Key takeaways

- Self-employed individuals can get personal loans, but it’s harder due to irregular income.

- Self-employed people can expect higher interest rates than employed individuals with regular income.

- To get a loan in Germany, you must be at least 18, reside in Germany, and have a German bank account.

- Banks require several documents, such as income tax statements, income statements, balance sheets, business evaluations, and bank statements, to assess your creditworthiness.

This is how you do it

- Compare the loan offers on comparison portals: Verivox*, Finanzcheck*, and Check24*.

- Check alternatives for personal loans like credit cards, short-term loans, or asking for money from friends and family.

- Providing collateral against the loan can improve your chances of getting a loan in Germany.

The AI overview and answers are as good as the sources it uses.

To ensure you get AI answers from a deeply researched, maintained, and up-to-date source, add GermanPedia to your preferred sources.

Table of Contents

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

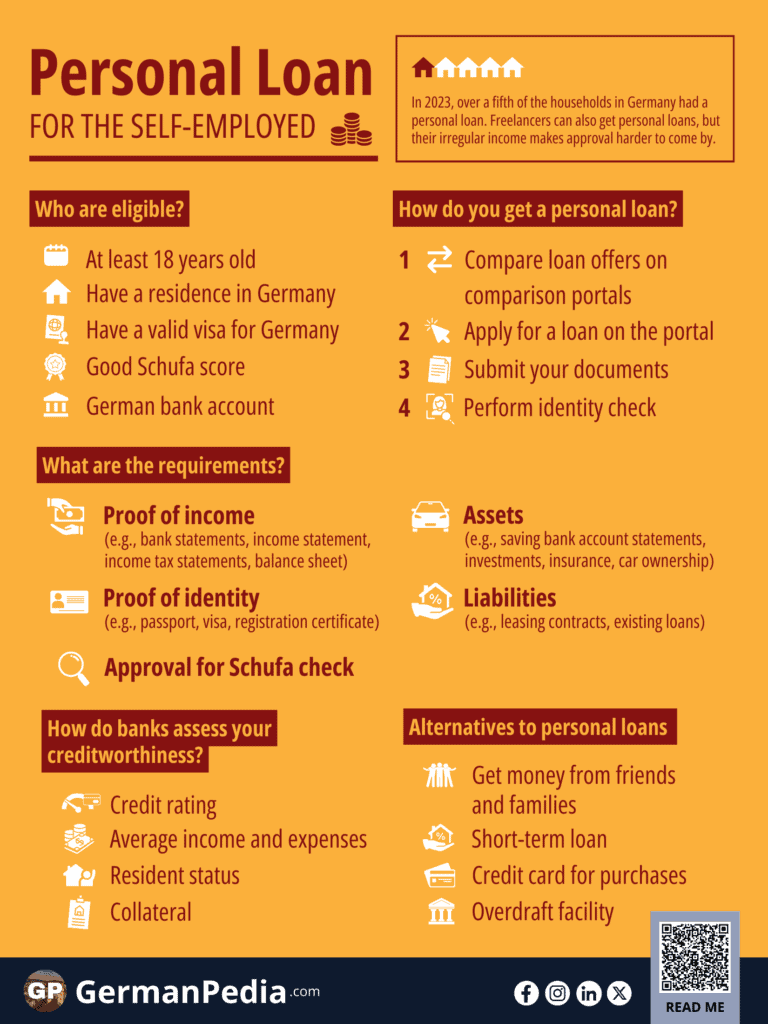

Can you get a personal loan if you are self-employed in Germany?

Yes, you can get a personal loan as a self-employed person in Germany. However, as a freelancer and self-employed person, you have irregular income, which makes it tough to get good loan offers.

The requirements for getting a personal loan for the self-employed are the same as those for an employed individual.

- You are at least 18 years old

- You have a residence in Germany

- You have a valid visa for Germany (Banks prefer permanent residence)

- Good Schufa score

- German bank account where the loan should be paid.

Best free checking bank accounts in Germany ->

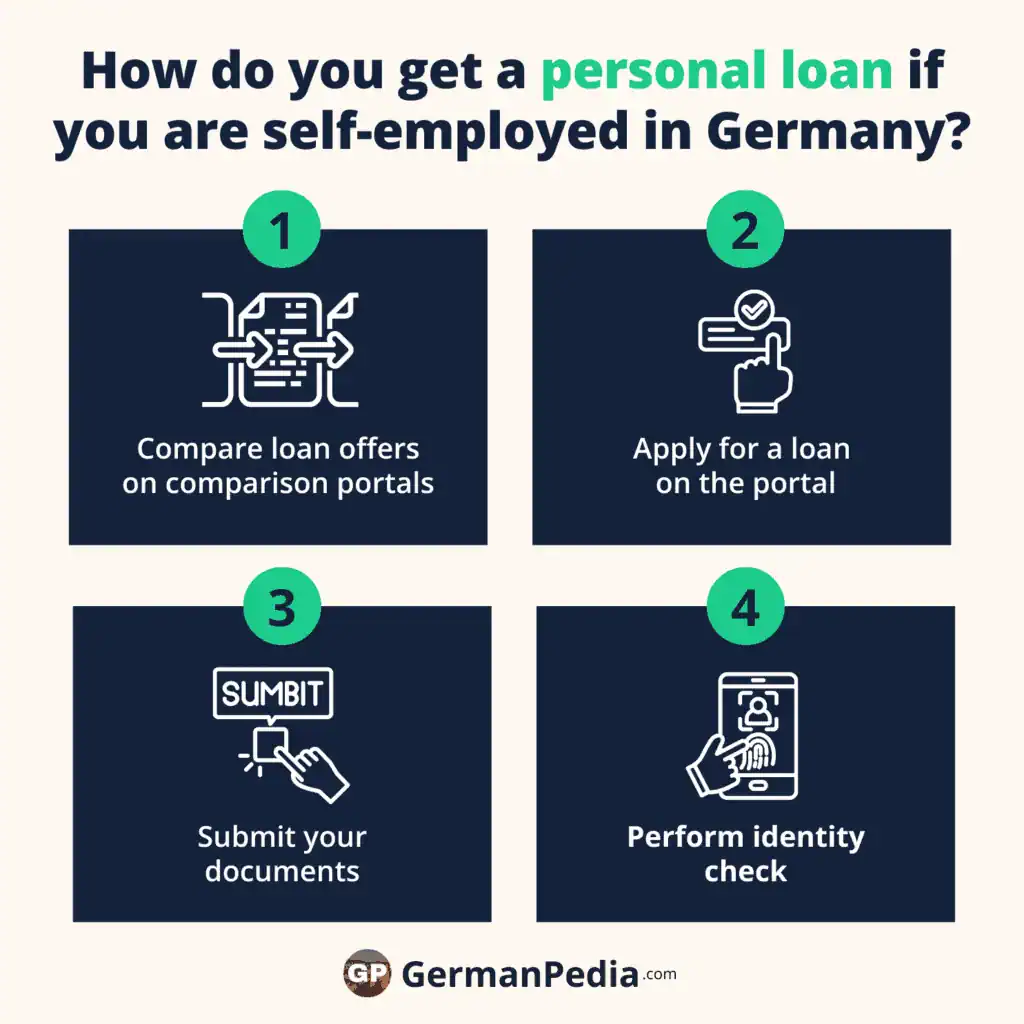

How do you get a personal loan if you are self-employed in Germany?

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

- Compare the loan offers on comparison portals: Verivox*, Finanzcheck*, and Check24*.

- Apply for a loan directly at the portal

- Submit the required documents

- Perform the identity check using video ident or going to the post office to verify your identity.

Usually, self-employed individuals get loans at a higher interest rate than employed individuals with stable incomes.

NOTE: You can compare as many offers as you want on comparison portals, but apply for the one that you find the best. Never apply for multiple offers on the same or different portals. It affects your Schufa score negatively.

Compare personal loan offers on Verivox

- Top interest rates with around 40% savings

- Fast confirmation and payment

- Non-binding, free of charge and Schufa-neutral

Compare personal loan offers on Finanzcheck

- 100% free

- Non-binding loan request

- 99.3% positive reviews

Compare personal loan offers on Tarifcheck

- Free and without obligation

- Free advice from over 300 credit experts

- Guaranteed to be Schufa-neutral

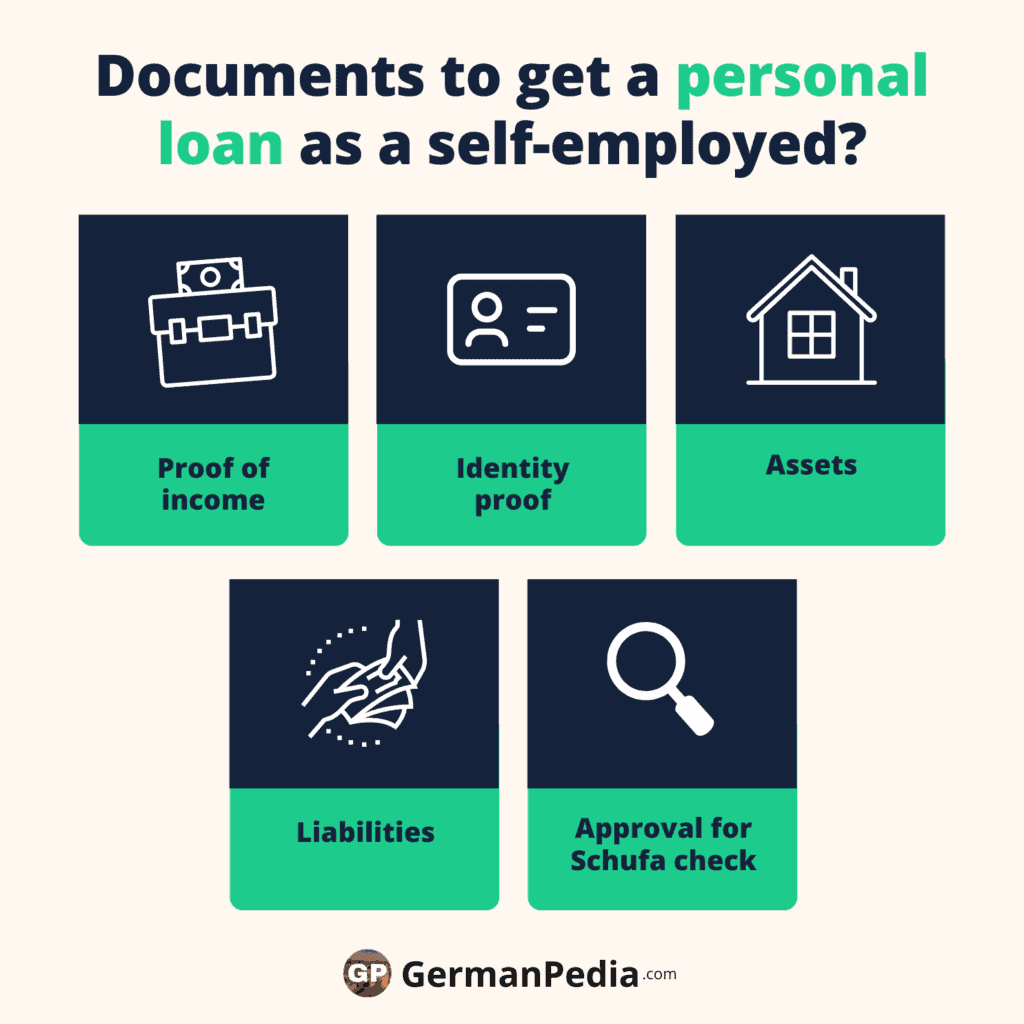

What documents do you need to get a personal loan as a self-employed?

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

Banks require these documents to process the loan application.

- Proof of income

- Profit & Loss Statement

- Bank statements from the past 3 months

- Current business evaluation (e.g., BWA)

- Asset and debt status

- Income statement

- Income tax statements or balance sheets from the last two years

- Health insurance contribution statement (Buchungsanzeige der Krankenkasse)

- Tax prepayment notice

- Proof of payment of income tax prepayment (e.g., bank statement, direct debit notifications from the tax office (Lastschriftanzeige des Finanzamtes))

- Balance sheet for the current financial year

- Depending on your business’s legal form, some banks may require

- Business registration

- Trade license

- Chronological commercial register extract

- Partnership agreement

- Certificate of registration in the Chamber of Commerce

- Profit & loss statement

- Business plan

- Identity

- Passport

- Visa

- Registration certificate (Meldebescheinigung)

- Assets/Collateral

- Saving bank account statements and other savings plans

- Investments like stocks, real estate, etc.

- Insurance, such as term life insurance or homeowners’ insurance

- Car ownership

- Liabilities

- Leasing contracts

- Existing loans

- Spousal or children’s support, if applicable

- Your approval is required so that the bank can request your Schufa score.

The banks may ask for further documents based on your personal situation.

The banks don’t want to give loans to high-risk individuals. They add you to the high-risk individuals category based on the following criteria

- you don’t have a stable income,

- you are a low earner,

- you have existing loans and obligations,

- you don’t have a permanent German resident card,

- you don’t have enough savings or investments,

- you have no or low Schufa score, etc.

How can you improve your Schufa Score? ->

How do banks assess your creditworthiness?

It’s tougher for self-employed individuals to get a loan in Germany than for employed individuals. The main reason is the irregular income.

However, banks consider the following when assessing your creditworthiness:

- Credit rating: Banks refer to your Schufa score (Credit score) to assess your credit rating. The higher the score, the better it is.

- Your average income and expenses

- Resident status: Banks prefer individuals with a permanent residence card over a blue card or a temporary visa.

- Collateral: Banks want to reduce their risk as much as possible. Collateral can reduce the bank’s risk, thus improving your chances of getting a loan.

- Stable track record: Banks prefer self-employed applicants who have been operating successfully for at least a year. This allows them to assess the business’s stability or profitability. New entrepreneurs or start-ups, on the other hand, are perceived as higher risk.

How can you improve your chances of getting a personal loan?

- Offer collateral for your loan application. This will reduce the bank’s risk. Hence, improving your chances of loan approval or a favorable interest rate.

- Add a co-borrower to your loan. This will increase overall income and reduce the risk of payment defaults.

Alternatives to personal loans for a self-employed person

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

- Get money from friends and families

- Private lenders and investors

- Apply for a short-term loan

- KfW loans (German Development Bank)

- You can make the purchase using a credit card. You can either repay the amount in 30 days or utilize the installment payments option.

- Use the overdraft facility of your checking account.

- Take out a purpose-bound loan (e.g., car loan, mortgage, etc.). The financed item (e.g., a car) can serve as collateral, reducing the bank’s risk.

How can self-employed individuals get a loan for their business?

Business loans are completely different from personal loans in Germany. You have the following options to get a loan for your startup or business.

- Low-interest loans for startups from EU funding: The EU backs the funding, reducing the risk for the banks and allowing them to offer loans to startups at low interest.

- GRW grants: GRW provides investment grants and subsidies to manufacturing companies in disadvantaged regions.

- Get funding from the investors

- Get a loan from a bank

Learn more about how to raise funds for your startup in Germany here ->

You can use the loan for your business only. Here are some examples.

- buying new equipment

- expanding your business

- improving cash flow

FAQ

Yes, you, as a self-employed individual, can get a personal loan without collateral. Still, offering collateral, a guarantor, or a co-borrower can improve your approval chances or loan conditions.

Yes, your company’s legal form affects which documents you must submit as part of your personal loan application. However, the legal form itself doesn’t influence the loan approval or rejection.

Banks focus on your income stability and business track record to assess risk.

More topics

References

- https://gruenderplattform.de/finanzierung-und-foerderung/kredit-fuer-selbststaendige#vor-und-nachteile

- https://www.check24.de/kredit/kredit-fuer-selbststaendige/

- https://www.smava.de/kredit/selbststaendige-kredit/

- https://www.vr.de/firmenkunden/produkte/finanzierung/betriebsmittelkredit/kredit-fuer-selbststaendige.html#faq-26758e7ea1-item-edc5bc5e0b

- https://www.sparkasse.de/pk/produkte/kredit.html

- https://www.targobank.de/de/kredit/selbststaendigenkredit.html#TB1-E-ACCO-01-10-A

- https://selbststaendigkeit.de/news-forderung-und-finanzierung/besonderheiten-bei-einem-kredit-fuer-selbststaendige/?utm_source=chatgpt.com

![Residual Debt Insurance In Germany - Is It Worth It? [2025 Ultimate Guide]](https://fefffe12.delivery.rocketcdn.me/wp-content/uploads/2025/10/6765_08-27_Residual-Debt-Insurance-In-Germany-lg-FINAL-768x2021.webp)