Key Takeaways

- Net household saving rates diverged across the EU over time. Between 2004 and 2024, countries followed different paths, shaped by income growth, financial systems, and economic shocks.

- The COVID-19 pandemic changed saving a lot. In 2020, many countries saw people save much more money. Saving rates hit 22.2% in Ireland, 20.8% in Luxembourg, and 16.0% in Germany.

- Estonia shows the clearest structural shift. From −11.2% in 2004 to 3.0% in 2024, savings moved from credit-driven consumption to more cautious, income-based behaviour.

- Some countries faced declining saving rates, including Greece (−12.9 pp), Italy (−6.9 pp), and Belgium (−3.9 pp). This reflects weaker income growth and higher spending.

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

Need help communicating complex ideas visually? We help you turn data into your most persuasive story. Contact us to learn more.

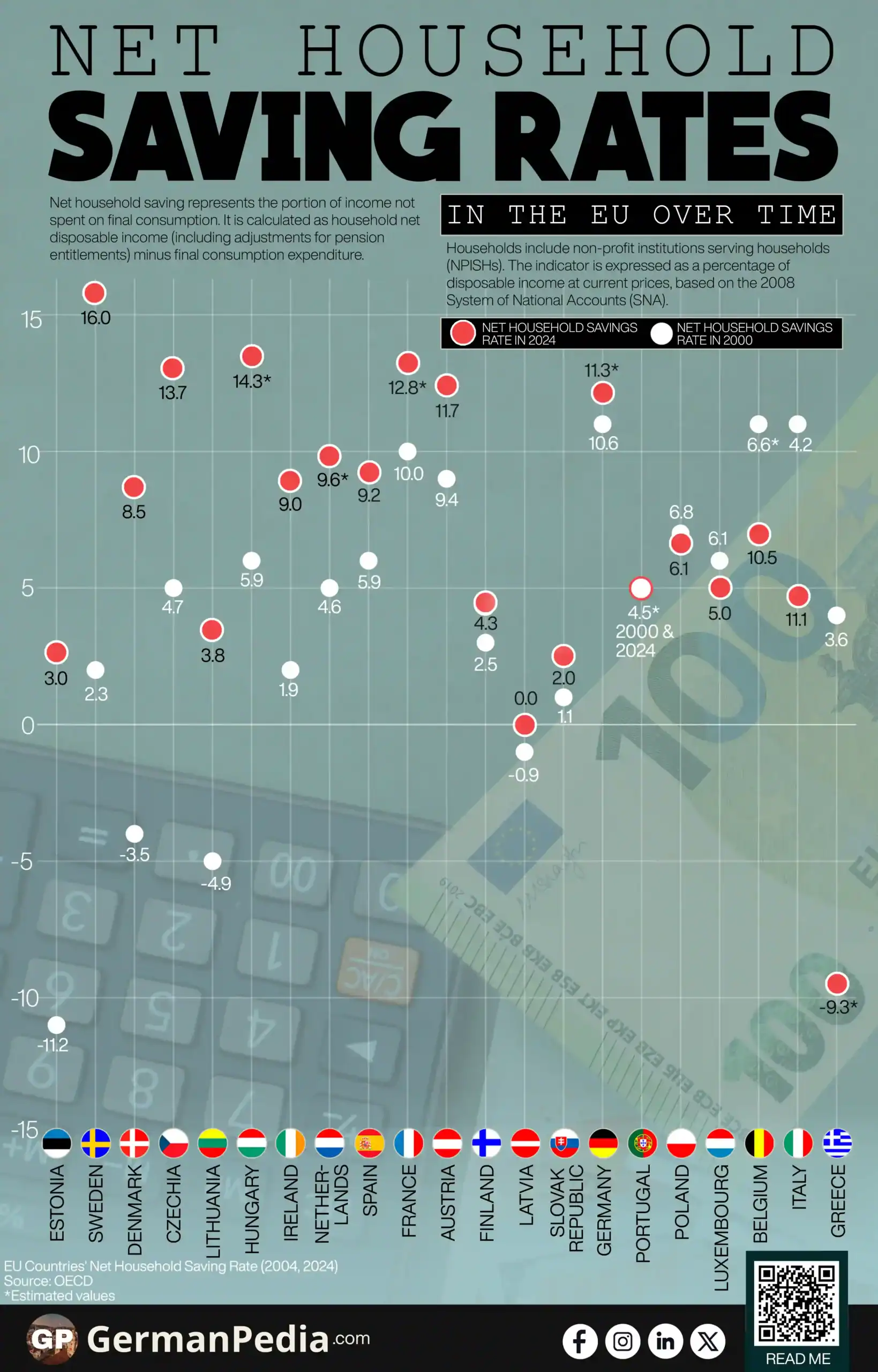

Net Household Saving Rate in EU Countries

| Country | Net Household Savings Rate | |||

|---|---|---|---|---|

| 2004 | 2020 | 2024 | Change in pp (2004-2024) | |

| Estonia | -11.2 | 9.2 | 3.0 | +14.3 |

| Sweden | 2.3 | 15.0 | 16.0 | +13.7 |

| Denmark | -3.5 | 3.0 | 8.5 | +11.9 |

| Czechia | 4.7 | 12.5 | 13.7 | +9.0 |

| Lithuania | -4.9 | 8.3 | 3.8 | +8.8 |

| Hungary | 5.9 | 12.0 | 14.3* | +8.4 |

| Ireland | 1.9 | 22.2 | 9.0 | +7.1 |

| Netherlands | 4.6 | 15.6 | 9.6* | +4.9 |

| Spain | 5.9 | 14.3 | 9.2 | +3.3 |

| France | 10.0 | 14.8 | 12.8* | +2.8 |

| Austria | 9.4 | 13.6 | 11.7 | +2.2 |

| Finland | 2.5 | 6.8 | 4.3 | +1.8 |

| Latvia | -0.9 | 9.7 | 0.0 | +1.0 |

| Slovak Republic | 1.1 | 5.4 | 2.0 | +0.8 |

| Germany | 10.6 | 16.0 | 11.3* | +0.7 |

| Portugal | 4.5 | 3.7 | 4.5* | −0.0 |

| Poland | 6.8 | 11.1 | 6.1 | −0.7 |

| Luxembourg | 6.1 | 20.8 | 5.0 | −1.1 |

| Belgium | 10.5 | 13.0 | 6.6* | −3.9 |

| Italy | 11.1 | 10.3 | 4.2 | −6.9 |

| Greece | 3.6 | -6.9 | -9.3* | −12.9 |

Source: OECD

*Estimated values

Net household saving represents the portion of income not spent on final consumption (e.g., food, rent, bills). It is calculated as household net disposable income (including adjustments for pension entitlements) minus final consumption expenditure. Households include non-profit institutions serving households (NPISHs). The indicator is expressed as a percentage of disposable income at current prices, using international accounting rules called the 2008 System of National Accounts (SNA).

Net household saving is the part of a household’s income that is not spent. It’s what’s left after paying taxes and buying things. In simple terms, it shows how much of their income people manage to keep instead of spend.

Between 2004 and 2024, saving habits changed differently in each EU country. The COVID-19 pandemic stands out as a moment when saving rates jumped sharply almost everywhere.

The largest increases are found in countries that started from low or even negative saving rates:

- Estonia: −11.2% → 3.0% (+14.3 pp)

- Sweden: 2.3% → 16.0% (+13.7 pp)

- Denmark: −3.5% → 8.5% (+11.9 pp)

- Czechia: 4.7% → 13.7% (+9.0 pp)

Estonia is the clearest example of this shift. Around 2004, savings were very low as consumption grew quickly, supported by credit and a housing boom. Many households were spending more than they earned.

Over time, this changed. After the 2008 global financial crisis, households became more careful with money. Incomes grew, people borrowed less, and the saving rate slowly rose.

Denmark’s low starting point shows a different system. Danish households typically carry high mortgage debt, but the country’s strong welfare system reduces the need for precautionary saving for risks such as unemployment or health shocks. This combination can result in low or even negative saving rates, even when overall household wealth remains high.

In contrast, Sweden and Czechia show a steadier pattern. Saving was already positive and increased further, supported by strong labour markets, rising incomes, and sound public finances. As the economy improved, households in these countries managed to save a bigger share of their income.

Top 10 Foreign Holders of German Government Debt ->

Meanwhile, some countries moved the other way, saving less over time:

- Greece: 3.6% → −9.3% (−12.9 pp)

- Italy: 11.1% → 4.2% (−6.9 pp)

- Belgium: 10.5% → 6.6% (−3.9 pp)

This reflects households that are often spending more than their income, for different reasons, such as:

- In Greece, the country’s gross disposable income is below 20% of the EU average, leaving less room to build savings.

- In Italy, years of government spending cuts and tax increases, slow wage growth, an ageing population, and a widening gap between rich and poor have all squeezed household budgets.

How did the pandemic affect the EU net household savings rate?

In many countries, saving rates jumped sharply during the COVID-19 pandemic:

- Ireland reached 22.2%

- Luxembourg rose to 20.8%

- Germany climbed to 16.0%

Many households faced a combination of different factors:

- Spending opportunities were limited due to lockdowns and restrictions.

- Government measures helped support incomes, reducing the need to cut consumption sharply.

- Heightened uncertainty encouraged precautionary saving.

These pandemic‑related shocks changed inflation patterns.

In 2020, people were buying less, so prices stayed low. Later, as people started buying more again, along with supply shortages and all the extra money people had saved, prices rose across the EU.

After 2020, interest rates rose sharply as central banks tightened policy to bring inflation back under control. This made borrowing more expensive and increased the return on savings compared with the low‑rate years of the 2010s.

Many households also stayed more cautious after the pandemic. Even once restrictions ended, spending did not fully return to pre‑pandemic levels. Some households, especially higher‑income groups, saved a large financial buffer and continued to sustain it.

Together, these factors helped keep net household saving rates elevated in most of the EU even after the initial shock had passed.

More topics

- GDP per Capita vs Actual Consumption per Capita in the EU

- Where are Billionaires Concentrated in the EU?

- Happiness vs Income in the EU

- Which Countries Use AI the Most in the EU?

- Electric and Hybrid Cars in the EU: Who Is Leading the Shift?

- Claude Usage in the EU: Which Countries Lead and Why?

- Petrol Prices Are Rising Across the EU

- Top 13 Most Valuable Brands in the EU

- Foreign-Born Population in the EU Is Rising

- EU Countries with the Most U.S. Troops

- Where are Billionaires Concentrated in the EU?

- Employment by Federal State in Germany

- Germany’s Median Wage by Federal State

- Top EU Countries Where People Say They Don’t Need AI

- EU Unicorn Startups: Which Countries Lead and Why

- EU Alternatives to Common US Platforms

- Most Surveilled Major Cities in the EU

References

- https://data-explorer.oecd.org/vis?fs[0]=Topic%2C1%7CEconomy%23ECO%23%7CNational%20accounts%23ECO_NAD%23&fs[1]=Topic%2C3%7CEconomy%23ECO%23%7CNational%20accounts%23ECO_NAD%23%7CGDP%20and%20non-financial%20accounts%23ECO_NAD_GNF%23%7CNational%20Accounts%20at%20a%20Glance%23ECO_NAD_GNF_NAT%23&pg=0&fc=Topic&snb=12&df[ds]=dsDisseminateFinalDMZ&df[id]=DSD_NAAG%40DF_NAAG_V&df[ag]=OECD.SDD.NAD&dq=A.AUT%2BCZE%2BDNK%2BEST%2BFIN%2BFRA%2BDEU%2BGRC%2BHUN%2BIRL%2BITA%2BLVA%2BLTU%2BLUX%2BNLD%2BPOL%2BPRT%2BSVK%2BESP%2BSWE%2BBEL.B8NS1M..&pd=2004%2C2024&to[TIME_PERIOD]=false&vw=tb

- https://www.elibrary.imf.org/view/journals/001/2023/150/article-A001-en.xml

- https://ec.europa.eu/eurostat/statistics-explained/SEPDF/cache/65805.pdf

- https://haldus.eestipank.ee/sites/default/files/publication/en/Archive/kroon_economy/2007/_5.pdf

https://dipartimenti.unicatt.it/politica-economica-ISPE0063.pdf - https://www.nationalbanken.dk/media/xmzow4j0/em-inequality-and-savings-memo.pdf

- https://www.ecb.europa.eu/press/economic-bulletin/focus/2022/html/ecb.ebbox202205_03~d262f01c8b.en.html

- https://www.kbc.com/en/economics/publications/belgians-are-saving-less-and-less-and-that-has-implications%20%20%20.html