Key takeaways

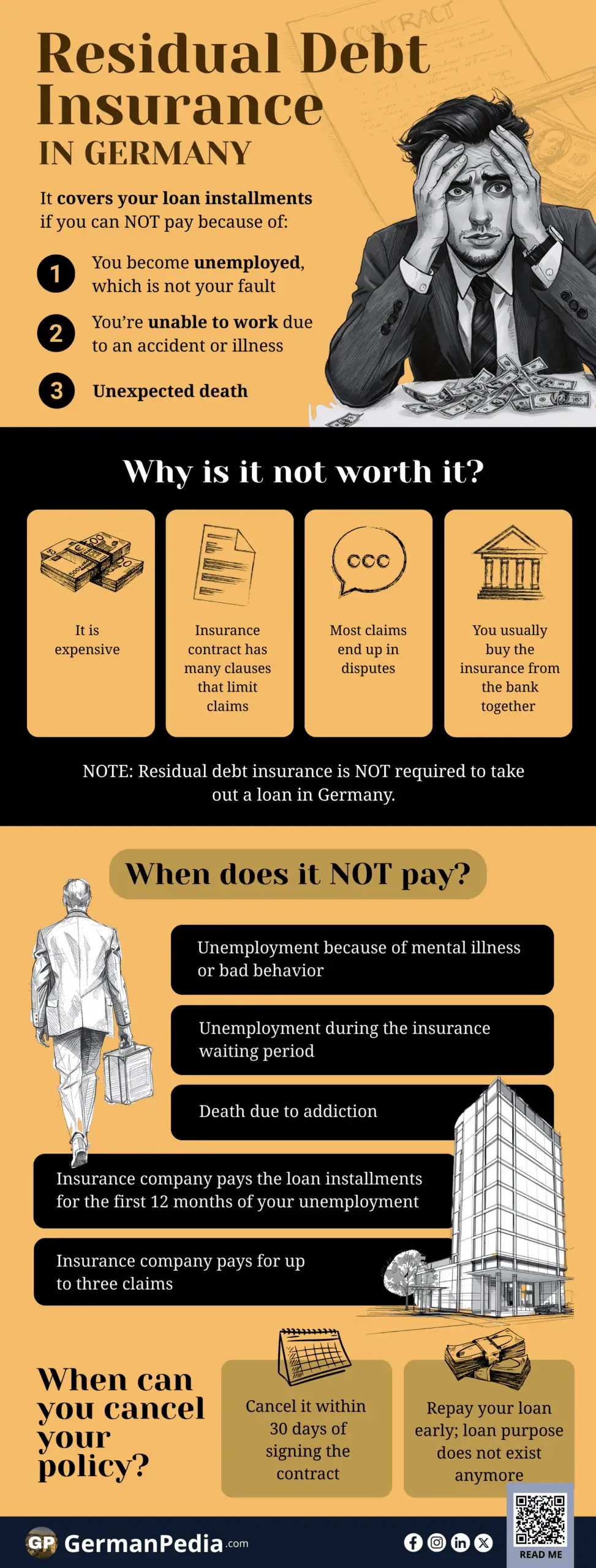

- Residual debt insurance covers your loan payments if you cannot pay them as you become unemployed, unable to work due to illness, or in the event of death.

- Residual debt insurance isn’t worth it as it’s expensive and doesn’t offer the right performance.

- You can take term life insurance and/or occupational disability insurance instead.

This is how you do it

- Taking residual debt insurance is not mandatory. If your bank advisor tells you otherwise, talk to their supervisor or submit a complaint online at Verbraucherzentrale or Bafin.

- Check the total loan costs instead of the interest rate while comparing loan offers.

- Compare the loan offers on comparison portals: Verivox*, Finanzcheck*, and Check24*.

The AI overview and answers are as good as the sources it uses.

To ensure you get AI answers from a deeply researched, maintained, and up-to-date source, add GermanPedia to your preferred sources.

Table of Contents

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

What is residual debt insurance (Restschuldversicherung)?

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

Residual debt insurance covers your loan installments if you cannot pay as

- you become unemployed, which is not your fault

- you are unable to work due to an accident or illness

- unexpected death.

As good as it may sound, residual debt insurance is not worth it. It’s expensive, and most claims end up in disputes.

New regulations regarding residual debt insurance

- Since July 2022, the commission the bank receives from selling residual debt insurance has been capped at 2.5% of the loan amount.

- Since 1 January 2025, you can take out residual debt insurance seven days after taking out the loan (Future Financing Act). This way, it’s clear to the borrower that taking out residual debt insurance has nothing to do with the loan and its conditions. If you get residual debt insurance before 7 days of taking out the loan, the insurance contract is void, and you get the money back.

Is residual debt insurance worth it in Germany?

No, residual debt insurance isn’t worth it for the following reasons.

- It’s expensive

- The insurance contract has many clauses that limit the insurance benefits and the scenarios in which you can claim it.

- Most claims end up in disputes.

- You usually buy the insurance from the bank together with the loan. Thus, you don’t have the option to compare and find the right policy for you.

- Bank consultants are not insurance experts. They can not provide you with professional advice or determine if you really need the insurance.

As per the data from the German federal government, the residual debt insurance companies covered the loan installment of only 0.3% of the contracts [2].

Why do banks and loan consultants pressure you to take residual debt insurance?

Residual debt insurance (Restschuldversicherung) is a very profitable business for banks. According to Bafin (the banking supervisory authority), banks received more than 50% of the insurance premiums as commission in 2019.

So, you can imagine why your bank consultant is so keen on selling you residual debt insurance.

Is taking residual debt insurance compulsory?

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

No, residual debt insurance is not required to take out a loan in Germany. If your bank consultant or broker says otherwise, get it in writing or talk to their supervisor.

Forcing clients to take residual debt insurance is very common when taking out a mortgage in Germany. The insurance makes the mortgage very costly.

You may not notice the cost if you look only at the interest rate. You must check the total cost before signing the contract.

If the bank still forces you to get residual debt insurance, file a complaint with Verbraucherzentrale. Verbraucherzentrale is a central customer advisory in Germany that helps resolve consumer complaints.

You can also submit an official complaint to Bafin. Bafin is the banking supervisory authority in Germany.

Do you need residual debt insurance in Germany?

First of all, residual debt insurance isn’t worth it. Moreover, you don’t need it if you already have occupational disability insurance, term life insurance, or statutory unemployment insurance.

How much does residual debt insurance in Germany cost?

The cost of residual debt insurance depends on the loan amount and the insurance provider. The table below shows the residual debt insurance costs on a 10,000 € loan per Finanztip’s calculations.

| Bank / Insurance | Insurance costs (Percentage of the loan amount) | Interest on loan |

|---|---|---|

| SWK/SOGECAP and SOGESSUR | 1255.48 € (≈13%) | 1896.36 € |

| ING/AXA France Vie and the AXA France IARD | 535.8 € (≈5%) | 2504.03 € |

| Hypovereinsbank/LifeStyle Protection Lebensversicherung | 912.47 € (≈9%) | 2863.52 € |

| Degussa/Creditprotect | 1146.27 € (≈12%) | 3415.10 € |

As you can see, residual debt insurance costs drastically increase the total loan cost. This is why you should always check the total loan cost instead of the interest rate when comparing the loan offers.

Compare the loan offers on comparison portals: Verivox*, Finanzcheck*, and Check24*.

However, you may find that it’s hard to determine what residual debt insurance actually costs. The bank doesn’t show the costs transparently in the contract. This is why you must look at the total repayment amount to understand how much the loan really is.

Here’s an overview of how residual debt insurance increases interest rates. Continuing with the above table.

| Bank | Insurance costs | stated effective interest rate | Actual effective interest rate with insurance |

|---|---|---|---|

| SWK | €1255.48 | 6.49% | 11.96% |

| ING | €535.80 | 9.56% | 11.55% |

| HypoVereinsbank | €912.47 | 9.99% | 13.71% |

| Degussa | €1146.27 | 11.46% | 17.12 % |

When does residual debt insurance not pay?

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

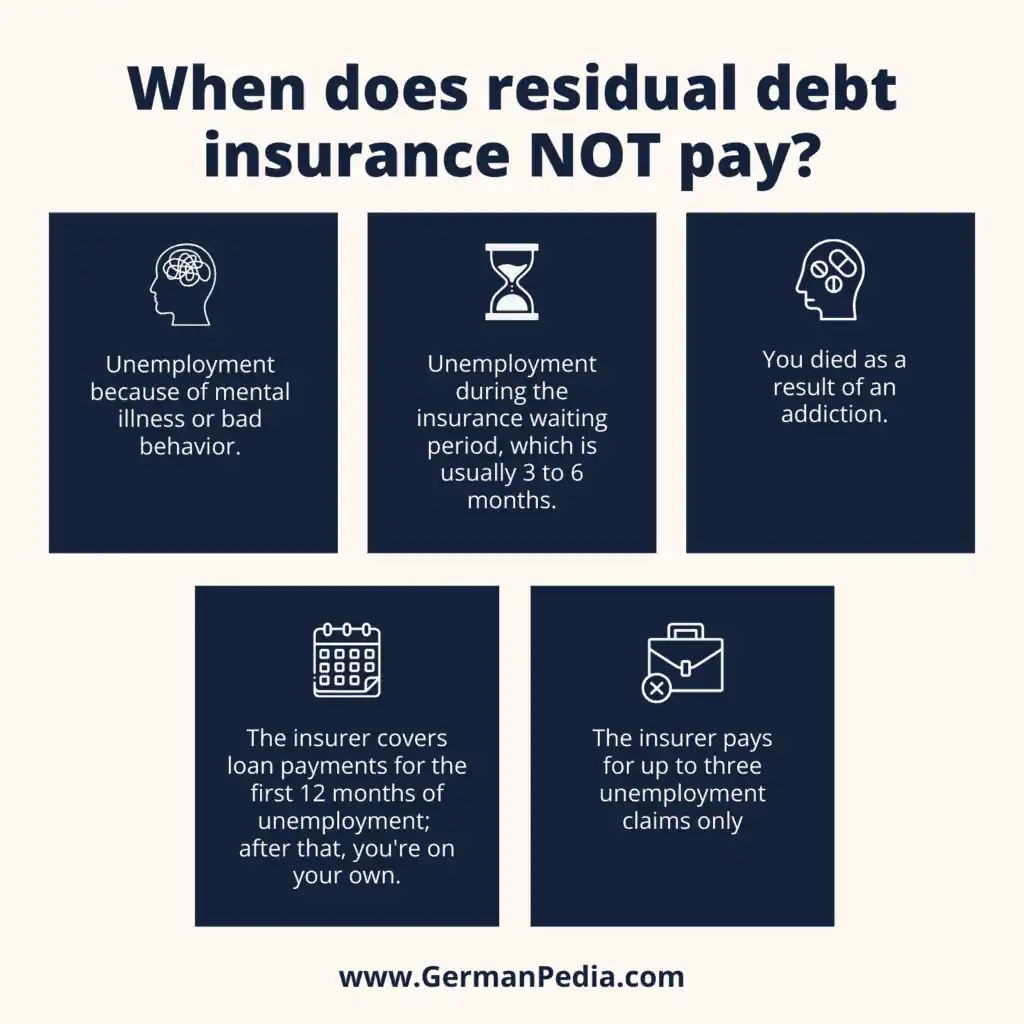

Like any insurance policy, residual debt insurance contracts have many clauses you should know. The insurance company doesn’t pay the loan installments in the following cases.

- You become unemployed because of mental illness or bad behavior.

- You become unemployed during the insurance waiting period, which is usually 3 to 6 months.

- You died as a result of an addiction.

- The insurance company pays the loan installments for the first twelve months of the insured event (e.g., unemployment, disability). After that, you must pay on your own.

- The insurer pays for up to three claims. If you become unemployed a fourth time, the insurer will not pay.

Residual debt insurance policies vary widely. One insurer may cover certain situations that another excludes entirely.

NOTE: Not all exclusion clauses are valid legally. Some provisions are too vague for the Federal Court of Justice.

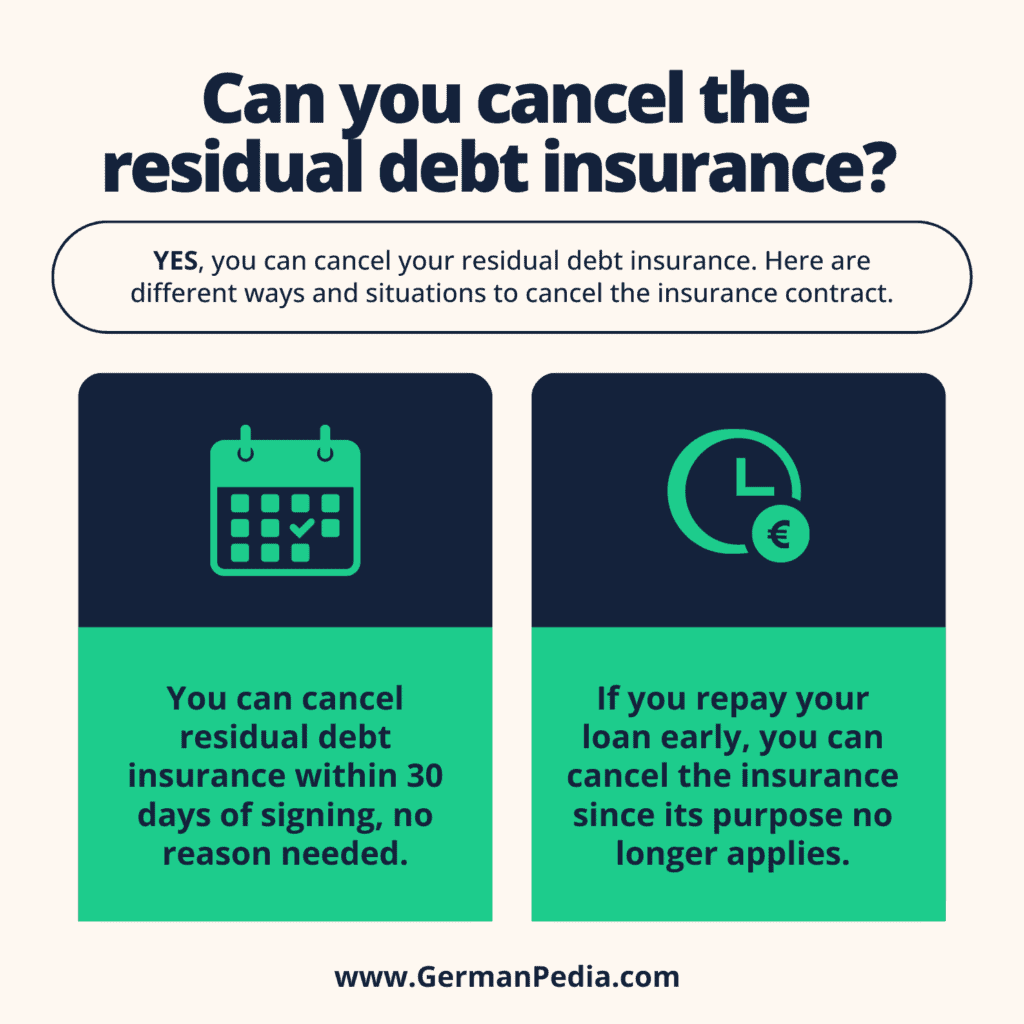

Can you cancel the residual debt insurance?

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

Yes, you can cancel your residual debt insurance.

Here are different ways and situations to cancel the insurance contract.

- Cancel the residual debt insurance policy within 14 or 30 days of taking the residual debt insurance. You can cancel the insurance within 30 days if your policy offers death benefits (§ 152 para. 1 VVG). Otherwise, you must cancel within 14 days (§ 8 para. 1 VVG). This is also called Widderrufsrecht in Germany. You don’t need to provide any reason for cancelling the contract within this period.

- If you refinance or repay your loan early, you can cancel the insurance contract. The reasoning is that the purpose of taking the insurance (i.e., loan) no longer exists.

- Avoid taking on new residual debt insurance unless it makes sense for your situation. Many insurers will recommend this. However, it usually leads to more expensive insurance and restarts your waiting period.

- You can cancel both the loan and the insurance together if the bank made mistakes in their cancellation instructions in the contract. However, you must repay the loan within 30 days.

- If the cancellation period has passed, many insurers allow regular cancellation. This usually requires giving notice about two weeks before the end of the month.

NOTE: We recommend sending your cancellation request via registered mail with a return receipt so you have proof of your cancellation.

What alternatives to residual debt insurance are there?

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

For small personal or car loans you don’t necessarily need residual debt or any other type of insurance. However, for real estate mortgage, it might make sense to protect yourself and your family financially.

Instead of taking residual debt insurance that covers your loan only, you can take the following insurance policies.

- Term insurance (Life insurance) to cover your family members in the event of your death. Term life insurance from Allianz* is rated the best by all the rating agencies in Germany..

- Occupational disability insurance covers you if you cannot work due to an illness. Finding the right insurance plan can be challenging, so we recommend consulting an insurance broker or advisor before taking out the policy.

Suppose you don’t take any insurance. In this case, you have the following options:

- Pay off your loan as fast as you can. The less outstanding debt you have, the lower your financial risk.

- If you’re financially struggling, talk to your bank early. Many banks allow you to extend the loan term to reduce monthly payments.

- Check whether your loan allows for a payment break. Some lenders let you pause installments for a few months for certain reasons (e.g., during unemployment). However, this may increase the total cost of the loan.

NOTE: Never stop monthly payments without informing the bank. It can have a negative impact on your credit history and may trigger debt collection procedures. If financial problems arise, contact your bank immediately.

Things that affect your credit history in Germany ->

FAQ

The residual debt insurance and loan contracts are two separate contracts. Thus, your loan terms don’t depend on whether you keep or cancel the insurance. If the bank threatens otherwise, ask for written justification and file a complaint with BaFin or Verbraucherzentrale.

No, you cannot transfer residual debt insurance to another loan. It is tied to a specific loan and its remaining debt. If you take out a new loan, you need a new insurance contract.

Yes, residual debt insurance can deny your claim due to a pre-existing illness. This is one of the most common reasons for denied claims.

More topics