Key takeaways

- Private health insurance costs depend on your age, health, and the insurance services you opt for.

- Public health insurance costs depend on your income.

- A good private health insurance costs between (as of 2025)

- Children insured by their parents: between €98 and €200 per month. Your employer also contributes to your child’s premium, but there is a maximum limit.

- Young employee: starting from €250 per month (after deducting the employer’s contribution).

- 35-year-old employee: between 301 € and 430 € per month (after deducting the employer’s contribution)

- Self-employed: between 563 € and 830 € per month

- Civil servant (Beamter in German) with 50% subsidy: between 325 € and 440 € per month

- Civil servant (Beamter in German) with 70% subsidy: between 256 € and 330 € per month

- Private health insurance doesn’t cover your family for free. You must get separate health insurance for your spouse and children.

- You can insure your non-working spouse and children for free with public health insurance.

This is how you do it

- You should know what good private health insurance covers before signing a contract.

- Private insurance is not automatically better than public. Compare them to weigh in the pros and cons.

- We recommend getting private health insurance via an insurance broker. They are experts and can help you find the best plan for your needs. You can book a call with an expert we recommend here.

- You can use our “Health Insurance Finder” tool to check which health insurance (Public or Private) makes sense and when.

- In our comparison and test, we found Haellesche, Allianz, and Signal Iduna’s private health insurance plans to be the best.

Table of contents

Cost of public health insurance in Germany

The cost of public health insurance depends on your income and occupation.

You can use our public health insurance cost calculator to easily calculate the premium you’ll pay based on your income and occupation.

Public Health Insurance Cost Calculator

- Calculate how much different public health insurance companies cost.

- You can check if you are insured with the cheapest public health insurance.

- Calculate how much you can save by switching to cheaper public health insurance.

Employed

Employees pay 14.6% of their gross income into the public health insurance system every month. On top of it, there is an additional contribution (Zusatzbeitrag in German).

The public health insurance company determines the additional contribution. The average additional contribution is 2.5% (as of 2025).

The German government has set a maximum limit on income to be considered when calculating the insurance cost. This is 5,512.5 € per month (as of 2025).

You also contribute to nursing care insurance (Pflegeversicherung). People with no children pay 4.2% of your gross monthly salary (as of 2025) into nursing care insurance. And people with one child pay 3.6% of your gross monthly salary (as of 2025).

The long-term nursing care insurance percentage reduces with each additional child. It’s 3.35% if you have two children and 2.6% if you have five children.

So, the total public health insurance premium you pay is

| Maximum income considered for calculating premium | 5,512.5 € per month (as of 2025) | |

| Percentage of your gross salary | Monthly premium | |

| General contribution | 14.6% | 804.8 € |

| Additional contribution (Zusatzbeitrag) | 2.5% (average) | 137.8 € |

| Long-term nursing care | 3.6% (with 1 child) 4.2% (no children) | 198.4 € (with 1 child) 231.5 € (no children) |

| Total monthly contribution | 20.7% (with 1 child) 21.3% (without children) | 1141 € (with 1 child) 1174.16 € (without children) |

The good news is that your employer pays half the public health insurance premium in Germany.

German Healthcare Demystified – Free eBook

- The German healthcare system is complex. This is why we wrote this book to help you navigate it.

- Choosing health insurance is a life-long decision. If you pick the wrong plan, it may cost you dearly in the future.

- Learn what is covered in public and private health insurance and what is not.

- What supplement health insurance plans must you get based on your personal situation?

Self-employed

The public health insurance premium for the self-employed is the same as that for the employed. The only difference is that the self-employed must cover the entire health insurance cost on their own. This is why many self-employed individuals pick private health insurance over public health insurance.

We recommend getting private health insurance via an insurance broker. They are experts and can help you find the best plan for your needs. You can book a call with an expert we recommend here.

Self-employed individuals have two options:

- Public health insurance without sick pay (Contribution = 14% of their gross income)

- Public health insurance with sick pay (Contribution = 14.6% of their gross income)

The self-employed also pay the additional contribution and long-term care insurance like the employed.

| No sick pay | Sick pay | |||

| Have 1 child | No kids | Have 1 child | No kids | |

| General contribution | 14.0% | 14.6% | ||

| Average Additional contribution | 2.5% | |||

| Nursing care insurance | 3.6% | 4.2% | 3.6% | 4.2% |

| Total contribution | 20.1% | 20.7% | 20.7% | 21.3% |

| Maximum income considered for calculating premium | 5,512.5 € per month (as of 2025) | |||

| Total monthly contribution | 1108€ | 1141€ | 1141€ | 1174€ |

Civil servant

Civil servants pay 14% of their gross income to public healthcare insurance. They must also pay the additional contribution (Zusatzbeitrag) and nursing care insurance like the employees.

Like self-employed people, civil servants must cover the entire insurance cost on their own. However, the following federal states cover half the insurance costs.

- Thüringen

- Baden-Württemberg

- Berlin

- Brandenburg

- Bremen

- Hamburg

- Niedersachsen

- Sachsen

- Schleswig-Holstein

Student

Student health insurance premium depends on your age and number of children. You are eligible for discounted student health insurance if you are under 30.

Students who are 30 or above no longer get discounted student health insurance. Read our guide on student health insurance to learn more.

| Percentage of your gross salary | Monthly premium (Age: under 30) (from 01.10.2024) | Monthly premium (Age: 30 or above) (from 01.10.2024) | |

| BAföG rate for students (This is the rate used to calculate student health insurance premiums) | 855 € | Student rate no longer applies. Premium depends on your income. The minimum income considered is 1248.33 € | |

| General contribution | 10.22% | 87.38 € | 127.58 € (10.22% of 1248.33) |

| Additional contribution (Zusatzbeitrag) | 2.5% (average) | 21.37 € | 31.21 € |

| Long-term nursing care | 3.6% (with 1 child) 4.2% (no children) | 30.78 € (with 1 child) 35.91 € (no children) | 44.93 € (with 1 child) 52.43 € (no children) |

| Total monthly contribution | 16.32% (with 1 child) 16.92% (without children) | 139.53 € (with 1 child) 144.66 € (without children) | 203.72 € (with 1 child) 211.21 € (without children) |

Unemployed

If you are unemployed, you have the following options.

- Insure yourself for free under your spouse’s public health insurance.

- If you get Arbeitlosgeld or Bürgegeld, you don’t pay the insurance premium and still get the full coverage.

- If none of the above cases applies, you pay the minimum contribution of 279.6€ per month (as of 2025).

Retired/Pensioners

The health insurance premium calculations for retirees depend on several factors. You can learn about it in our guide on public health insurance for pensioners in Germany.

Here is how much you pay for public health insurance after retirement.

- General contribution: 14% (don’t pay sick pay contributions anymore)

- Additional contribution: 2.5% (as of 2025)

- Long-term care insurance contribution: 4.2% of your gross monthly salary (as of 2025) (no kids) and 3.6% of your gross monthly salary (as of 2025) (1 child).

- Total: 21.3% (no children)

- You get a health insurance subsidy from your pension insurance.

- The income considered for calculating the premium varies based on how long you were insured in the public health system during your work life.

Register with TK

- Biggest public health insurance company in Germany based on number of members.

- Enjoy low premiums

- Get English customer support, website, and mobile app.

- Complete the application process in English.

Cost of private health insurance in Germany?

Private health insurance premiums don’t depend on your income. The private health insurance cost is based on the following factors.

- Age: The older you are, the more expensive the private insurance plan

- Health: Private health insurance providers do a complete health check before accepting a new customer. The premium for private health insurance is lower for healthy individuals. A private insurer adds a risk surcharge to your insurance premium if you have an existing disease.

- Services: You can select which services you want in your health insurance. The better services you opt for, the more the private insurance cost.

We used comparison portals to find the cost of different private health insurance plans in Germany. Here are our assumptions while looking for a private health insurance policy.

- You have no prior health problems

- You are 35 years old

- You earn more than the income threshold, i.e., 73,800€ (as of 2025)

The filters we used during our search

- We set the maximum deductible to 500 € per annum.

- The daily sickness allowance should be at least 100€ paid from the 43rd day.

- Shared room or 2-bed room in the hospital.

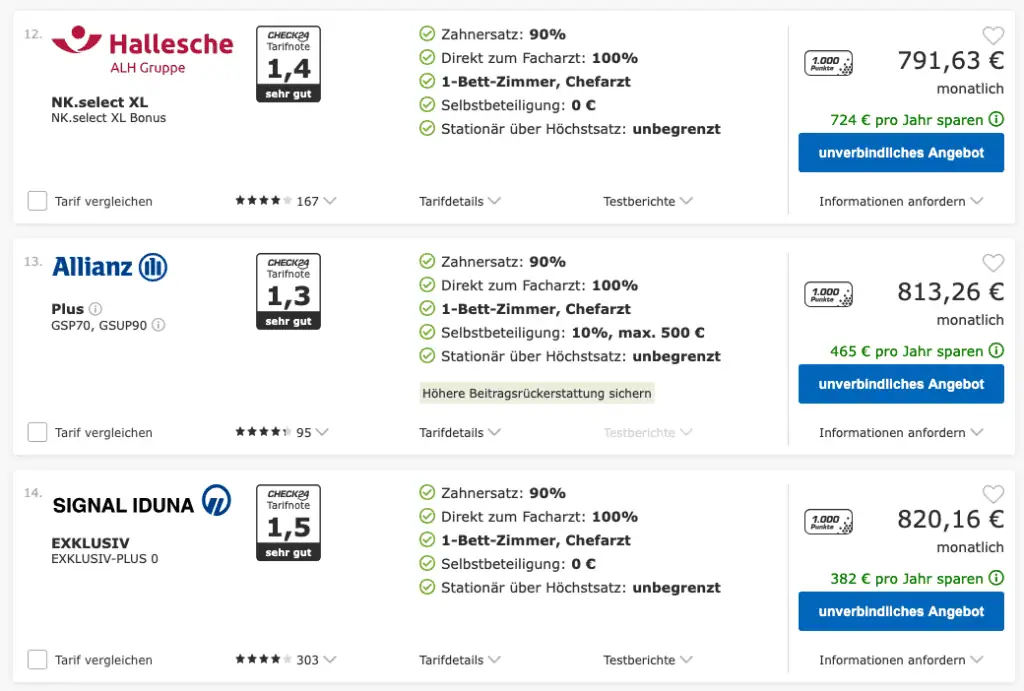

The private health insurance premium varies based on your occupation. Here is what we found.

Self-employed

The private health insurance cost between 563 € and 830 € per month (as of Feb 2025).

At this cost, you get the following services.

- The private insurer reimburses 80% to 90% of the dental treatment costs.

- You can go directly to a specialist. You don’t need a “Überweisung” from the general practitioner (Hausartz).

- The deductible is zero for “premium” private health insurance plans that cost 683 € per month. And it’s 300€ and 500 € for cheaper plans.

- The private health insurance provider will reimburse the cost of a 1-bed room during your stay at the hospital.

- The head doctor will treat you in the hospital.

NOTE: Just because your insurance provider reimburses the costs of a head doctor doesn’t mean the doctor will be available to treat you.

Employed

The private health insurance cost between 301 € and 430 € per month (as of Feb 2025) for employees. Private health insurance premiums are low as your employer pays half.

So, in reality, private health insurance costs between 602 € and 860 € per month. At this cost, you get the same services as the self-employed.

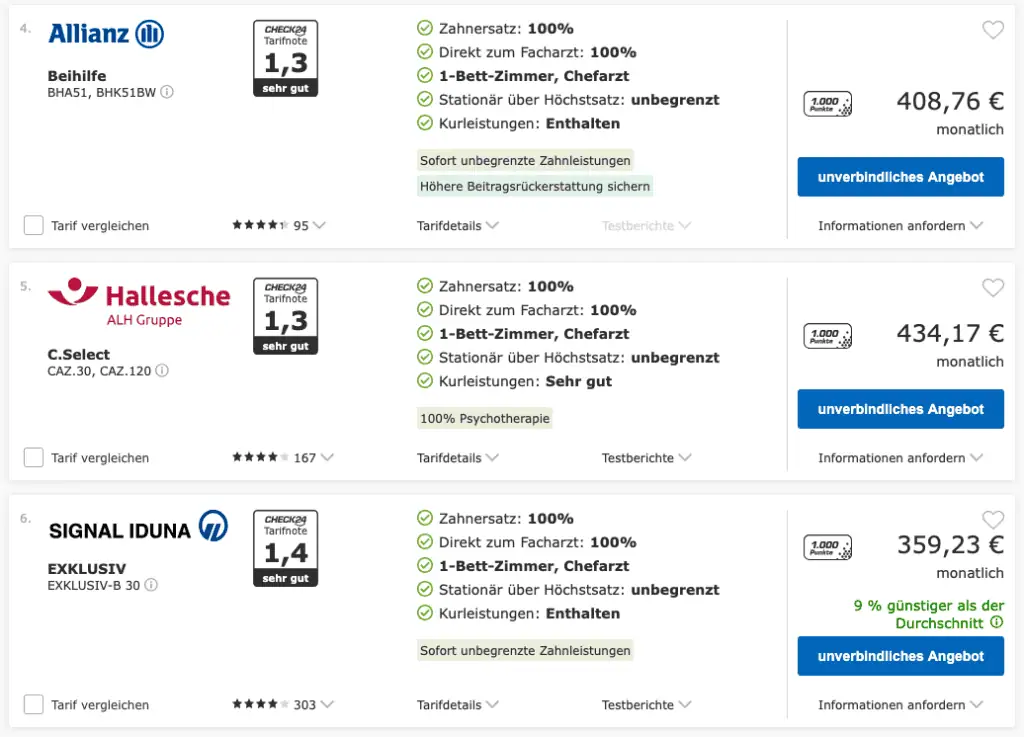

Civil Servant

The federal state covers 50% to 70% of civil servants’ medical bills. Thus, civil servants need supplementary health insurance to cover the rest of the costs. This makes private health insurance very cheap for civil servants.

Assuming you get a 50% subsidy from the state, you pay between 325 € and 440 € per month into the private health insurance system.

Civil servants not only get cheaper insurance but also better services.

- 100% dental coverage

- Visit a specialist directly

- 1-bed room during hospital stays

- Treatment by the head doctor

If you plan to get private health insurance, you should do so before you turn 45. We have created a checklist you can use to ensure that your private health insurance plan has all the essential services.

Private health insurance services checklist

- A comprehensive list of services good private insurance should cover.

- Use it during your consultation with an insurance broker or a fee-based advisor.

- Use it while searching for a private health insurance policy.

We recommend getting private health insurance via an insurance broker. They are experts and can help you find the best plan for your needs. You can book a call with an expert we recommend here.

Insurance brokers and advisors are liable for their advice. This means that if the insurance plan they recommended doesn’t fulfill your wishes, they are liable to pay the damages.

Insurance brokers offer free advice. The insurance company pays them upon the successful conclusion of the contract.

An insurance broker can also help you file a claim with the provider. The broker we recommend has been offering services to expats for more than a decade.

Book a free call with a health insurance expert

- German health insurance is a complicated product. There are several factors that must be considered before deciding which health insurance is best for you. An expert can guide you and help you pick the best option for you.

- An Insurance broker is liable for their advice. This means if the policy they recommended doesn’t offer the coverage you requested, they are liable to pay the damages incurred in the future.

Family health insurance premium in Germany

Public health insurance premium for a family

Your spouse and children are covered for free under statutory health insurance. The prerequisite is that your partner doesn’t earn or earn below 535€ (as of 2025).

If you both earn, you and your partner must pay into the public health insurance system.

Private health insurance premium for a family

In a private health system, you must take out a separate health insurance policy for each family member. Moreover, you must continue paying the private health insurance premium during maternity leave.

So, private health insurance gets expensive quickly for families. However, the situation is different for the civil servant’s family.

The state gives civil servants an 80% subsidy for children and 70% for spouses on private health insurance.

Increase in health insurance cost

Thanks to inflation, medical treatment costs are increasing and will continue to rise in the future. Thus, an increase in both public and private health insurance costs is inevitable.

You can learn more in our guide on how the cost of private and public health insurance will develop in the future (forecast).

Increase in the public health insurance cost

The statutory health insurance premium increased by 4.1% per annum between 2015 and 2025. And 3.8% per annum between 2005 and 2025.

However, you feel the price changes the most if you are a high earner.

Increase in the private health insurance cost

The private health insurance cost increased by 3.9% per annum between 2015 and 2025. And 3.1% per annum between 2005 and 2025.

| Year | Increase in the public health insurance cost | Increase in the private health insurance cost |

| 2005 to 2025 (Two decades) | 3.8% annually | 3.1% annually |

| 2015 to 2024 (One decade) | 4.1% annually | 3.9% annually |

How do you interpret the increase in health insurance costs?

As you can see, public insurance costs increased more than private insurance. However, you must understand how the costs of the two healthcare systems are calculated.

Each year, the German government increases

- the maximum income public insurers consider when calculating the premium and

- the percentage of your gross salary you contribute to the public system.

When the percentage of the gross salary increases, it affects everyone. However, an increase in the “maximum income considered for premium calculation” affects the people earning above that threshold.

So, if your income is not increasing or is below the threshold, your public insurance premium will not increase that much.

On the other hand, private health insurance costs don’t depend on your income. So, even if your income is not increasing, the insurance premium will continue to rise.

This is why you should always consider the long-term perspective when deciding between private and public insurance.

NOTE: High earners pay more premiums for public health insurance than private. Read our guide on health insurance premium development in the past and future forecasts to learn more.

How do health insurance costs develop as you get older?

Germany has an aging population. Rising medical costs and the aging population have put pressure on its health insurance systems.

Hence, it’s safe to assume that health insurance costs will continue to rise. It doesn’t matter if you are in public or private health insurance, you’ll pay a higher premium in the future.

High earners

High earners usually pay the same or less for private health insurance after retirement than public health insurance. It’s because private health insurance companies save part of your contributions as aging provisions.

The insurer uses this saved amount to compensate for the increased medical costs when you are old. This way, your premium in private health insurance stays stable or decreases after retirement.

NOTE: Based on our calculations, an average high earner (self-employed) pays around 250,000€ more in the public health system as compared to private health insurance over 32 years.

Low earners

Low earners pay less in the public healthcare system than in private. It’s because, in public health insurance, the premium depends on your income.

If you earn less, you have a lower monthly contribution.

Read our guide on health insurance premium development in the past and future forecasts to learn more.

Can you reduce the costs of health insurance in Germany?

Public health insurance

Statutory health insurance costs depend on income. If you are a high earner and don’t want to pay high premiums, you can switch to private health insurance.

Another option is to switch public health insurance providers. Each public insurer is free to set an additional contribution percentage.

So, you can reduce your public insurance premium by opting for an insurer with a lower additional contribution percentage.

You can use our public health insurance cost calculator to check how much you can save by moving to a cheaper health insurer.

We find TK to be the best public health insurance company for expats. It’s one of the cheapest insurers and offers English customer support.

Register with TK

- Biggest public health insurance company in Germany based on number of members.

- Enjoy low premiums

- Get English customer support, website, and mobile app.

- Complete the application process in English.

Private health insurance

Here are the options to reduce the private health insurance premiums.

- Switch to a cheaper tariff. A private health insurance company offers several insurance plans. So, you can always switch to a cheaper plan to reduce your monthly premium.

- Cancel services you don’t use from your private health insurance contract.

- Increase your deductible

- You can ask for a risk surcharge reassessment (Risikozuschlägen). Insurance companies add a risk surcharge for pre-existing conditions. So, you reduce your premium if your previous illnesses are now cured.

- Return to statutory health insurance.

Learn more in our guide on reducing private health insurance costs in Germany.

How do you pay medical bills in Germany?

Statutory health insurance members

In Germany, every public health insurance member gets a health insurance card. When you go to a doctor, you show your health insurance card for treatment. So, you don’t pay anything.

If you avail of a treatment not covered by public insurance, the clinic issues you a bill that you must pay. For example, professional teeth cleaning.

Of course, the doctor informs you in advance if the treatment is covered by public insurance.

The same applies to buying medication. Usually, the prescribed medication is covered by public health insurance, and you don’t pay anything at the pharmacy.

You have to pay a small amount per quarter for prescribed medicines. Over-the-counter medication is not covered in public insurance.

Private health insurance members

- Outpatient: Doctors give you a receipt for outpatient treatments. You must pay the medical bill within 10 to 14 days. You must submit the receipt to your private health insurance provider for reimbursement. Usually, the insurer reimburses the cost within a few days. But you are responsible for settling the medical bill.

- Pharmacy: At pharmacies, you must also pay the bill yourself. Later, you can submit the receipt to your private health insurer for reimbursement.

- Inpatient: Usually, the hospital can settle the treatment costs directly with the health insurer. However, sometimes, you might have to pay the bill and get reimbursed later.

We recommend consulting with your insurer before getting expensive medical treatment. Sometimes, the insurance provider doesn’t cover all the costs. So, it’s better to know what is covered and what isn’t to avoid surprises.

When does switching to private health insurance make sense in Germany?

Moving to private health insurance is a lifelong decision. So, you should consult a fee-based advisor or an insurance broker before making the decision.

You should educate yourself about the German healthcare system and then decide.

In general, private health insurance makes sense in the following situations.

- You are a young, single, high-earner living in Germany.

- You are a civil servant who gets a 50% to 70% subsidy from the state.

- For married couples, if both partners are high earners

You can use our “Health Insurance Finder” tool to check which health insurance (Public or Private) makes sense and when. We recommend getting advice from a fee-based advisor or health insurance broker before deciding.

Book a free call with a health insurance expert

- German health insurance is a complicated product. There are several factors that must be considered before deciding which health insurance is best for you. An expert can guide you and help you pick the best option for you.

- An Insurance broker is liable for their advice. This means if the policy they recommended doesn’t offer the coverage you requested, they are liable to pay the damages incurred in the future.

More topics

- Best private health insurance as per top rating agencies

- Switch from private to public health insurance

- Private vs public health insurance

- Private health insurance cost in old age

- Why is private health insurance cheaper than public health insurance?

- Employer’s contribution to private health insurance

- Private health insurance for self-employed

- Health insurance for students

- Health insurance for children

- Healthcare in Germany

- Best public health insurance in Germany

References

- https://www.wip-pkv.de/veroeffentlichungen/detail/entwicklung-der-praemien-und-beitragseinnahmen-in-pkv-und-gkv-aktualisierung-20232024.html

- https://www.bundesgesundheitsministerium.de/private-krankenversicherung

- https://www.check24.de/private-krankenversicherung/kosten/

- https://www.finanztip.de/pkv/pkv-kosten/

- https://www.transparent-beraten.de/gesetzliche-krankenversicherung/berufsgruppen/beamte/

- https://versicherungsvergleich-beamte.de/beamte-in-der-gesetzlichen-krankenkasse