Key takeaways

- Opening a bank account in Germany is straightforward. You can open an account online or directly at a branch.

- You only need an ID and registration certificate (Meldebescheinigung) to open a bank account in Germany.

- Expats from non-EU countries must also submit a residence permit, and students must have a university enrollment letter on top.

- C24* is the best online bank for expats who know basic German. N26* and Revolut are the other online banking options in Germany for expats. They offer services in English.

- Commerzbank* and Deutsche Bank* are the best brick-and-mortar banks for expats in Germany.

The AI overview and answers are as good as the sources it uses.

To ensure you get AI answers from a deeply researched, maintained, and up-to-date source, add GermanPedia to your preferred sources.

Table of Contents

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

Need help communicating complex ideas visually? We help you turn data into your most persuasive story. Contact us to learn more.

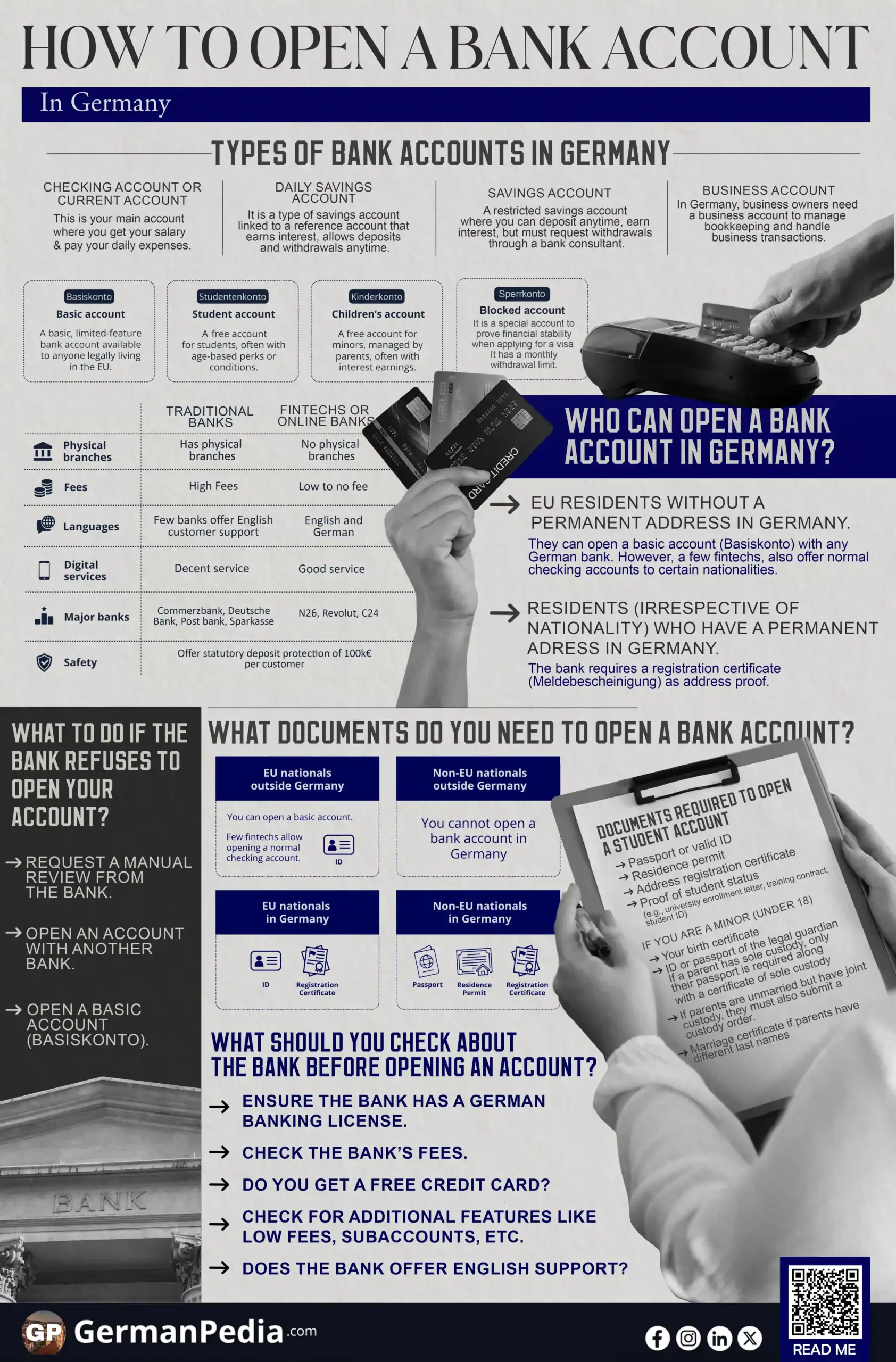

Types of banks in Germany

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

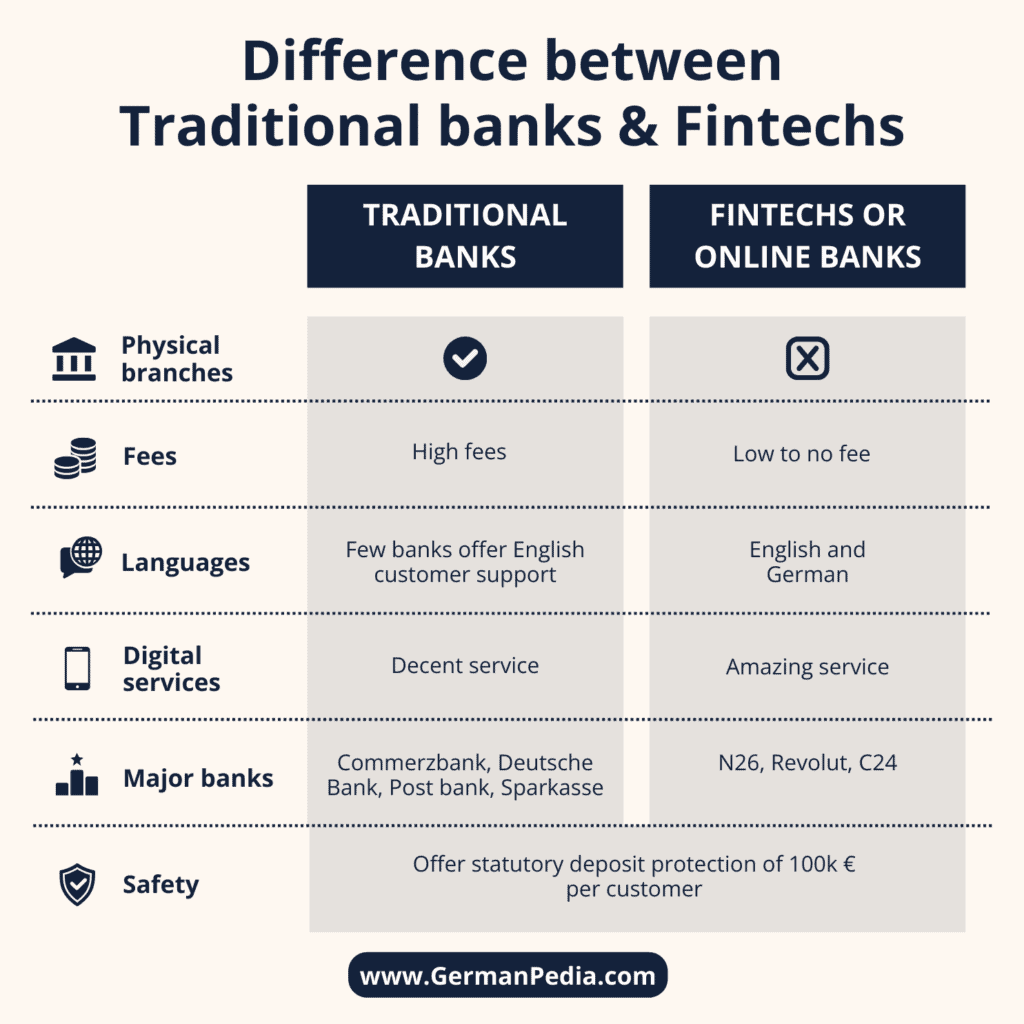

There are two main types of banks in Germany.

- Brick-and-mortar banks: These are traditional banks with physical branches.

- Fintechs or online banks: These are modern banks without physical branches.

Here are some main differences between traditional banks and fintechs.

| Traditional banks | Fintechs | |

| Physical branches | ✅ | No physical branches |

| Fees | High fees | ✅ Low to no fee |

| Language | Only a few banks and certain branches of a bank offer English customer support. | ✅ Many banks offer English and German support |

| Digital services | Offers decent digital services and banking apps | ✅ Offers amazing mobile banking and digital services |

| Major banks | Commerzbank* Deutsche Bank* Post bank (now part of Deutsche Bank) Sparkasse | N26* Revolut C24* |

| Safety | Offer statutory deposit protection of 100k € per customer | Offer statutory deposit protection of 100k € per customer |

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

We recommend having accounts with at least two banks in Germany: one with a traditional bank and one with a fintech. Here are the reasons

- Never keep all your money in one bank (diversify).

- Banks in Germany have the authority to block or close your account without giving any reason. So, if one account is blocked, you can use another to cover your daily expenses. Getting your account blocked is very common and can happen to anyone.

- If you have over 100,000 € in cash, split it among different banks. This is because banks offer statutory deposit protection of 100,000€ per customer. So, if a bank goes bankrupt, you’ll get a maximum of 100k€.

- There might be situations where you’ll need a personal consultation, such as a mortgage. In such situations, it helps to have an account with a traditional bank.

Types of bank accounts in Germany

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

Types of bank accounts in Germany

There are four main types of bank accounts in Germany.

- Checking account or current account (Girokonto): This is your main account where you get your salary and pay your daily expenses.

- Daily savings account (Tagesgeldkonto): It’s a type of savings account connected to a reference account (e.g., your checking account). You get interest on your money in this account and can deposit and withdraw money anytime. You can only withdraw money to your connected reference account. You cannot make payments or purchases directly from your daily savings account. You must first transfer the funds to your connected reference account and make the payment from there.

- Savings account (Sparkonto): A typical savings account with restrictions. You can deposit money anytime. However, you cannot withdraw money yourself. You must ask your bank consultant to withdraw the money. You also earn interest in this account.

- Business account (Geschäftkonto): You need a business account if you are a business owner in Germany. A business account makes it easier to maintain your books. You use this account for business purposes only.

Best business bank accounts for freelancers in Germany ->

Best checking accounts in Germany ->

Other than these, Germany has three more types of bank accounts.

- Basic account (Basiskonto): This is similar to a checking account but with limited features. It is suitable for people with a poor or no Schufa score and for EU residents without a permanent address in Germany. Banks may refuse a basic account only on specific legal grounds and must communicate the refusal in writing (Zahlungskontengesetz, ZKG).

- Blocked account (Sperrkonto): It is a special account to prove financial stability when applying for a visa (e.g., for international students). Compared to a checking account, this account has a monthly withdrawal limit. This means you cannot withdraw more than the set monthly limit.

- Student account (Studentenkonto): Banks offer special bank accounts for students. Such accounts don’t have any fees. If you are 18 and above, you can open the account yourself. However, you need a legal guardian’s consent if you are below 18.

- Children’s account (Kinderkonto): Parents can open a bank account for their minor child. Such accounts often charge no fees. However, parents cannot use this account for themselves. Children get their own tax allowance on the interest earned.

How much tax do you pay on the bank interests in Germany ->

NOTE: Banks usually raise the fees of a child’s account automatically once your child crosses the age requirement. Thus, it’s best to open a new bank account with lower or no fees.

Free bank accounts in Germany ->

Who can open a bank account in Germany?

- EU residents without a permanent address in Germany. They can open a basic account (Basiskonto) with any German bank. However, a few fintechs, such as N26*, also offer normal checking accounts to certain nationalities.

- Residents (irrespective of nationality) who have a permanent address in Germany. The bank requires a registration certificate (Meldebescheinigung) as address proof.

How to get an address registration certificate in Germany ->

Every bank has its own eligibility criteria for opening a bank account. So, banks can reject your application without giving any reason, except for basic accounts, which require justification for the rejection.

Some of the main reasons banks reject opening a bank account are as follows:

- You don’t have good creditworthiness. Banks check your creditworthiness based on your Schufa Score, job contract, income, etc. People who are new to Germany have a hard time opening a bank account.

- The bank doesn’t open accounts for citizens

In general, it’s easier to open a bank account with Fintech banks (digital banks) like N26*, Revolut, and C24* because they often involve less bureaucracy and use fully digital application processes.

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

How can you open a bank account in Germany?

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

The process of opening a bank account in Germany is straightforward.

- Pick a bank you want to open an account with.

- You can open a bank account online or at the bank’s branch.

- In both cases, you must fill out the application form and submit the required documents.

- Verify your identity. You have five options:

- Go to the branch directly and have the bank employee verify your identity

- Post-Ident: In this case, you take your account opening documents and ID to the local Deutsche Post branch. They verify your ID and send the documents to the bank free of cost.

- Video-Ident: You must download a video-ident app. Someone on the video call will verify you and your ID.

- E-Ident: You need the electronic function of your ID card and a digital app to read it.

- Bank-Ident: Some banks allow you to verify your identity through your existing German bank account. In this method, the new bank asks you to log into your existing bank account and send a small amount to your new one.

- Receive details to open your account.

- If you applied to a traditional bank, expect an IBAN and a bank card (e.g., Girocard) via post within 5-7 days. In some cases, it may arrive later.

- If you applied to a digital bank or used video-ident, the bank account is usually opened immediately. Online banks like N26, C24, etc., give you instant online access after verification. However, some banks still send specific login details or your 2FA PIN by post, which may delay full access.

GermanPedia

8.1 out of 10

C24 Bank

02/2026

C24 offers a balanced, free checking account with all the important functions and transparent costs.

GermanPedia

6.3 out of 10

N26 Bank

04/2025

N26 used to be the best free checking account for expats in Germany. But now its free plan doesn’t offer key services that C24 does.

👑 Winner: C24 wins in all the categories except English support. We find C24 a better choice if you are fine without an English banking app.

What documents do you need to open a bank account in Germany?

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

- EU nationals living outside Germany: You can open a basic account. Few fintechs like N26 allow opening a normal checking account. You only need your personal ID.

- Non-EU nationals outside Germany: You cannot open a bank account in Germany.

- EU nationals in Germany: You need your ID and an address registration certificate (Meldebescheinigung) from the local municipal office (Rathaus).

- Non-EU nationals in Germany: You need a passport, a residence permit, and an address registration certificate (Meldebescheinigung).

Learn how to get a registration certificate from the local municipal office ->

Some banks may also request proof of employment and income (e.g., payslips, work contract) to open an account.

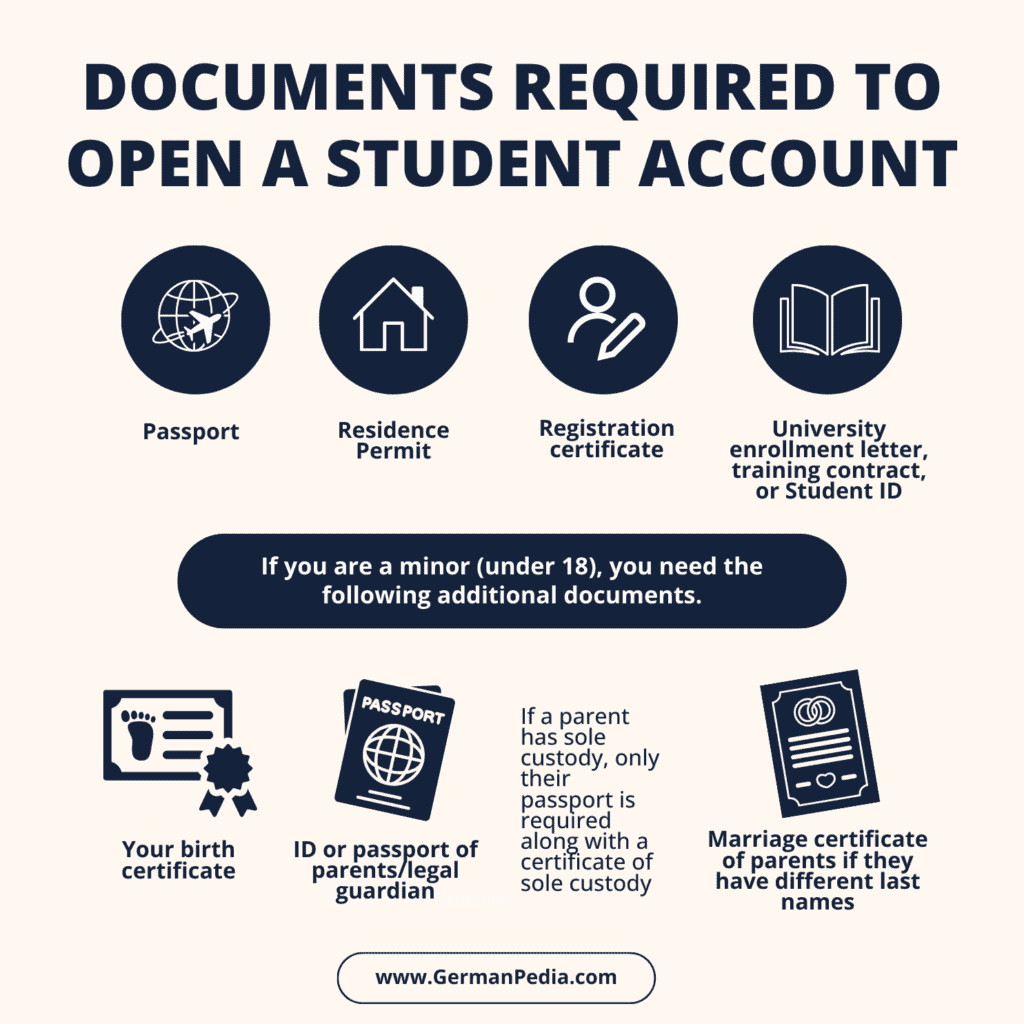

Documents required to open a student account

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

- Passport or valid ID

- Residence permit

- Address registration certificate (Meldebescheinigung).

- Proof of student status (e.g., university enrollment letter, training contract, student ID)

If you are a minor (under 18), you need the following additional documents.

- Your birth certificate

- ID or passport of the legal guardian (both parents, even if they are separated)

- If a parent has sole custody, only their passport is required along with a certificate of sole custody (Sorgerechtsbeschluss bei alleinigem Sorgerecht)

- If parents are unmarried but have joint custody, they must also submit a custody order

- Marriage certificate if parents have different last names

NOTE: If your child has a work contract despite their minor age, they can open an account without your consent (§ 113 BGB). However, they must bring a copy of their work contract and proof that you approved them to do this particular work.

Which banks in Germany accept expats?

- It’s easier for expats to open a bank account with an online bank (fintech).

- Some traditional banks like Commerzbank* and Deutsche Bank* are also expat-friendly.

Learn more about the best bank accounts in Germany ->

Can you open an account from outside Germany?

Whether you can open a bank account in Germany from outside Germany depends on your nationality.

EU nationals

- You can open a basic account (Basiskonto) without having a permanent address in Germany.

- You can open a normal checking account with fintechs like N26, but only if the bank supports your country of residence.

Non-EU nationals

No, you cannot open a bank account without having a permanent address (registration certificate) in Germany. Depending on your nationality, you may even need a residence permit to open the account.

What should you check about the bank before opening an account with it?

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

- Ensure the bank you choose has a German banking license. You can check if the bank has a German banking license on BaFin. All banks with German banking licenses offer statutory deposit protection of 100,000 € per customer.

- Check the bank’s fees. Traditional banks usually charge account maintenance and other fees (e.g., for withdrawals, transfers) based on your account type. Fintechs usually charge little to no fees.

- Do you get a free credit card? Most Fintech banks don’t offer a credit card at all. In traditional banks, you must apply for a credit card, and they charge a monthly fee. However, N26 and C24 offer a free MasterCard (debit card) that you can use for online payments like a credit card. You can compare free credit cards here.

- What other products or services does the bank offer? Some banks provide additional services (e.g., low international fees, savings accounts) that may be useful for you.

- Does the bank offer English support?.

Which bank offers the best checking account in Germany?

For expats who are settled in Germany

C24* is the clear winner. No bank offers the services C24 provides for free. The only drawback is that it’s only in German.

You can read our complete review of C24 here.

If you prefer a traditional bank, ING, Commerzbank*, and Deutsche Bank* are some good options.

For expats who are new to Germany (with no German skills)

Revolut and N26* are the best options. It’s easier for expats to open a bank account with them. Additionally, they offer free checking bank accounts with English customer support.

You can read our complete review of Revolut and N26 to learn more.

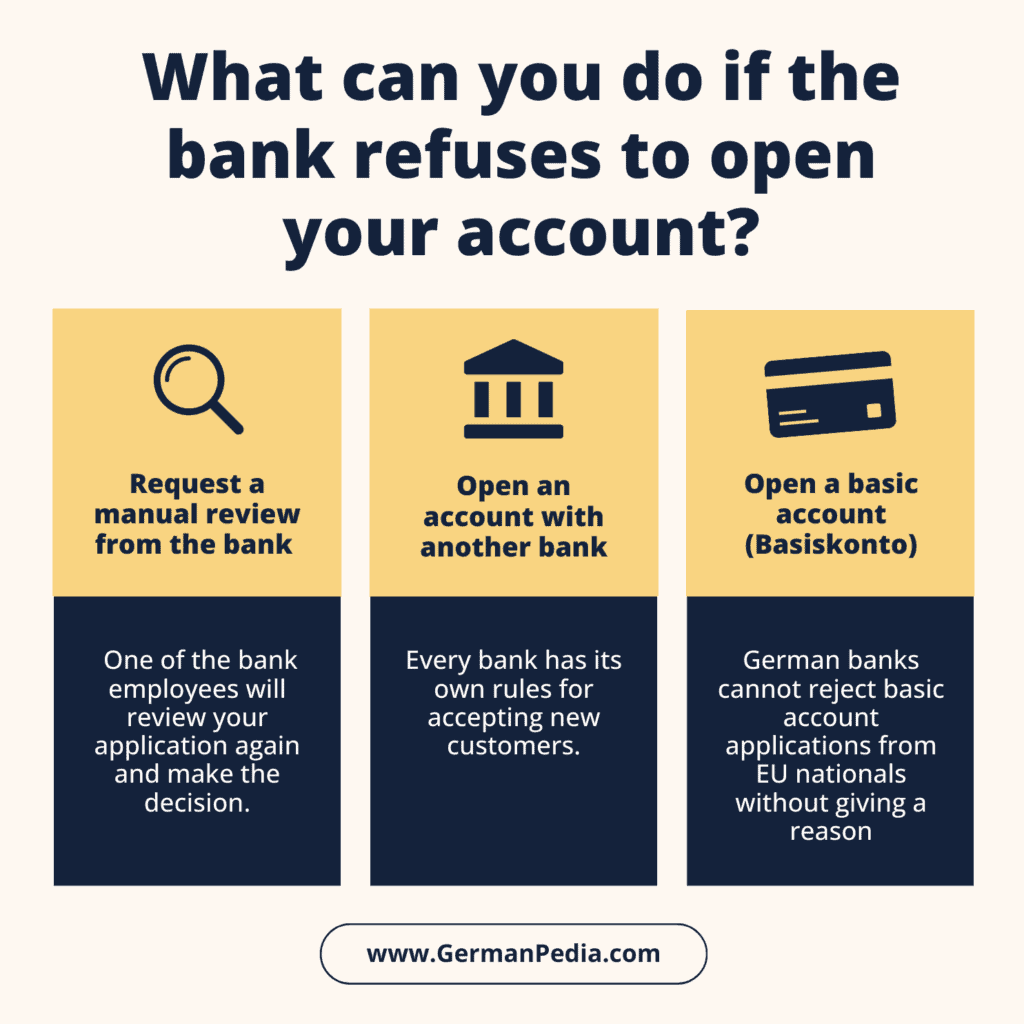

What can you do if the bank refuses to open your account?

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

- Request a manual review from the bank. One of the bank employees will review your application again and make the decision.

- Open an account with another bank. Every bank has its own rules for accepting new customers. So, don’t sweat if one bank rejects your application. There are tons of banks in Germany.

- Open a basic account (Basiskonto). German banks cannot reject basic account applications without giving a reason. This right applies to people who are legally residing in the EU. It also covers certain individuals without a fixed address within Germany (e.g., asylum seekers, homeless people), as long as they are of legal age and are legally competent.

You should also check your Schufa report for incorrect entries. Incorrect entries may reduce your Schufa score and cause banks to reject your account opening application.

FAQ

No, it’s not mandatory, but it is highly recommended. You can still use your foreign cards. However, this may incur extra or higher fees, and is not accepted everywhere. Having a German bank account would be more convenient for your daily spending.

Moreover, you need a German bank account to get a loan, to recieve salary when you start a job in Germany, etc.

Yes, you can open a bank account in Germany if you have no Schufa entry or Schufa score. This is normal for expats new to Germany.

– You already have a working payment account in another German bank

– You previously had a basic account with the same bank, but the bank terminated it due to nonpayment of fees or a breach of the terms.

– You used the bank account for criminal activity (e.g., money laundering)

– It will be against the bank’s due diligence to grant you an account

If you’re rejected for no valid reason, you can

– file a complaint with BaFin

– take legal action, or

– reach out to the consumer arbitration body (Verbraucherzentrale)

English-speaking lawyers in Germany ->

You can open a joint account with a partner or an acquaintance. Both of you can deposit money and pay shared bills (rent, groceries, etc.).

Some joint accounts allow both account holders to own the money. However, there are also accounts that allow only one person to own the balance, while the other has limited access to it. Always check the bank’s terms before opening a joint account.

Usually, additional services like credit cards, insurance, etc. that come with a bank account are not worthwhile for the following reasons.

– The account has a high monthly fee.

– The services or coverage provided by the insurance are not comprehensive.

– You are bound to pay using the bank’s credit card to avail the services.

However, some banks offer cashback. It could be beneficial depending on your monthly account fee and the monthly cashback you can expect.

More topics

References

- https://www.bafin.de/DE/Verbraucher/Bank/Produkte/Basiskonto/basiskonto_artikel.html

- https://www.bafin.de/DE/Verbraucher/Bank/Produkte/Tagesgeld/tagesgeld_node.html

- https://www.check24.de/girokonto/studenten-schueler/

- https://www.bafin.de/EN/Verbraucher/Bank/Produkte/Basiskonto/basiskonto_node_en.html

- https://www.finanztip.de/girokonto/kinderkonto/

- https://www.auswaertiges-amt.de/en/sperrkonto-388600