Key takeaways

- There are several benefits of investing in German real estate, such as forced discipline, a tenant paying the mortgage, inflation working in your favor, etc.

- Like any investment, real estate investment comes with risks. Thus, it’s vital to know these risks and how to manage them.

- Real estate investment also offers several tax advantages you won’t get if you live in the property yourself.

This is how you do it

- Educate yourself on how to buy a house and invest in German real estate before investing your hard-earned money. We have written a book on buying a house in Germany. It explains the complete buying process, how to invest in German real estate, and offers expert tips that'll save your thousands of euros.

- Understand the risks of investing in German real estate. Prepare yourself to manage these risks.

The AI overview and answers are as good as the sources it uses.

To ensure you get AI answers from a deeply researched, maintained, and up-to-date source, add GermanPedia to your preferred sources.

Table of Contents

9 benefits of investing in German real estate

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

Investing in real estate may seem scary to some, but if done correctly, it can be the most rewarding investment. Here are nine benefits of investing in real estate.

- Discipline: Most people are not disciplined long-term investors. However, real estate investment forces discipline, as you can’t buy and sell a property in seconds. While this may seem a drawback at first glance, it’s one of real estate’s greatest strengths. This encourages long-term thinking and commitment.

- Someone pays for your purchase: Real estate is the only investment where someone else pays you a significant part to build your asset. First, the banks lend you the money to buy a real estate. Afterward, a tenant pays the rent you can use to repay the mortgage.

- Inflation is good: Most people don’t like inflation. Though inflation increases the prices of products, it also reduces the real value of the debt. This means that over time, your rental income will increase with inflation. However, the real value of your debt will decrease.

- Easy to build on existing investments: As you add a real estate investment in your protfolio. Adding another property gets easier for two reasons. Rental income increases your total income. Over time you repay part of the debt. This increases your asset value, which helps you get mortgage for another property.

- Leverage: Real estate allows you to use borrowed money to control a valuable asset. With a relatively small down payment, you can own a property worth far more, amplifying your returns.

- Tax Benefits: You can deduct the expenses of buying, maintaining, and running a rental property, such as mortgage interest, property tax, insurance, renovation costs, etc. In addition, you can depreciate the property over time. This saves you a lot in taxes. Moreover, you don’t pay capital gains tax if you sell the property after ten years. You don’t get these tax advantages when buying stocks.

- Everyone needs a roof: Housing is a basic human need, making investing in real estate future-proof.

- Passive income: Once the mortgage is repaid, you’ll earn the rental income without actively working for it.

- You understand where you invest: Many buy a stock without understanding the underlying business or company. This is not the case with real estate. You know the product well because you use it daily (living in a home). You know the challenges, risks, user behavior (as you are a user yourself), and benefits of owning one.

Let’s understand each benefit in detail.

NOTE: Every investment that offers real opportunities involves risks. The trick is to master how to deal with these risks.

#1 Real Estate investment enforces discipline

You’re not alone if you’ve ever bought a stock and sold it the next week. Most people struggle to stay disciplined when it comes to investing.

It’s easy to get excited by the highs and panic during the lows.

Why Is Discipline So Hard?

Since the beginning of human history, our brains have been wired to focus on immediate rewards. This made perfect sense in the Stone Age; survival depended on acting fast.

If you found food, you ate it right away. Waiting for a “better opportunity” or planning months ahead wasn’t an option. This instinct of prioritizing what we can have now over what we might get later is still part of our biology.

It’s deeply embedded in our DNA, even though our world has changed dramatically.

On top of this, financial apps make it easy to buy and sell in seconds. You can track markets in real time, follow trending stocks, and react instantly to the news.

It’s never been easier to chase short-term wins.

These tools make it feel normal or even smart to act on impulse. The problem is that this kind of behavior often hinders long-term financial success.

The result of poor discipline is

- You buy when the market is up.

- You sell when it crashes, as it feels like the safe thing to do.

- You jump from one strategy to another, never giving any approach enough time to work.

A study by DALBAR shows that many investors hurt their returns by trying to time the market. On the other hand, investing consistently through all market conditions is less stressful and offers better returns in the long run.

That’s one reason why real estate investment can be such a powerful tool to save for your future.

What makes investing in real estate different?

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

- Monthly Payment Mechanism: Real estate creates automatic discipline through mortgage obligations. You must pay the monthly installment regardless of your personal circumstances or market conditions. This helps you stay consistent and build equity steadily over time.

- Serious consequences of missing a payment: You want to buy the latest iPhone, so you skip investing your money for one month. Later, you plan a trip, and another month goes by without investing. This is not possible in real estate. If you miss a mortgage payment, you face serious consequences. In short, you are forced to spend what you are left after investing.

- You can’t sell real estate in seconds: Unlike stocks, real estate transactions take weeks or months to complete. This built-in delay prevents impulsive selling and helps you stay invested long-term. High transaction costs (typically 5-10% between buying and selling) further discourage frequent trading.

- Psychological Commitment: Unlike stocks, you develop emotional attachments to the properties you purchase. You view them as long-term assets rather than trading vehicles. This mindset shift encourages patience and motivates you to do research. People often research a lot more before buying a property than they do when buying a stock. This alone increases your probability of success drastically.

What initially appears to be real estate’s disadvantage (illiquidity and commitment requirements) is its greatest advantage for most investors. It eliminates the option of impulsive trading and forces you to accumulate wealth over time.

#2 Someone is paying for your real estate investment

The best part of investing in real estate is the rent you receive every month.

The rent is often enough to cover a large portion or even all of your monthly mortgage payment. That means someone else is helping you pay off the mortgage.

Let’s say your mortgage is €1,000 a month. If your tenant pays you €850 in rent, you only add €150 from your pocket to pay the mortgage.

Over the years, that small contribution has helped you build an asset worth hundreds of thousands of euros.

Moreover, the rental income is predictable and stable. Even during housing market downturns, your tenant continues paying rent.

Once your property is paid off, you’ll have a reliable income source.

#3 Inflation is your friend in real estate investment

Inflation is often considered bad. However, as a real estate investor, inflation is your powerful ally.

On the one hand, inflation decreases the purchasing power. At the same time, it also decreases the real value of debt.

In other words, your rental income will increase over time due to inflation. However, your mortgage payment remains fixed (assuming a fixed-rate mortgage).

This means you’ll pay the same monthly installment in year 10 as in year 1. But you’ll receive more rental income in year 10 than in year 1. This improves your cash flow, reduces debt faster, and builds equity.

Not only rental income, but your income from work will also increase with time.

In the past twenty years, the average salary in Germany has increased by 2% per annum. This means a significant monthly installment today will feel much more manageable ten or twenty years later. This is all thanks to inflation.

#4 Building on existing real estate investments gets easier

Buying the first property is usually the most challenging part. But after that, things fall in your favor.

The rental income increases your overall revenue, and your asset value increases as you repay debt. Both of these affect your credit score positively.

In other words, your first property can help you qualify for the next one.

Here is an example. Suppose you bought a two-room apartment for 250,000€.

- Your monthly installment is 1250€ (2% loan repayment and 4% interest).

- You receive a total rent of 1000€.

- You increase the property’s rent on average by 2% every year.

This means after 5 years, your rental income will increase to 1100€. At the same time, you reduced your debt by 11.5% or repaid 28,800€ in 5 years.

Suppose your property’s value increases during this time; your asset value will increase further.

If you apply for a mortgage for a second property, your increased net worth will work in your favor. It’ll be easier for you to get a mortgage for the second property.

Similarly, as the number of properties in your portfolio increases, buying the next properties gets easier.

#5 You utilize leverage to its best in real estate investment

One of the most significant advantages of real estate as an investment class is leverage.

Leverage is the ability to use borrowed money to control a high-value asset.

Unlike stocks or mutual funds, where you typically invest only the money you have, real estate allows you to make a relatively small down payment and benefit from the full appreciation and rental income of the entire property.

Here’s a simple example of leverage at work.

- You buy a property worth 250,000€

- You get 100% financing, which means the bank lends you 250,000€.

- Your monthly installment will be 1250€, assuming 2.4% loan repayment and 3.6% interest.

- 750€ of the monthly rent will be the interest you pay to the bank, and 500€ will be used to repay the mortgage.

- You have a monthly maintenance and renovation cost of 100€.

- So, your total monthly costs will be 1350€ (1250 + 100).

Case 1: You rent the property for at least 1350€

In this case, the property will pay for itself. Here is how.

500€ used to repay the mortgage is your saved capital. This converts to 6000€ per annum.

Your additional cost (Nebenkosten) to buy the property is 25,000€ (10% of 250,000). This is the money you invested from your pocket.

In this case, your return on the invested capital (25,000€) will be 24% (6000€ / 25,000€).

Let’s examine the case where you receive a lower rent.

Case 2: You rent the property for 1000€

In this case, you must bring the remaining amount, i.e., 350€ (1350€ monthly expenses – 1000€ rental income), from your pocket. This reduces your saved capital from 500€ in the previous case to 150€ (500€ mortgage repayment – 350€ your own cash).

The total annual savings will be 150€ x 12 months = 1800€ per annum. So, your return on investment (ROI) will be 7.2% (1800€ / 25000€).

In short, you need at least 850€ (1350€ total cost – 500€ mortgage repayment) in rent to cover the expenses. Any amount above this amount goes into building your savings.

You’ll not get an ROI of 7% to 24% in any other investment product. This is the power of leverage.

Moreover, no one will lend you money for stock or crypto manipulation. However, banks will gladly lend you hundreds of thousands of euros to buy a property.

The reason for this is that banks have property as security. So, if you default on your mortgage payments, the bank will sell the property to recover the loan.

Your rental income will also increase due to inflation as time passes. However, your monthly installments will stay the same. Hence, further increasing your ROI.

Finally, once you have repaid the mortgage in 20 years, you have built an asset worth hundreds of thousands and secured a stable monthly income.

Risks that come with leverage

Leverage has benefits and risks. Here are some of the main risks that can bankrupt you.

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

- You bought a property where no one wants to live. In this case, you’ll have a hard time finding a tenant. Thus, you are left with a property that depreciates in value and must pay the mortgage yourself. If you can’t repay the mortgage, you’ll default and ultimately go bankrupt.

- You overpaid for the property. This means you borrowed more money than the value of the real estate. If you sell the property, you can’t recover what you paid and are left with debt.

- You have no cash reserve. If a tenant stops paying the rent, you’ll default on your monthly installments.

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

Thus, you must know how to manage these risks. Here are some ways to do so.

- Buy the property where people want to live. People usually live where they work. Hence, a city with several companies offering employment is ideal for buying a property. This ensures you won’t have trouble finding good tenants who pay rent on time.

- Borrow the amount you can repay, even if you don’t get rental income for a few months. There are always unknowns in the investment. You may get stuck with a tenant who doesn’t pay rent or can’t find a tenant for a few months. Every landlord faces such situations in their lifetime. This is why you must have enough cash reserves or income to pay the monthly installments even if you don’t receive rent for a few months.

- Buy multiple smaller properties over a single big property. Suppose you can get a mortgage of 500,000€. In this case, you can buy one property worth 500,000€ or two properties worth 250,000€ each. By purchasing multiple properties, you reduce your risk. Thanks to diversification. Suppose you have one property, and your tenant doesn’t pay rent. In this case, you must pay the whole installment yourself. On the other hand, suppose you have two properties. In this case, it’s rare that tenants of both properties will stop paying the rent simultaneously.

- Pay the right price for the property. Real estate is similar to stocks in this case. In stocks, you profit if you buy low and sell high. The same applies to real estate. Thus, knowing you are paying a fair price when purchasing a property is vital.

Here are some words of wisdom from famous investor Robert Kiyosaki, author of Rich Dad Poor Dad. He is a vocal proponent of using leverage to build wealth. He often says that debt, when used responsibly, is a powerful tool:

“Good debt makes you rich, bad debt makes you poor.”

Kiyosaki boasts that real estate is the perfect instrument for using “good debt.” A debt that pays for itself through rental income while also appreciating in value.

NOTE: Don’t confuse buying a property to live in it with an investment property. Your own home is not an asset but a liability.

#6 Tax benefits of investing in German real estate

I can write a book explaining the tax benefits and optimization techniques of real estate investing. To keep it short, here are some significant tax advantages of investing in German real estate.

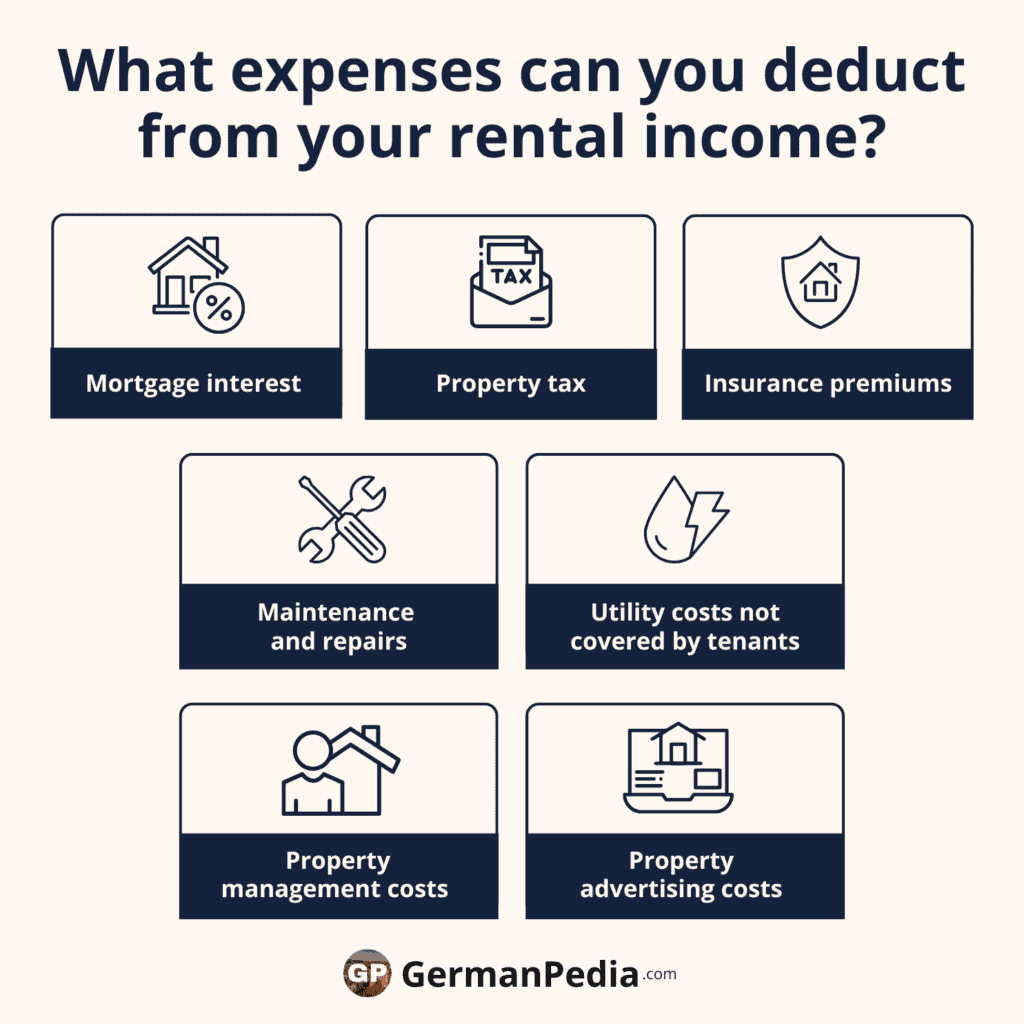

Expense Deductions (Werbungskosten)

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

You can deduct all the expenses related to your rental property from your rental income. This includes:

- Mortgage interest (Darlehenszinsen): The interest portion of your mortgage payments is fully deductible.

- Property management costs (Hausverwaltungskosten): Fees paid to property managers.

- Insurance premiums (Versicherungsprämien): Building insurance, legal insurance, etc.

- Property tax (Grundsteuer): Annual property tax payments.

- Maintenance and repairs (Instandhaltung und Reparaturen): Regular upkeep and necessary repairs.

- Utility costs not covered by tenants (Nebenkosten): Any utilities you pay as the landlord.

- Property advertising costs (Vermietungskosten): Expenses for finding tenants.

Please note that this is not an exhaustive list. However, in principle, you can deduct all the expenses incurred to generate the rental income. This is similar to a business where you can deduct all the costs incurred to generate revenue.

Example: If you earn €12,000 in annual rental income and have €7,000 in deductible expenses (mortgage interest, insurance, repairs, etc.), you only pay income tax on the remaining €5,000.

Property Depreciation (Abschreibung/AfA)

One of the most powerful tax advantages of real estate investment in Germany is property depreciation.

Every property requires renovation after some time, which costs money. This is why the tax office allows real estate investors to depreciate the value of the property over time.

Here is how much you can depreciate every year.

- Buildings constructed before 1925 can be depreciated at 2.5% annually over 40 years.

- Standard residential buildings constructed between 1925 and 2023 can be depreciated at 2% annually over 50 years.

- Buildings constructed after 2023 can be depreciated at 3% annually over 33 years.

- Commercial properties can be depreciated at 3% annually over 33 years

Example: If you purchase a residential property built after 1925 for €300,000 (with the building value assessed at €240,000 and land value at €60,000), you can deduct €4,800 (2% of €240,000) from your taxable rental income each year for 50 years. Note that only the building can be depreciated, not the land.

The principle behind depreciation is that in 50 years, your property will be unlivable and require extensive renovation.

Thus, you should save part of your rental income for such expensive renovations down the road. As a rule of thumb, you should save 10% of your rental income for repairs and renovations.

Capital Gains Tax Exemption (Spekulationssteuer-Befreiung)

Unlike stocks, you don’t pay any tax on the profit from the sale of real estate in the following cases:

- You held the rental property for at least 10 years before selling.

- You used the property yourself in the year of sale and in the two previous calendar years.

Example: If you buy a property for €200,000 and sell it after 11 years for €300,000, the entire €100,000 profit is tax-free. If you had made the same profit on stocks, you would typically pay 25% plus a solidarity surcharge (about €26,375 in taxes).

If you sell the property within 10 years, you pay tax on the profit, which is based on your personal income tax rate.

Example

Property details:

- Purchase price: €350,000 (Building value: €280,000, Land value: €70,000)

- Annual rental income: €14,400 (€1,200 monthly)

- Mortgage: €250,000 at 2.5% interest

Annual tax deductions:

- Mortgage interest: €6,250

- Property tax: €500

- Insurance: €600 (Legal insurance, homeowner’s insurance, etc.)

- Maintenance/repairs: €1,200

- Property management: €600

- Building depreciation: €5,600 (2% of €280,000)

- Total deductions: €14,750

In this scenario, despite generating €14,400 in rental income, the investor would show a paper loss of €350 for tax purposes. This means you won’t pay any tax on your rental income.

Other tax regulations apply based on your situation, such as the “three object limit (Drei-Objekt-Grenze).” We cannot cover all the rules in this guide. Thus, we highly recommend consulting a tax advisor for personalized advice and to optimize your tax returns.

#7 Everyone needs a roof

Housing is among the most essential human needs, alongside food and water. The need for shelter never becomes obsolete, making real estate inherently future-proof. This basic human necessity offers several key advantages for real estate investors:

- Consistent demand: Even during economic downturns, people need a roof and prioritize paying rent over buying a car.

- Inflation protection: Rents typically rise with inflation over time.

As a real estate investor, you can enjoy these benefits only if you buy the property in an area where people want to live.

Thus, the famous phrase “location, location, location” remains the golden rule of real estate. Please don’t confuse it with buying a property in the city center of a big city. A small town with good employment opportunities is also a good location.

Here are a few things that make an area attractive.

- Access to work: Despite having a home office, most people live in the city where they work. Thus, choose a city with thriving job opportunities. It’s vital that the city has several employers and not a single major employer. If the major employer moves their operation elsewhere, people will also move. Thus, you will have a hard time finding tenants for your property.

- Educational opportunities: Many parents pay a premium to live in an area with good schools.

- Healthcare access: Nearness to medical facilities matters increasingly as populations age

- Safety: Crime rates and neighborhood security significantly affect property values

- Amenities: Access to shopping, dining, entertainment, and green spaces enhances desirability

- Access to public transport is vital for students and many young workers.

Ultimately, the parameters you prioritize when choosing an area depend on your tenant’s persona: Do you want to rent to a family, an old couple, students, or young employed couples?

You can learn more about it in our guide on how to find the right tenant in Germany.

Only by picking the correct location can you secure a monthly rent.

Moreover, residential rents usually remain stable and increase with inflation. This is because moving is expensive and requires a lot of effort.

The two main reasons for changing residence are a job change or finding a lower-rent property.

In Germany, people prefer staying with an employer for at least 2 to 3 years. There are also employers like Bosch, S&P, Detusche Bank, etc., where employees remain loyal to the company until retirement. Thus, the first factor supports your rent stability.

Rent in Germany has increased consistently over the past 30 years. Moreover, demand and supply set the pricing of any product or service. The same applies to rent.

You’ll only reduce the rent if you can’t find a tenant. The main reasons you’ll have a hard time finding a tenant are a bad location or a property in poor condition. Both of these factors are in your control.

To conclude, housing is a basic need. Home prices may fluctuate significantly, but rents tend to rise steadily. However, to benefit from this, you must buy a property where there will continue to be jobs and thus demand for housing.

#8 Secure passive income source by investing in German real estate

Real estate can be a great source of passive income.

Yes, you have to maintain the property. However, this is not a full-time job. Moreover, you can hire a company to manage the property for you.

Thus, once you pay off the mortgage, you secure a reliable source of income without actively working for it.

Over time, you can create a portfolio that generates substantial monthly income with minimal ongoing effort. However, to secure your passive income and avoid financial troubles in the future, you should create a maintenance and renovation reserve.

Create maintenance and renovation reserves

You must adequately account for ongoing and future property expenses. Otherwise, you risk financial trouble when a hefty renovation bill lands in your postbox.

Not setting aside adequate maintenance reserves is the most common mistake among new investors. Ensure you are not among them.

The next question you may ask is how much you should save for maintenance. Here are two ways to calculate it.

Maintenance reserves according to the “Calculation Ordinance of the Housing Act (WoBauG)”

The table below shows how much you should save each year based on your property size and age. The older and bigger the property, the more you should save.

This is one reason why investing in smaller properties, such as 1- or 2-room apartments, is beneficial over buying single-family houses or 4-room apartments.

| Age of the property | Maintenance reserve per square meter and year | Yearly maintenance reserve for a 55sqm property |

|---|---|---|

| Not older than 22 years | 7.10 €/m² | 390€ |

| Older than 22 years | 9 €/m² | 495€ |

| Older than 32 years | 11.50 €/m² | 632€ |

NOTE: The maintenance amount calculated using this table is the minimum sum you should save to avoid financial trouble in the future.

Peters’ formula

Many experts use “Peters’ formula” to calculate maintenance reserves. This formula is particularly suitable for properties with known production costs per square meter.

In Germany, the approximate production cost per square meter is 36.7€.

The formula assumes that 1.5 times the value of the production costs will flow into maintenance within 80 years. However, a large portion of this cost (70%) is required to maintain the common parts of the property, such as apartment building walls, roof, boiler, etc.

If you own an apartment, you must save 30% of the total cost. Your “homeowners’ association (Hausverwaltung)” saves the rest as reserves (Rücklage).

Example:

- Property size: 55sqm

- Production cost per sqm: 36.7€

- Total yearly reserve per Peters’ formula: 36.7 x 1.5 x 55 = 3027€

- 70% of the total reserve is necessary to maintain the common parts of the building: 2120€ (176€ per month) -> You pay Hausverwaltung a monthly maintenance fee (Hausgeld). Part of this fee is saved for future renovations. This is called Rücklage in German.

- 30% of the total reserve is needed to maintain the apartment: 907€ (75.5€ per month)

Based on the two formulas, you should save between 400€ and 900€ as a maintenance reserve for a 55 sqm property.

#9 You understand where you invest in real estate investment

Many people think they don’t know anything about real estate. However, this is not entirely true.

You know more than you give yourself credit for.

Unlike stocks or complex pension plans, you experience housing daily. You live on a property yourself and have lived on it since birth. This familiarity provides natural insight into property value, desirability factors, and potential problems.

You know the importance of property layout, adequate storage, natural light, and sound insulation. This built-in knowledge helps you evaluate a property from financial and practical perspectives.

Complete control when buying a property

When buying stocks, you only have access to publicly available data. You have no insider information and current company dynamics.

Moreover, most people don’t spend enough time understanding the underlying business.

Ask yourself when you read the financial report of a company whose stock you bought.

Suppose you bought VW stocks. Do you know the dynamics of its competitors, what next products VW and its competitors are launching, how geopolitics will impact VW, who are VW suppliers, etc.? Understanding this requires a lot of time and effort and is complex.

On the other hand, evaluating a property is relatively simple compared to stocks and other investment products, such as pension plans.

Here is how you can thoroughly assess a property.

- Personal inspection: You can visit the property and assess the layout, its condition, natural light, noise levels, etc.

- Hausverwaltung (property management): They are responsible for maintaining the property building and common areas. They can provide maintenance histories, information about previous issues, and insights about the building community. You can ask them what renovations are planned or required in the next ten years, whether they have enough cash reserve (Rücklage) to perform them, etc.

- Professional Gutachter (property appraiser): These experts can identify potential structural issues and code violations and even tell the property’s fair market price. They charge you between 600€ and 1200€, depending on the property size, location, and whether you want a written report. They are liable for their report. This means they must pay the damages if they didn’t mention an expensive defect in their report.

- Document review: Examining property documents reveals crucial information:

- Grundbuch (land registry) entries showing ownership history, existing mortgages, etc.

- Energy performance certificates

- Building plans and permits

- Maintenance records

- Homeowners association protocols (if applicable)

This level of pre-purchase investigation gives you confidence in your investment decision.

Buying a home in Germany is time-consuming and involves a lot of money. There are a lot of things you must know before buying a property.

Thus, we wrote a book on buying a house in Germany to make it simple for you. Read it to learn everything there is about buying a property in Germany.

Master German Home Buying Process

in 12 Days For FREE

- Learn complete process of buying a house in Germany and how to invest in German real estate.

- Understand mortgage process, property documents and evaluation, and more.

- Expert tips that’ll save you thousands of euros.

- Know average renovation costs in Germany to plan and negotiate better.

Complete control over the operation

Unlike stock ownership, where your influence on the company’s operation is minimal unless you’re a major shareholder, real estate puts you in the driver’s seat.

You decide:

- When and how to renovate to increase property value

- Which improvements will yield the best returns – renovate the kitchen, modernize the bathroom, or improve the energy efficiency, etc?

- What rental rates to set

- Which tenant to choose

- When to refinance and on what conditions

This control lets you directly influence your investment’s performance rather than passively hoping for positive outcomes.

You can even take a renovation loan to execute your renovation plans.

Even modest improvements like bathroom renovation costing €10,000 might increase your property value by €15,000-20,000 while simultaneously justifying higher rental rates.

Adding a fully functional kitchen improves the attractiveness of your property for expat families or couples. Similarly, based on your ideal tenant persona, you can upgrade your property to enhance its appeal and demand higher rent.

Remember that you can deduct all these expenses from your taxes, which further increases your return on investment.

More topics

- How to buy a house in Germany?

- What makes a good investment property in Germany?

- Risks of investing German real estate and how to manage them?

- How do you find a good Mortgage in Germany?

- Understanding property documents

- Evaluating property online

- Evaluating property onsite

- How do banks calculate mortgage interests?