Key takeaways

- The German tax system offers several ways to save taxes. You must know what they are to maximize your tax refund.

- Tax ID is an 11-digit unique number that remains valid throughout your life.

- The tax office may charge a late fee and penalty if you miss the deadline to file the tax return.

- Your employer deducts income tax, social security contributions, church tax, and solidarity surcharge from your income and transfers the rest to your bank account.

This is how you do it

- Educate yourself about the German tax system and vocabulary.

- Keep a note of the tax filing deadline to avoid fines.

- Many online services help you file simple income tax returns in Germany. We find WISO Steuer* (German), SteuerGo*, Check24 Tax (German), and Wundertax*, among the best tax software out there. Here is the complete comparison of the tax software in Germany.

- We recommend consulting a tax advisor for complex tax returns. You can get a free quote a tax advisor here. The tax consultant offer services in English.

The AI overview and answers are as good as the sources it uses.

To ensure you get AI answers from a deeply researched, maintained, and up-to-date source, add GermanPedia to your preferred sources.

Table of Contents

Tax Id and Tax Number

In Germany, the tax office assigns two numbers to everyone for tax purposes.

- Tax Identification Number (Tax ID) (Steueridentifikationsnummer)

- Tax Number (Steuernummer)

Tax ID

German Tax ID has the following characteristics.

- It’s eleven digits and unique.

- Your tax ID is valid for life and even up to 20 years after death.

- The tax office automatically assigns a tax identification number.

- If you are born in Germany, you the tax ID within three months of your birth.

- If you are an expat, you get the tax ID once you register at the local municipal office in Germany.

- People also refer to Tax ID as

- Persönliche Identifikationsnummer,

- Identifikationsnummer,

- TIN (Tax Identification Number),

- IdNr.

- Steuer-ID

- Tax ID helps tax authorities to uncover tax evasion more easily

Tax number

Your local tax office (Local Finanzamt) issues the tax number (Steuernummer), which differs from your tax identification number (Tax ID).

Tax number is a 10-13 digit number that indicates which tax office is responsible for you. You can break down the German tax number into four parts.

- The first 2/3 digits identify your local tax office (Finanzamt)

- Next 2/3 digits identify your district

- Next 4/3 digits identify you

- The last digit is used as the check digit.

Tax classes in Germany

There are seven different tax classes in Germany. Your payroll tax deduction depends on your tax class.

| Tax Class (Steuerklasse) | Who gets this tax class | Tax allowance you get in this tax class |

|---|---|---|

| Tax class I | – Single – Divorced employees – Widowed employees – but only from the second year after the spouse’s death. – A non-german employee whose spouse lives outside the EU. – An employee is subject to limited income tax liability because they earn income in Germany but live abroad permanently. | Basic tax-free allowance of 12,348€ (in 2026) |

| Tax class II | All individuals listed in tax class 1 can opt for tax class II, provided they are single parents. The prerequisite is that at least one child lives in your household for whom you receive a child allowance (Kinderfreibetrag) or child benefit (Kindergeld). The tax office does not assign you the tax class II automatically. Instead, you must apply for it. | Tax relief amount (Entlastungsbetrag in German) on top of the basic tax free allowance. The tax relief amount (Entlastungsbetrag) is 4,260€ (as of 2026) for the first child and 240€ additionally for each additional child |

| Tax class III & V | Married couples and registered civil partners. You must fulfill the following conditions. – You and your partner both live in Germany. – You don’t live in different households permanently. – Your spouse does not earn, or they are in tax class 5. | In tax class III, your basic tax-free allowance doubles. However, your partner gets no basic tax-free allowance in tax class V. Filing a tax return is mandatory for couples in tax classes 3 and 5. |

| Tax class IV | The tax office automatically assigns the newly married couples tax class IV irrespective of whether they both work or not. To be eligible for tax class IV, – you and your spouse must live in Germany – and not live in different households all the time. | The tax deduction and tax allowance is similar to that in tax class 1. Thus, tax class 4 makes sense if both partners earn almost the same income. |

| Tax class IV with factor | Married couples or registered civil partners | The factoring technique ensures a fair distribution of the salary tax burden. Filing an annual tax declaration is compulsory. Moreover, you must apply to stay in this tax class combination every two years. |

| Tax class VI | Employees who start a second or third job automatically end up in tax class VI. You can decide to which of your jobs the tax class 6 should be applied. Example: Suppose you were in tax class I before you got a second job. You earn more from Job A. In this case, you can tax it per tax class 1 and tax the Job-B under tax class 6. | No tax-free allowance |

Who is obligated to file a tax return in Germany?

Self-employed and farmers must always file a tax return.

Employees and civil servants must file an income tax return in the following situations (According to Section 46 of the Income Tax Act (EStG)).

- You have income on which you didn’t pay income tax, such as rental income.

- You received wage replacement benefits, such as unemployment, short-time work, sickness benefits, maternity, insolvency, or parental allowance of more than 410€. This also applies to top-up contributions for partial retirement.

- You work multiple jobs or receive multiple wages at the same time.

- You have the tax class combination 3/5 or 4/4 with a factor.

- You have claimed allowances for income tax deductions from the tax office, and you received more than 12,096€ (in 2025) as a single person and 24,192€ (in 2025) as a married couple filing jointly. This is increased to 12,348€ (in 2026) for single person and 24,696€ (in 2026)

- Your income tax certificate (Lohnsteuerbescheinigung) is marked with the letter “S.” This may happen in the following situation: You changed jobs within a year and received special payments such as a Christmas bonus. In this case, it’s possible that your new employer didn’t consider your previous employer’s contributions when calculating your income tax. This is rare, but you should check your Lohnsteuerbescheinigung to confirm.

- You have received a severance payment, and the favorable fifths rule (Fünftelregelung) was applied when calculating the income tax.

- Your partner died or you got a divorce, and you or your ex remarried in the same year.

- Your spouse is on the tax card and lives in another EU country.

- Your current residence is outside Germany, and you have applied for unlimited tax liability in Germany.

- You have claimed a loss carryforward.

Note: You must file an income tax return if the tax office requests it even if none of the above-mentioned requirements apply to you.

What are the deadlines for filing taxes in Germany?

The deadline to file an income tax return in Germany depends on whether filing the tax return is mandatory.

Deadline for people required to file a tax return

| Tax year | Deadline (You don’t hire a tax advisor) | Deadline (You hire a tax advisor) |

| 2024 | 31.07.2025 | 30.04.2026 |

| 2025 | 31.07.2026 | 01.03.2027 |

Deadline for people filing a tax return voluntarily

If you are not required to file a tax return, you can still file one voluntarily. In this case, you have four calendar years to file the tax return.

| Tax year | Deadline (Doesn’t matter if you hire a tax advisor or not) |

| 2022 | 31.12.2026 |

| 2023 | 31.12.2027 |

| 2024 | 31.12.2028 |

| 2025 | 31.12.2029 |

So, as of 2026, you can still file a tax return for 2022 and onward.

You can learn all the tax-deductible expenses here.

Cheatsheet to Save Taxes – Free Download

- Download the cheatsheet summarizing all the expenses you can deduct from the taxes.

- Maximize your tax savings by claiming expenses you don’t need proof of.

- Moved due to work, bought a new chair, repaired your rental apartment, etc. Claim all these expenses to save tax.

What happens if you miss the deadline to file the tax return?

The tax office levies a fine if you miss the deadline to file the tax return. However, the penalty only applies to you if you are required to file the tax return.

If you don’t file the voluntary tax return on time (i.e., within four years), you don’t pay any fine. However, you lose your chance of filing the tax return for that tax year.

Here are the different penalties the tax office may impose based on the level of escalation and delay.

- Late fee (if you miss the regular deadline)

- Penalty in addition to the late fee (if you miss the new deadline set by the tax office)

- The tax office estimates your taxable income (last step)

Late fee (Verspätungszuschlag)

Firstly, the tax office sends a letter warning you to file the tax return and the new deadline.

In this first step, the tax office MAY levy a penalty if you submit your tax return after the regular deadline but within 14 months of the tax year. However, the tax office MUST levy a penalty if you file the tax return 14 months after the tax year.

For the tax year 2025, the tax office MAY charge a late fee if you miss the regular deadline of 31 July 2026. However, the tax office MUST charge the late fee if you file after 28 February 2027 (14 months after tax year 2025).

The late fee is 0.25% of your tax debt, but at least 25€. You must pay this fee for each month of delay in tax filing.

Example: Suppose you delayed filing the tax return by 4 months. In this case, you pay at least 100€ (25€ * 4 months) in late fees on top of any tax payments.

NOTE: The late fee applies regardless of if you have to make a tax payment or you’ll receive a tax refund. So, always file the tax return within the deadline.

Penalty (Zwangsgeld)

If you miss the new deadline set by the tax office in their first letter, you may have to pay a penalty (Zwangsgeld) and the late fee (Verspätungszuschlag).

The penalty amount depends on the following factors:

- Your financial situation

- How cooperative you have been with the tax authorities so far

- Whether you’ve submitted your tax return late on several occasions.

If you’ve failed to file a tax return for the first time, the penalty is usually between 100€ and 500€. However, the tax office may charge you up to 25,000€.

The tax office estimates your taxable income

You still haven’t filed the tax return after receiving a penalty notification from the tax office. In this case, the tax office estimates your taxable income.

You have one month after receiving the estimate to file an objection. After that, it becomes final.

Furthermore, the tax office charges interest of 1.8% on the tax due. The interest period begins 15 months after the end of the calendar year in which the tax was incurred.

Example: For tax year 2025, the interest period begins on 1 April 2027, 15 months after the end of 2025.

Due to the coronavirus pandemic, the tax office adjusted the interest period to the tax return deadlines. For example, for the 2023 tax year, the interest period starts on 1 July 2025.

Fun fact: Suppose filing a tax return is not mandatory for you. So, you decided to file the tax return voluntarily and expect a tax refund. In this case, you can file the tax return late to have the tax office pay interest on your refund. However, this used to be more worthwhile when the interest rate on taxes was still 6 percent.

You can use online services to help you file and save income tax in Germany. We find Wundertax*, SteuerGo*, and WISO Steuer* (German) among the best tax software out there.

If you have a complex tax return or filing it yourself makes you nervous, you should get advice from a tax consultant. Tax consultants are not cheap in Germany. Depending on your situation, they may cost between 600€ and 2000€.

However, a good tax consultant can save you a lot of money.

You can get a free quote from a tax consultant here. The tax advisor offer services in English.

Get a Free Quote From a Tax Advisor

- A tax advisor can help you file an income tax return,

- Change tax class,

- Get a tax residency certificate,

- Support in starting a business,

- Offer services in English

File Income Tax with WISO Steuer (German)

- 35.99 € for filing a single income tax return

- Easy to file and save tax.

- The tool is only available in German.

- It can even handle complex tax situations.

File Income Tax with Wundertax

- 34.99 € for filing a single income tax return

- Tips on deductible costs & plausibility check

- Try it out for free & only submit if you’re fully satisfied

- Also available in English

File Income Tax with SteuerGo

- 34.95 € for filing a single income tax return

- Easy to file and save tax.

- The tool is also available in English.

- Get tax-saving tips to maximize your tax return in the current and the following years.

You can read the detailed comparison of best tax software in Germany here.

How is your income taxed in Germany?

Here are the steps the tax office takes to calculate the tax.

- Calculate your total gross income from all sources.

- Deduct tax allowances from your gross income. Germany offers a lot of tax allowances (Freibetrag) and Relief amounts (Entlassungsbetrag) to reduce your taxable income. The tax office automatically deducts most of these allowances before calculating the income tax.

- Deduct all income-related expenses and other expenses to reduce your taxable income further.

- Deduct child allowance and hardship allowance if applicable. The tax office deducts them automatically.

- Your taxable income is the income left after deducting all the expenses and allowances. The tax office uses this taxable income to calculate your income tax.

The table below shows various types of income sources, allowances, and expenses. Read our guide to learn more about tax allowances and tax-deductible expenses in Germany.

| Income (+) Expense (-) | Income / Expense Type (English) | Income / Expense Type (German) |

|---|---|---|

| + | Income from Agriculture and Forestry | Einkünfte aus Land- und Forstwirtschaft |

| + | Income from Business Operations | Einkünfte aus Gewerbebetrieb |

| + | Income from Self-Employment | Einkünfte aus selbständiger Arbeit |

| + | Income from Employment | Einkünfte aus nichtselbständiger Arbeit |

| + | Income from Capital Assets | Einkünfte aus Kapitalvermögen |

| + | Income from Renting and Leasing | Einkünfte aus Vermietung und Verpachtung |

| + | Other Income as per § 22 EStG | Sonstige Einkünfte i.S.d. §22 EStG |

| = | Total Income | Summe der Einküfte |

| – | Age Relief Amount (Tax-free allowance that is taken into account if you have reached the age of 64 before the tax assessment period) | Alterentlasungsbetrag |

| – | Relief Amount for Single Parents | Entlasungsbetrag für Alleinerziehende |

| – | Allowance for Farmers and Foresters | Freibetrag für Land und Forstwirte |

| + | Additional Amount | Hinzurechnungsbetrag |

| = | Total Amount of Income | Gesamtbetrag der Einkünfte |

| – | Deduct Losses | Verlustabzug |

| – | Special Expenses | Sonderausgaben |

| – | Extraordinary Burdens | Außergewöhnliche Belastungen |

| – | Tax Benefits for Residential Properties, Buildings, Monuments, and Protected Cultural Assets | Steuerbegünstigungen durch zu Wohnzwecken genutzte Wohnungen, Gebäude und Baudenkmale sowie schutzwürdige Kulturgüter |

| + | Refund Surpluses | Erstattungsüberhänge |

| = | Income | Einkommen |

| – | Child allowances (Automatically considered by the tax office if it’s more beneficial than the Kindergeld) | Kinderfreibeträge |

| – | Hardship compensation (according to §46 Abs. 3 EStG, §7 EStDV) | Härteausgleich nach §46 Abs. 3 EStG, §7 EStDV |

| = | Taxable income | zu versteuerndes Einkommen |

What is the difference between tax “absetzen” and “abziehen”?

Understanding the difference between “tax deduction (Steuerabsetzen)“ and “tax reduction (Steuerabziehen)” is vital. In tax deduction, you reduce your taxable income and hence your taxes. In tax reduction, you directly reduce your taxes.

Let’s understand them in detail.

Tax deduction (Steuerabsetzen)

In Germany, you can subtract or deduct the expenses incurred to earn an income. The income left after subtracting/deducting the expenses is the income on which you pay taxes. This income is called taxable income.

So, the less your taxable income, the less taxes you pay.

However, you can’t deduct all your expenses. Only expenses related to earning an income are tax-deductible.

Example: You have a gross income of 80,000€. You bought a laptop for 2000€ and use it 60% of the time for work and 40% for private purposes.

In this case, you can deduct (absetzen) 60% of 2000€ (i.e., 1200€) from your income. This reduces your taxable income by 1200€.

However, you won’t receive a refund of 1200€ from the tax office. Instead, a refund of 439€ only.

Here is how.

- The expense will reduce your total income by 1200€, to 78,800€.

- You pay 15,665€ in income tax on these 78,800€.

- If you didn’t deduct the expense, the tax burden would be 16,104€ (80,000€ income).

- Thus, the tax benefit from deducting the expense is 439€ (16,104€ – 15,665€)

So, the more you earn or the higher your tax bracket, the more you can save in taxes.

Tax Reduction (Steuerabziehen)

As you saw, you don’t get 100% of the expense back in tax deduction (Steuerabsetzen). You only get part of the expense back. However, in tax reduction (Steuerabziehen), you subtract the costs directly from the tax payable.

Only certain expenses qualify for tax reduction (Steuerabziehen). One of them is household expenses. You can subtract 20% of the labor costs for household help from your taxes.

However, the tax office has set a limit on the maximum labor cost for household help you can subtract, which is

- Up to 2,550€ per year for an employee on a mini-job.

- Up to 20,000€ for a self-employed cleaner.

- Up to 6,000€ for a tradesperson.

Example: Suppose you hire a self-employed household helper to clean your apartment and pay them 3,000€ per annum. In this case, you can receive a tax reduction of 600€ (20% of 3,000€). It doesn’t matter how much you earn or in which tax bracket you fall.

Tax allowance vs Flat rate vs Exemption limit

You must have heard several technical terms when understanding ways to save taxes in Germany. They all seem similar, but are different.

If you know what these terms mean exactly, you can use them to your advantage and save taxes. The three terms that confuse people a lot are

- Tax allowance (Freibtrag)

- Flat rate (Pauschbetrag)

- Exemption limit (Freigrenze)

Let’s understand each in detail.

Tax Allowance (Freibetrag)

A tax allowance is a fixed amount that the tax office automatically deducts from your income before calculating taxes. Tax allowance doesn’t directly reduce the tax you must pay by the corresponding amount. Instead, it lowers your taxable income and hence the tax you must pay.

Common tax allowances are

- Basic allowance(Grundfreibetrag): 12,348€ (in 2026)

- Child allowance (Kinderfreibetrag): 3,414€ per child per parent (as of 2026)

Flat-rate (Pauschbetrag / Pauschalen)

Flat rates are the expenses you can claim without proof. Flat rates are beneficial for both the taxpayers and the tax office.

- Taxpayers don’t have to save invoices or proofs for small expenses, as they can claim the flat rates without proof.

- Even if you don’t have any expenses, you can still claim the flat rates to save taxes in Germany.

- Flat rates help the tax office reduce its administrative work.

You can also claim expenses exceeding the flat rate on your tax return. However, you must provide proof to the tax office.

Common flat rates available in Germany are

- Income-related expenses flat rate (Arbeitnehmerpauschbetrag / Werbungskostenpauschale): 1230€ (as of 2026)

- Capital gains flat rate or saver’s flat rate (Sparerpauschbetrag): 1000€ (from 2024)

Tax exemption limit (Freigrenze)

In the tax exemption limit, you pay no tax if your income is within the threshold. However, the tax office taxes your entire income if it exceeds the tax exemption limit.

The exemption limit, therefore, works according to the “all or nothing” principle.

Example: The tax exemption limit for private sales is 1000 €. You pay no taxes if your income from private sales is under 1000 € in a year. However, the tax office will tax your entire income if you earn a euro more than this limit.

Understanding your salary slip

There is a belief that you pay 40% to 45% of your salary in taxes in Germany. This is incorrect.

Here is why.

The following is automatically deducted from your gross income before it lands in your bank account.

- Income tax (Lohnsteuer)

- Social security contributions (Sozialversicherung)

- Church tax (Kirchensteuer)

- Solidarity surcharge (Solidaritätszuschlag)

Social security contributions (Sozialversicherung)

You have already seen what allowances and expenses are deducted from your gross income to calculate the taxable income. Let’s check what constitutes social security contributions.

Social security contributions are broken down as follows:

- Pension insurance

- Unemployment insurance

- Health insurance

- Long-term care insurance

Here is how much you pay for each type of insurance.

| Social security type | Total Contribution Rate | Employer’s share | Employee’s share |

|---|---|---|---|

| Statutory pension insurance | 18.6% | 9.3% | 9.3% |

| Unemployment insurance | 2.6% | 1.3% | 1.3% |

| Statutory health insurance | 14.6% + additional contribution (2.9% average) | 7.3% + 1.45% | 7.3% + 1.45% |

| Long-term care insurance (no children) | 4.2% | 1.8% | 2.4% |

| Long-term care insurance (with 1 child) | 3.6% | 1.8% | 1.8% |

| Long-term care insurance (with 2 children) | 3.35% | 1.8% | 1.55% |

| Long-term care insurance (with 3 children) | 3.1% | 1.8% | 1.3% |

| Long-term care insurance (with 4 children) | 2.85% | 1.8% | 1.05% |

| Long-term care insurance (with 5 or more children) | 2.6% | 1.8% | 0.8% |

Suppose you are single with no kids and earn 3500 € gross per month. The table below summarizes how much you’ll contribute to Social Security.

| Social Security Type | Monthly Contribution (€) | Employer Contribution (€) | Employee Contribution (€) |

|---|---|---|---|

| Pension | 651.00 (3500 € * 18.6%) | 325.50 | 325.50 |

| Unemployment | 91.00 (3500 € * 2.6%) | 45.50 | 45.50 |

| Health Insurance | 598.50 (3500 € * 14.6% + 3500 € * 2.9%) | 306.25 | 306.25 |

| Long-Term Care Insurance | 147.00 (3500 € * 4.2%) | 63 (3500 € * 1.8%) | 84 (3500 € * 2.4%) |

| Total social security contributions paid | 1487.50 | 740.25 | 761.25 |

As you can see, you pay 710€ in social security contributions and 415€ in taxes. In this case, taxes are lower than social security contributions.

However, there is a big difference between income tax and social security contributions.

You pay social security contributions up to a maximum threshold (also known as the contribution assessment ceiling). Once you reach this ceiling, you only pay social security contributions on this maximum amount.

However, you pay income tax on unlimited income. There is no maximum limit.

The table below shows the contribution assessment limit in 2023, 2024, 2025, and 2026.

| Social security type | 2023 (in €) Month (year) | 2024 (in €) Month (year) | 2025 (in €) Month (year) | 2026 (in €) Month (year) | Percentage Increase (%) |

|---|---|---|---|---|---|

| Reference value (Bezugsgröße in der Sozialversicherung”) | 3395 (40,740) | 3535 (42,420) | 3745 (44,940) | 3955 (47,460) | 5.60 |

| Pension (West) | 7300 (87,600) | 7550 (90,600) | 8050 (96,600) | 8450 (101,400) | 4.96 |

| Pension (East) | 7100 (85,200) | 7450 (89,400) | 8050 (96,600) | 8450 (101,400) | 4.96 |

| Health & Long-Term Care | 4987.5 (59,850) | 5175 (62,100) | 5512.5 (66,150) | 5812.5 (69,750) | 5.40 |

| Unemployment (West) | 7300 (87,600) | 7550 (90,600) | 8050 (96,600) | 8450 (101,400) | 4.96 |

| Unemployment (East) | 7100 (85,200) | 7450 (89,400) | 8050 (96,600) | 8450 (101,400) | 4.96 |

Church tax (Kirchensteuer)

You also pay church tax if you are a member of a Christian church community. Church tax is 8% in Bavaria and Baden-Württemberg, and 9% in all other federal states.

NOTE: You don’t pay 8 or 9 percent church tax on your gross salary. But 8 or 9 percent of the tax is due.

Example: You pay 415€ in income tax if you earn 3500€ monthly gross. The church tax will be 8 or 9 percent of 415€, which is 33.2€ or 37.35€ per month.

Solidarity surcharge (Solidaritätszuschlag)

The solidarity surcharge is 5.5% of the tax due. It was introduced in 1991 to cover the costs of German reunification.

Until the end of 2020, every German resident paid a solidarity surcharge. As of 2021, only high earners pay the solidarity surcharge.

If the annual tax you must pay is less than

20,350€ (as of 2026)

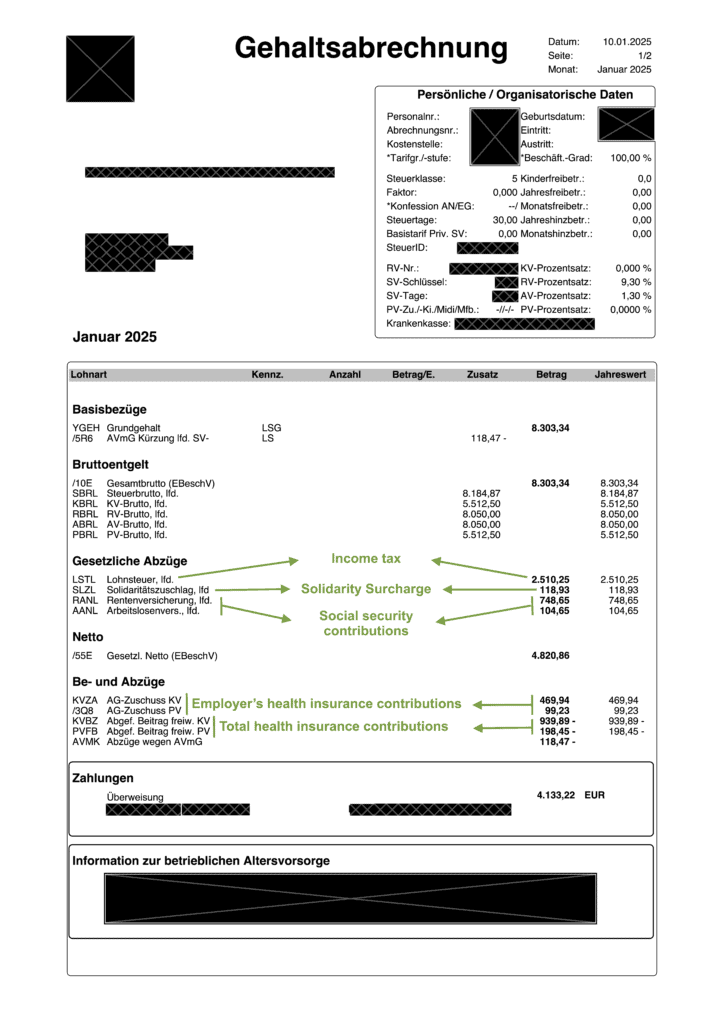

, you don’t pay the solidarity surcharge. However, you pay a solidarity surcharge if you exceed the threshold.Sample salary slip

Here is a salary slip of a high earner. The following is deducted from the gross salary.

- Income tax: 2510.25€

- Social security: 1418.43€ (Your contribution only)

- Health insurance (KV): 939.89€ (Your: 469.95€, Employer: 469.94€)

- Long-term care insurance (PV): 198.45 (Your: 99.23€, Employer: 99.23€)

- Pension insurance (RV): 748.65€

- Unemployment insurance (AV): 104.65€

- Solidarity surcharge: 118.93€

- Church tax: 0€ (not a member of the church)

More topics

- How to save taxes in Germany?

- Tax ID and number

- Change tax class

- Myths about filing a tax return in Germany

- Capital gains tax in Germany

- Deduct relocation costs from taxes

- Types of taxes you pay in Germany

- How much money does the German government collect in the form of taxes?

- Is filing a voluntary tax return worth it?

- What income-related costs can you deduct from taxes in Germany?

- Avoid double taxation in Germany

- Do you pay tax on income from outside Germany?

- Deduct medical expenses from taxes in Germany

References

- https://www.finanztip.de/solidaritaetszuschlag/

- Walter, Fabian. Sei doch nicht besteuert: Mit Steuerfabi die Welt der Steuern verstehen und richtig Geld sparen | Erweiterte und vollständig aktualisierte Ausgabe | Für die Steuererklärung 2024 (German Edition)

- https://www.hanseaticbank.de/hilfe-services/finanzlexikon/solidaritaetszuschlag

- https://www.sage.com/de-de/blog/lexikon/hinzurechnungsbetrag