Key takeaways

- Expats with valid visas and stable income sources can get a personal loan in Germany.

- When assessing your creditworthiness, banks consider factors like your Schufa score, income, expenses, types of insurance you have, existing loans, etc.

- Getting a personal loan makes sense if you plan to invest the loan amount in an asset that grows in value over time or if you need it to improve your life.

- The maximum personal loan you can take depends mainly on your income and expenses.

This is how you do it

- Compare the loan offers on comparison portals: Verivox*, Finanzcheck*, and Check24*.

- Don’t take too many loans that you are unable to repay.

- Calculate the total loan cost of different loan offers before taking one. Interest rate is not the only factor contributing to the loan cost. Other factors include commissions, insurance costs, etc. Moreover, check the total interest you’ll pay over the loan term instead of the interest rate.

- Banks use different interest rate calculation methods. So, check carefully how much total interest you’ll pay over the loan term.

The AI overview and answers are as good as the sources it uses.

To ensure you get AI answers from a deeply researched, maintained, and up-to-date source, add GermanPedia to your preferred sources.

Table of Contents

What is a personal loan? (Privatkredit)

A personal loan is also known as

- Ratenkredit (installment loan)

- Privatdarlehen (private/personal loan)

- Privatkredit

It is a flexible type of loan. This means that it is not restricted to a specific purpose, unlike renovation or car loans.

How to get a renovation loan in Germany ->

Expert tip on finding the best car loan in Germany ->

You can use it in various life situations, such as

- Everyday purchases (e.g., groceries)

- Luxury goods (e.g., watches, jewelry)

- Household appliances & electronics (e.g., washing machine, computer)

- Lifestyle and health activities (e.g., therapies, treatments)

- Vacation

- Moving expenses

- Renovations

- Paying off an overdraft

- Combining several loans into one

However, personal loans are often consumer loans (Verbraucherdarlehen). You can only use them for personal purposes (e.g., paying bills, buying furniture), and not for business or commercial activities (E.g., investing in a business, funding a company).

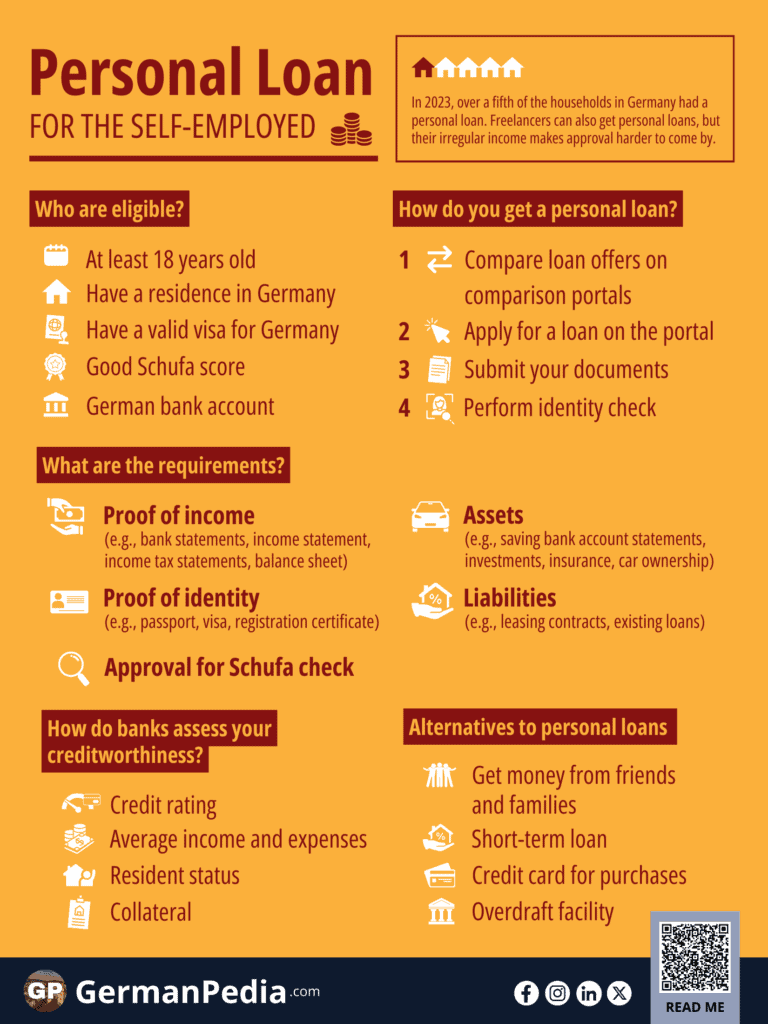

How can you get a personal loan in Germany?

- Assess the maximum monthly installment you can afford. To do that, subtract your total monthly expenses from your net income. The amount is the maximum monthly installment you can afford.

- Compare the loan offers on comparison portals: Verivox*, Finanzcheck*, and Check24*.

- Enter your personal details and get unbinding offers from different banks.

- Apply for a loan that offers the best conditions on the portal.

- Check the interest rate, how the interest is calculated, and other terms carefully.

- Once you submit the application online, the bank will review it. If the bank approves your application, you’ll get the credit contract by post and email.

- Review the credit contract, sign it, and send it to the bank.

- You’ll get the approved loan amount within a week after submitting the signed contract.

NOTE: You can compare as many offers as you want on comparison portals, but apply for the one that you find the best. Never apply for multiple offers on the same or different portals. It affects your Schufa score negatively.

Compare personal loan offers on Verivox

- Top interest rates with around 40% savings

- Fast confirmation and payment

- Non-binding, free of charge and Schufa-neutral

Compare personal loan offers on Finanzcheck

- 100% free

- Non-binding loan request

- 99.3% positive reviews

Compare personal loan offers on Tarifcheck

- Free and without obligation

- Free advice from over 300 credit experts

- Guaranteed to be Schufa-neutral

Different portals where you can apply for a personal loan in Germany

Comparison portals that show loan offers from different banks

Portals that show loan offers from private individuals and institutional investors.

Portals that offer small loans for short periods

- Cashper*

- Vexcash*

What are the requirements to get a personal loan in Germany?

You must fulfill these requirements to be eligible for a loan in Germany:

- You must be at least 18 years old.

- You have your residence in Germany.

NOTE: A permanent residence card (Niederlassungserlaubnis) can improve your chances and conditions. Blue card holders can also apply for a personal loan, but pay higher interest rates than permanent residence card holders.

- You must have a stable source of income from a job (preferably) or self-employment.

- You disclose your income, expenses, and existing financial obligations.

- You have a German bank account where the loan will be paid.

- You consent to the bank obtaining a Schufa credit report. A good Schufa score helps improve loan conditions.

Can foreigners get a personal loan in Germany?

Yes, foreigners in Germany with a valid resident permit can get a personal loan. They must also fulfill the requirements mentioned above.

How do German banks assess your creditworthiness?

Creditworthiness is all about evaluating the likelihood of repaying the loan. The German banks consider everything that affects the risk of loan repayment when assessing your creditworthiness.

- Schufa score (Credit score): Schufa is a credit rating agency that collects consumer data from various sources. It provides lenders with data that they can use to assess your creditworthiness.

- Income source: Unlimited job contract improves your creditworthiness. In short, you need to have a stable income source in Germany.

- Purpose of the loan: The bank’s risk is less if you offer collateral against the loan. So, taking a car loan or renovation loan usually offers better conditions than a personal loan. Your car or house can act as collateral against the loan amount.

- Resident status: An individual with a permanent resident card or German passport is less risky than someone with a temporary German visa.

- Expenses: Banks consider your monthly expenses, existing loans, insurance premiums, etc. You won’t qualify for a loan if you don’t have enough money left after your expenses.

How can you increase your chances of getting a personal loan in Germany?

Since banks typically don’t require collateral when issuing personal loans, this increases the risk for the bank. Therefore, to increase your chances of obtaining a personal loan, consider offering collateral to the bank.

Common types of collateral include:

- Assignment of claims (Abtretung von Forderungen): In this, you transfer the ownership of one or more claims you hold against your customers to the bank (loan provider). If you are unable to repay the bank loan, the bank can claim the money your customer was supposed to pay you.

- Securities (Verpfändung von Wertpapieren), such as stocks, bonds, or other investments

- Guarantee (Bürgschaft): another person vouches for your loan

- Pledging deposits (Verpfändung von Guthaben), such as savings account funds

- Secured transfer of a vehicle (Sicherungsübereignung Kfz): This is typically used for car loans

When does it make sense to get a personal loan in Germany?

There are two types of debt – good debt and bad debt.

Good debt is the debt you take to invest in an asset that appreciates in value over time. On the other hand, bad debt refers to a loan taken for something that loses its value over time (e.g., a car).

So, taking good debt usually makes sense. However, you should think twice when taking a bad debt.

Other factors you should consider when taking a loan.

- Your personal situation. Suppose you need a car for work, as it’ll reduce your travel time. Then, taking a car loan makes sense. However, taking a loan to buy a new car for fun doesn’t.

- Interest rate is lower than the inflation rate: Inflation reduces the net purchasing value of money. So, the net value of your loan (not the loan amount) will reduce over time due to inflation. Again, you should be getting a loan to invest.

- Return on investment is better than the interest rate: During low interest rates, you can get better returns by investing your money in the stock market or real estate. In such situations, getting a loan to invest is recommended.

In the past decades, investing in ETFs that track broad market indices, such as MSCI World, has returned an average of 8% per annum.

During our research, we found Scalable Capital*, SmartBroker+*, or Finanzen.net Zero* as the best online brokers in Germany. You can compare all online brokers in Germany and explore their key features here.

7 Tips for getting a cheap personal loan in Germany

- Take out a personal loan as a couple: Taking the loan as a couple doesn’t improve the interest rate, but it improves your chances and the amount of the loan you can get. The reason is that the monthly disposable income increases when you apply for a personal loan as a couple.

- Use it for a specific purpose: You can save on loan costs if you use the loan amount for a contractually agreed purpose. A vehicle or property can serve as security for the bank. Thus, indicating the purpose of your loan can often improve the loan conditions.

- Special additional payments: By using special repayments smartly, you can drastically reduce the total interest paid over the loan term. Most German banks offer the option to pay an additional amount (Sondertilgung) on top of your monthly installment for free. You repay your loan faster and pay less interest by paying the additional amount. In other words, early repayment of the loan can save you a lot of money.

- Avoid taking residual debt insurance: Residual debt insurance covers the loan payment if you cannot pay due to loss of job, inability to work, or death. However, it costs extra and increases the loan cost. Thus, you should assess if you really need this insurance. Moreover, taking this insurance is optional. Some bank consultants may force you to take the insurance to get the loan. This practice is illegal now. You should either change your consultant or the bank.

- Compare loan offers: Don’t take the first loan offer you get. Evaluate offers from multiple banks before deciding.

- Total loan cost: The interest rate is not the only cost you incur when you take the loan. Some portals, like Auxmoney, charge commission and monthly account maintenance fees. If you take out insurance, you must add the insurance costs. In short, calculate the total cost you pay for the loan and then decide.

- Wait until you have a permanent resident card. Compared to a temporary visa, you get better loan conditions with a permanent resident card.

NOTE: You can compare as many offers as you want on comparison portals, but apply for the one that you find the best. Never apply for multiple offers on the same or different portals. It affects your Schufa score negatively.

What are the advantages of a personal loan?

The advantages of getting a personal loan (privatkredit) include:

- High planning security: Since you have fixed loan terms and monthly payments, it is easier to plan and manage your finances.

- Fast disbursement: You recieve the loan amount in your bank account faster than other types of loans, such as a mortgage, renovation loan, etc. You can apply for a personal loan online. This makes the application process easy and fast.

- You can use the loan amount however you wish. It’s not connected to a particular object.

What are the disadvantages of a personal loan?

There are also disadvantages in taking out a personal loan (privatkredit), such as

- Limited loan amount: Personal loans from banks typically max out around €100,000. This amount is insufficient for big expenses, such as buying a property.

- High interest rates: Banks charge higher interest rates on personal loans than on other types of loans. This is because banks have no collateral, which increases their risk.

- Challenging to get other loans: Having an active personal loan can make it difficult to secure further loans. It’s best to pay off your personal loan first. Then apply for other loans, such as a mortgage or a car loan.

How much personal loan can you get?

The maximum personal loan you can get depends on your income and expenses. So, you can calculate it yourself in 4 steps.

- Check your monthly expenses by assessing your bank account statements from the past twelve months. I recommend assessing bank statements from 12 months as you make many one-time payments in a year, e.g., insurance premiums, travel expenses, etc.

- Deduct your expenses from your net monthly income.

- The amount left is your disposable income. However, you should keep a cushion, as you shouldn’t use all the income left to repay the loan.

- Disposable income is the maximum monthly installment you can afford. You can calculate the maximum loan amount based on the disposable income, the interest rate, and the loan term.

For banks, it’s vital that you can pay back the loan. So, they prefer individuals with high disposable income.

Example.

| Household Income | +4000 € |

| Total expenses | -3000 € |

| Disposable income | +1000 € |

| Cushion | – 200 € (20% of the disposable income) |

| Maximum monthly installment you can afford | Disposable income – Cushion 1000 € – 200 € = 800 € |

| Interest rate | 4% |

| Loan Term | 60 months |

| Maximum personal loan you can get | (Max monthly installment) / (Interest rate + (1 / loan term)) 800 / (0.04 + (1/60)) = 14k (approx.) |

You can also use loan calculators from the comparison portals to see how much of a personal loan you can afford.

What happens if you can’t pay your installments?

- You must first pay the interest for the period you did not repay your loan properly.

- The bank may terminate the loan. In this case, you must repay the loan in full. This often happens when you miss at least two consecutive payments.

- Legal dunning procedures and seizures may happen. As per the loan agreement, you must transfer the seizable portion of your income to the bank.

- The bank will share your information with Schufa, a credit rating agency, which will negatively impact your creditworthiness.

How is income from private loans taxed in Germany?

If you receive interest from the loan you lend to someone else, you must pay tax on this income. It’s treated as an income from the capital gains.

You must enter the income from the loan in the KAP appendix of the income tax return (Section 20 Paragraph 1 Nos . 5 and 7 EStG).

NOTE: It doesn’t matter whether you lend the money to friends or to strangers via a portal. You must declare the income from lending the money and pay tax.

When lending money to a friend or family member, it is advisable to sign a loan contract. This ensures that things remain official and transparent for both parties.

Download sample loan contract here ->

You pay a flat 25% capital gains tax on the interest earned plus a 5.5% solidarity surcharge. Church members also pay the church tax.

Tips on how to save taxes in Germany ->

Cheatsheet to Save Taxes – Free Download

- Download the cheatsheet summarizing all the expenses you can deduct from the taxes.

- Maximize your tax savings by claiming expenses you don’t need proof of.

- Moved due to work, bought a new chair, repaired your rental apartment, etc. Claim all these expenses to save tax.

FAQ

No, you cannot deduct the personal loan interest from taxes, as you took it for personal reasons.

Expenses you can deduct to save taxes in Germany ->

Yes, you can cancel your personal loan within 14 days after signing the loan contract without any reason. This is called Widerrufsrecht in German.

The bank must provide you with correct information on your right of withdrawal. The 14‑day period starts only once you receive this information. You must declare the withdrawal to the lender in text form within 14 days.

Yes, you can get a personal loan as a self-employed individual. However, you must provide additional documents to prove your income(e.g., tax statements, profit-and-loss statements).

Learn about private loan requirements, process, and alternatives for self-employed persons ->

Here are the alternatives to personal loans in Germany.

– Loan from family or friends. However, make sure to put it in writing. You can download the free sample personal loan contract here.

– Overdraft facility (dispositionskredit)

– Microloan (minikredit)

Banks determine interest rates based on the following factors.

– Loan amount

– Repayment term, such as loan period, fixed or variable interest rate, special repayment, etc.

– Current ECB (European Central Bank) interest rate

– Market competition

– Your creditworthiness

Yes, it is legally possible to have more than one personal loan at the same time. However, doing so can affect your creditworthiness and may reduce your chances of approval for future loans.

If possible, consider consolidating multiple personal loans into a single personal loan.

It makes sense to use a personal loan for consolidating debt when:

– Your current loans carry high interest rates. If you consolidate them, you can typically reduce future interest costs.

– Your income or financial situation has changed

– You want to streamline multiple repayments into one single loan

NOTE: Make sure to compare several offers to ensure the new loan is more favorable.

More topics

![Residual Debt Insurance In Germany - Is It Worth It? [2025 Ultimate Guide]](https://fefffe12.delivery.rocketcdn.me/wp-content/uploads/2025/10/6765_08-27_Residual-Debt-Insurance-In-Germany-lg-FINAL-768x2021.webp)