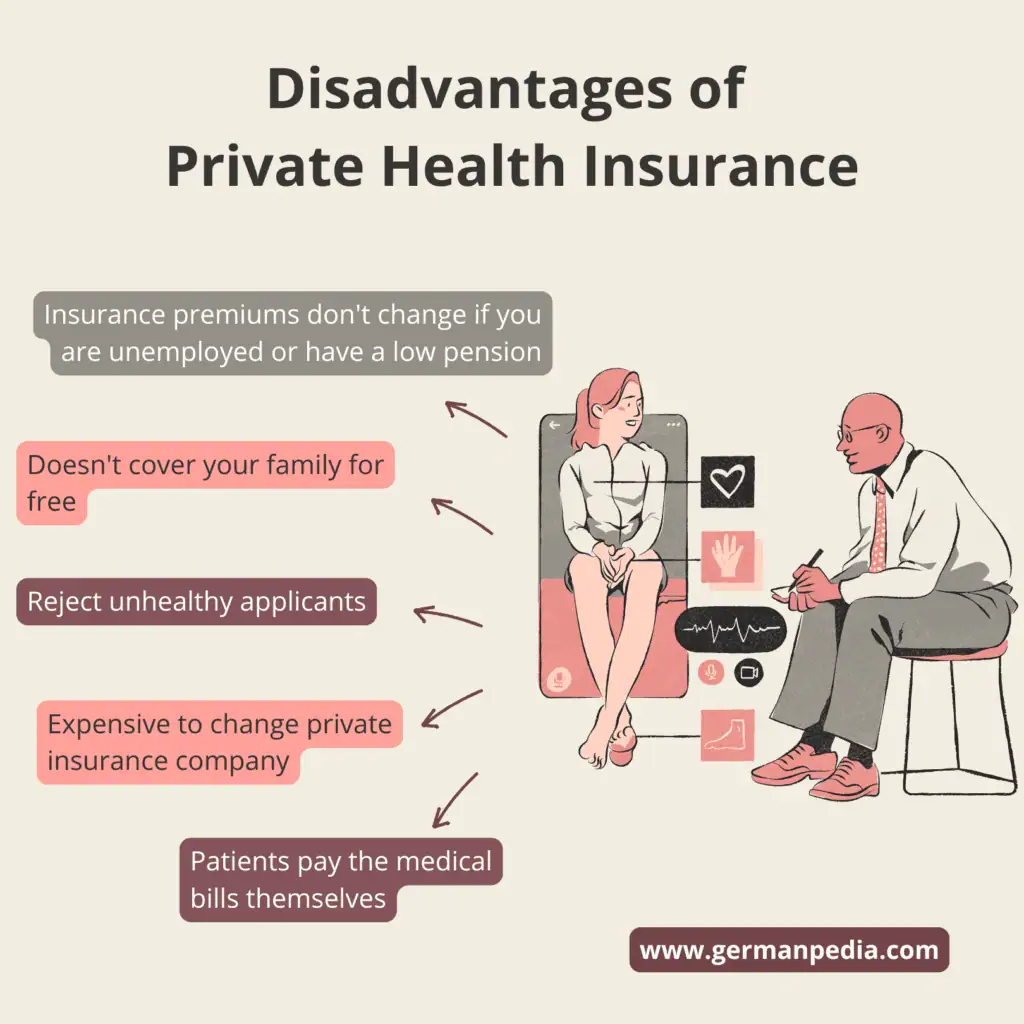

- Premium of private insurance doesn’t depend on your income. So, even if your income decreases or you become unemployed, you’ll continue to pay the same premium.

- Private health insurers reject unhealthy applicants. Private insurers perform a health check before accepting a new customer.

- It’s difficult to change the private health insurance plan. Suppose you want to change the services offered by your private insurance plan. You may have to go through a complete health check again. If the health check shows any existing diseases, you’ll end up paying a high premium.

- Premiums in the private healthcare system increased by an average of 2.8% per annum between 2004 and 2024 and 3.9% per annum between 2015 and 2025.

- Private insurance premiums don’t change if you are unemployed or have a low pension. Low income may mean you cannot afford private insurance contributions. It may force you to switch to the basic plan that offers fewer services.

- Divorce from a civil servant spouse may prove expensive. The state stops providing subsidies to the divorced spouse of a civil servant. Hence, you must take out full private health insurance on your own. Thus leading to high private insurance premiums.

- Private healthcare insurance doesn’t cover your family for free. You must take private health insurance for every individual. It doesn’t matter if they earn or not. However, the statutory health insurance system covers non-earning family members for free.

- Stuck to a private insurance company for life. It’s not economically worthwhile to switch to another private insurer. This is because only part of the retirement provisions (approximately 70%) can be taken to the new insurer. Moreover, the insurance premium will be higher at the new insurer. The reason is your age. You’ll be older than when you took the insurance from the previous insurer.

- Patients with private health insurance pay the medical bills themselves. Later, the private insurer reimburses the costs. However, you don’t pay the bills for inpatient treatments. Hospitals bill them via a health insurance card, similar to statutory health insurance.

Services good private health insurance must cover

We have created a checklist that you can use while finding private insurance.

You can also use this checklist during your consultation with an insurance broker. We recommend you make notes and have your broker sign the checklist after the consultation.

This way you can be sure that you have discussed all the important points and have understood everything correctly.

If you are unsure about private and public health insurance after your consultation with the insurance broker, you can consult a fee-based advisor.

Fee-based advisors don’t receive a commission if you take out private health insurance. You pay them instead. This ensures that you get an unbiased advice.

You pay between 150 and 200 euros per hour for a consultation with a fee-based insurance advisor. But this fee is worth it as you are making a lifelong decision.

You can find insurance advisors here. Ensure that the advisor specializes in private health insurance.

NOTE: You must not compromise on private health insurance coverage to reduce the insurance cost.

You can read our guide on private health insurance services in Germany to learn more.

Private health insurance services checklist

- A comprehensive list of services good private insurance should cover.

- Use it during your consultation with an insurance broker or a fee-based advisor.

- Use it while searching for a private health insurance policy.

Cost of private health insurance in Germany

The cost of private health insurance depends on your tariff, age, and health at the time of taking the policy. The private insurance costs for people in different age groups and professions if they take it in 2025.

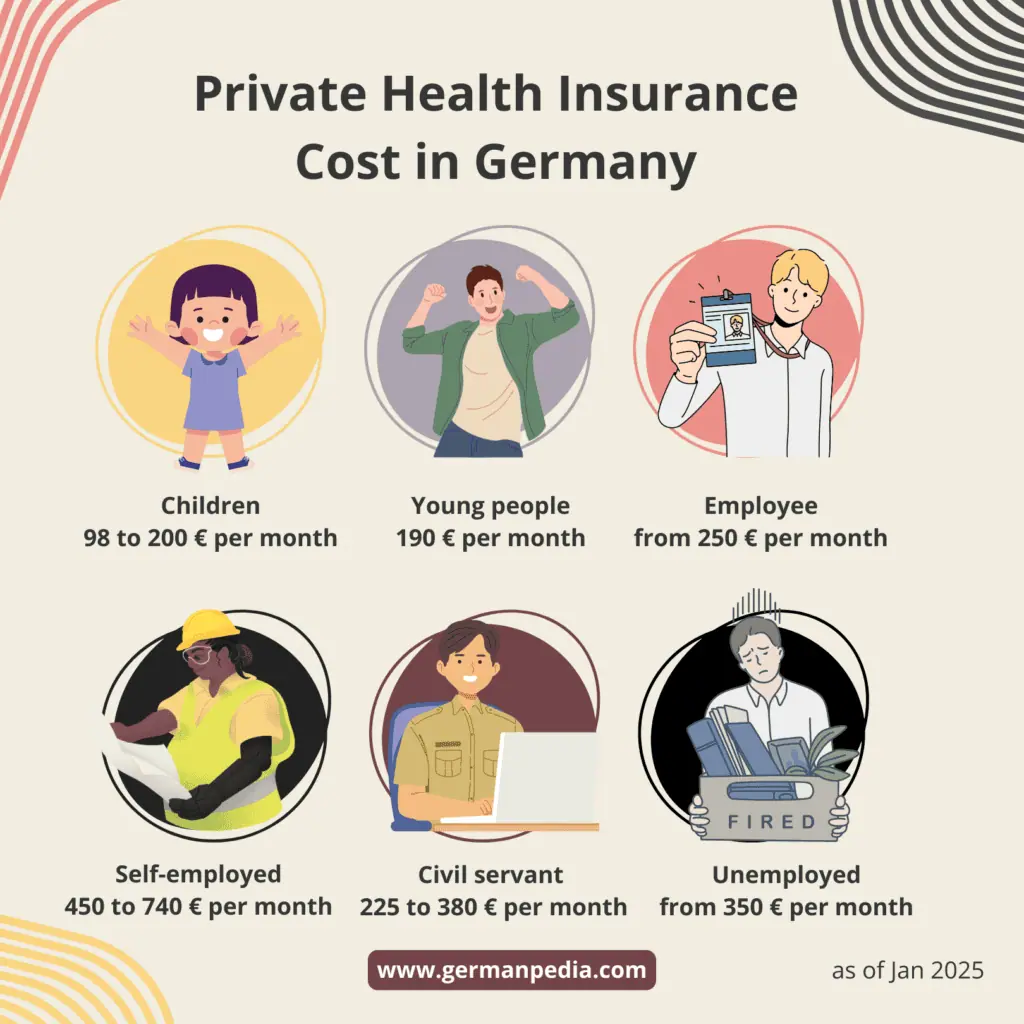

- Children insured by their parents: between €98 and €200 per month. Your employer also contributes to your child’s premium, but there is a maximum limit.

- Young employee: starting from €250 per month (after deducting the employer’s contribution).

- 35-year-old employee: between 301 € and 430 € per month (after deducting the employer’s contribution)

- Self-employed: between 563 € and 830 € per month

- Civil servant (Beamter in German) with 50% subsidy: between 325 € and 440 € per month

- Civil servant (Beamter in German) with 70% subsidy: between 256 € and 330 € per month

- Not working: It doesn’t matter if you are not employed; private health insurance premiums do not depend on your income.

NOTE: The cost of private health insurance doesn’t increase if you get sick after taking the insurance.

You can learn more about the costs in our guide on health insurance costs in Germany.

Can you cancel private health insurance anytime?

Yes, you can cancel your private health insurance policy by sending a written cancellation request to your insurance provider within the notice period.

The notice period for most health insurers is three months before the end of the “insurance year.”

You can use our sample private health insurance cancellation letter to cancel your policy. You can download it here for free.

Sample letter to terminate the health insurance contract

- Download the sample termination letter written in German and English.

- You can use the letter as it is. You only need to fill in your details.

- The letter is available in both docx and pdf formats. Hence making it easy to modify.

German law requires everyone in Germany to have a health insurance policy. Thus, to cancel your health insurance policy, you must prove the following to your current insurer.

- You have a new German health insurance policy.

- You’ll remain insured without interruption.

In short, you cannot cancel your current health insurance policy without proof of a valid new policy.

In special situations like an increase in insurance premium, you can cancel the contract within two months after receiving the letter. Moreover, you can cancel the contract immediately if you leave Germany permanently.

Private health insurance companies can also terminate your contract if you breach the contract terms or provide misleading information when applying.

Where can you get advice on the German health insurance system?

As you know, purchasing private health insurance is a lifetime decision. So, before making a decision, you should consult with a fee-based advisor (Versicherungsberater in German) or a health insurance broker (Versicherungsmarkler in German).

You pay fee-based advisors on an hourly basis. Insurance brokers get a commission from the insurance company.

Both insurance brokers and fee-based advisors are liable for their advice. This means that if you asked for a particular coverage and the insurance policy recommended by the broker or the advisor didn’t cover it, they are liable to pay you the damages.

The consultation fee of a fee-based insurance advisor is between 150 and 200 € per hour.

You should never get insurance advice from insurance agents. They represent a single insurance company, and their goal is to sell as many insurance policies of that company as possible. Moreover, they are not liable for their advice.

We recommend getting free advice from an insurance broker first. If you are not satisfied, contact a fee-based advisor.

You can book a free call with the insurance broker we recommend or find a fee-based insurance advisor here.

Advantages of consulting an insurance broker or fee-based advisor

- If you inquire about private health insurance yourself and get rejected, the insurer may enter you in the “information and advice system (Hinweis- und Informationssystem (HIS))” of the German insurance industry. This will make it difficult for you to get insurance from other providers.

- Insurance brokers or advisors can make an anonymous pre-inquiry on your behalf. This way, your personal details, such as name, address, etc., are hidden from the insurer. Thus, even if the insurer rejects your application, no entry can be made in the HIS.

- Finding good private health insurance is not easy. Insurance companies differ in their benefits and acceptance criteria. Depending on your state of health, one insurance company may reject you, but another may accept you under normal conditions.

- An insurance broker or fee-based advisor can help you find the best private health insurance plan with good conditions.

Book a free call with a health insurance expert

- German health insurance is a complicated product. There are several factors that must be considered before deciding which health insurance is best for you. An expert can guide you and help you pick the best option for you.

- An Insurance broker is liable for their advice. This means if the policy they recommended doesn’t offer the coverage you requested, they are liable to pay the damages incurred in the future.

Best private health insurance companies in Germany

In our comparison and test, we found Allianz, LVM, and Signal Iduna private health insurance companies among the best.

Private health insurance is a complicated product. So, we recommend consulting a fee-based advisor or an insurance broker for personalized advice.

Best private health insurance tariffs in Germany

Here are the private health insurance plans that were rated the best by Handelblatt and Morgen & Morgen.

| Basic protection | Standard protection | Top protection |

|---|---|---|

| Hallesche “NK.select S Bonus, NK.select Flex URZ” | Allianz (GSP70) | Hallesche “NK.select XL Bonus, URZ” |

| Hallesche “NK.select L Bonus, URZ” | UKV (GesundheitVario) | |

| uniVersa (uni-top) | ||

| Allianz (GSB70) |

Filing a complaint against your private health insurer

The top two complaints against private insurers by patients are

- Was the treatment medically necessary?

- The medical bills are too high.

Your first point of contact when filing a complaint is the insurance ombudsman. The ombudsman acts as an arbitration board for disputes with private health insurance.

Unfortunately, many disputes related to private health insurance end up in court. In 2023, the ombudsman was able to resolve only one out of every 5 cases. Thus, taking legal protection insurance is critical here.

NOTE: Never take legal and private health insurance from the same company.

German Healthcare Demystified – Free eBook

- The German healthcare system is complex. This is why we wrote this book to help you navigate it.

- Choosing health insurance is a life-long decision. If you pick the wrong plan, it may cost you dearly in the future.

- Learn what is covered in public and private health insurance and what is not.

- What supplement health insurance plans must you get based on your personal situation?

More topics

- Best private health insurance as per top rating agencies

- Private health insurance costs in Germany

- Private vs public health insurance

- Private health insurance cost in old age

- Why is private health insurance cheaper than public health insurance?

- Employer’s contribution to private health insurance

- Private health insurance for self-employed

- Health insurance for students

- Health insurance for children

- Healthcare in Germany

- Best public health insurance in Germany

References

- https://www.finanztip.de/pkv/

- https://www.pkv.de/wissen/private-krankenversicherung/leistungen-und-erstattung/

- https://www.test.de/Private-Krankenversicherung-Alles-was-Sie-wissen-muessen-5353750-0/

- https://www.pkv.de/wissen/private-krankenversicherung/

- https://www.bundesgesundheitsministerium.de/private-krankenversicherung