Key takeaways

- Private health insurance is a cheaper and better option for high earners only.

- Unlike public health insurance, private health insurance costs don’t depend on your income.

- Private health insurance premiums rose 3.4% per annum between 2006 and 2026. On the other hand, public health insurance costs rose 3.9% per annum between 2006 and 2026.

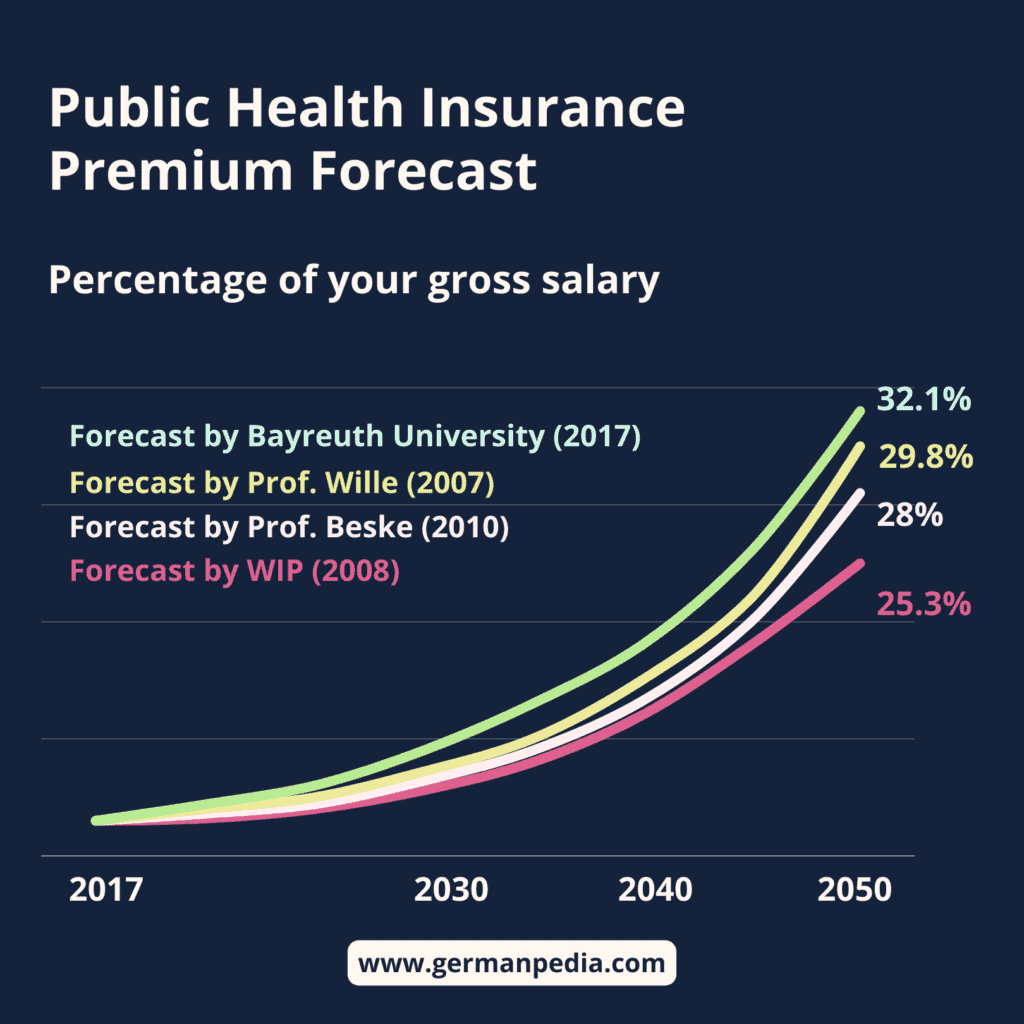

- Experts predict you’ll pay between 25% and 32% of your gross salary in public health insurance by 2050.

This is how you do it

- Educate yourself about the private health insurance system in Germany.

- Use our "Health Insurance Finder" tool to check which health insurance is best for you.

- We recommend getting private health insurance via an insurance broker. They are experts and can help you find the best plan for your needs. You can book a call with an expert we recommend here.

- In our comparison and test, we found Haellesche, Allianz, and Signal Iduna's private health insurance plans to be the best.

The AI overview and answers are as good as the sources it uses.

To ensure you get AI answers from a deeply researched, maintained, and up-to-date source, add GermanPedia to your preferred sources.

Table of Contents

Private health insurance offers better coverage than public health insurance, yet it’s cheaper. You may ask how that is possible.

Note that private health insurance is cheaper for high earners only. Low earners cannot afford private health insurance in Germany.

Here are the reasons why private insurance is cheaper for high earners.

- Every insured member of private health insurance pays a contribution

- Private health insurance companies accept only healthy individuals

- Private health insurance providers save part of the monthly contribution to keep the premium stable in old age.

- Only high-paid individuals can join the private healthcare system.

- The increasing aging population in Germany

Let’s understand each point in detail.

#1 Every insured member of private health insurance pays a contribution

Private health insurance does not offer free coverage for your non-working partner or children. Everyone must make contributions to get services.

On the other hand, with statutory health insurance, you can insure your non-working spouse and children for free. The statutory system has 15.1 million (as of 2025) people insured for free.

However, the public system needs money to run. So, its only option is to collect money from those with income.

The earning population of the public health system must contribute enough to cover

- their medical expenses and

- the medical costs of freely insured members.

Additionally, public health insurance premiums depend on your income. So, the higher you earn, the more the health insurance cost.

On the other hand, with private health insurance, you only pay the premium for yourself. The insurance company calculates the premium based on your

- health condition,

- age, and

- your estimated total medical expenses throughout life.

This makes private health insurance premiums lower than public health insurance premiums for high earners.

#2 Private health insurance companies accept only healthy individuals

Private health providers have the right to choose their customers. So, they accept only healthy and young individuals as their customers.

As you can imagine, young and healthy individuals don’t get sick often. This keeps the expenses of the private health insurance system low.

On the other hand, public health insurance cannot choose their customers. So, unhealthy people who cannot get private insurance must join the public health insurance system.

So, the expenses per insured member of public health insurance are higher than those of private health insurance for similar services. This leads to higher public health insurance premiums than private.

We recommend getting private health insurance via an insurance broker. They are experts and can help you find the best plan for your needs. You can book a call with an insurance broker we recommend here.

Insurance brokers and advisors are liable for their advice. This means that if the insurance plan they recommended doesn’t fulfill your wishes, they are liable to pay the damages.

Insurance brokers offer free advice. The insurance company pays them upon the successful conclusion of the contract.

An insurance broker can also help you file a claim with the provider. The broker we recommend has been offering services to expats for more than a decade.

Book a free call with a health insurance expert

- German health insurance is a complicated product. There are several factors that must be considered before deciding which health insurance is best for you. An expert can guide you and help you pick the best option for you.

- An Insurance broker is liable for their advice. This means if the policy they recommended doesn’t offer the coverage you requested, they are liable to pay the damages incurred in the future.

#3 Aging provisions

Medical expenses increase as you age, and Germany has an aging population. So, the medical expenses of the German population are growing.

The two German healthcare systems tackle the aging problem differently. Their approach to solving it significantly affects insurance premiums.

How does the public healthcare system solve the aging problem?

Public health insurance relies on young professionals to pay for the increased medical expenses of retired insurance members. In other words, the current generation pays for the previous generation.

This is why Germany’s aging population threatens the survival of the statutory healthcare system.

There won’t be enough young professionals to pay for the retired. Hence, it’ll lead to unaffordable insurance premiums in the future.

Currently, the German government offers billions of euros in subsidies to public health insurance companies to keep them running.

The situation worsens as public health insurance does not have a concept of aging reserves.

How does the private healthcare system solve the aging problem?

In the past, private health insurers also didn’t save for old age. No aging provisions led to unaffordable insurance premiums in old age.

This is why many baby boomers have bad experiences and stories about private health insurance. However, private health insurance companies and the German government learned from their past mistakes.

Since 2000, every private health insurance company has been legally required to save part of the monthly premium. The insurer uses this saved amount to compensate for increased medical costs in your old age. Thus, it keeps the premium stable in old age.

This saving is called aging provisions (Altersrückstellungen in German).

Aging reserves don’t mean that your premiums won’t increase. It means that your premium in old age and the premium of a young person at that time will be the same.

In other words, you need more medical services than a young individual does in your old age. However, both you and the young individual will pay the same premium. This is possible because your aging reserves compensate for the increased medical expenses.

#4 30% of the people in Germany are 60 or above

Germany has an aging population. 30% of the German population is 60 and above, and 45% is 50 and above.

Only 31% of the population is between 25 and 49 [4]. This poses a huge threat to the German economy and to keeping the country running.

Many experts forecast that public health insurance contributions will rise from 16.3% of your gross salary (as of 2024) to 30% by 2050.

Private health insurance is also affected by the German aging population. So, the private health insurance premiums will also increase in the future.

However, private health insurance is better prepared for the future with 354 billion euros as of 03 Dec 2025 in aging reserves. Private health insurance companies use this amount to stabilize the premium in old age.

#5 Only high-paid individuals can join the private healthcare system.

To be eligible for private health insurance, you must earn above 77,400€ (as of 2026). This limit applies to employed individuals only.

Self-employed and civil servants with lower incomes can also join private health insurance. However, as per experts, private health insurance is not a good option for low earners.

Statistically, high-paid employees are also highly educated and spend more on their health than low-earning employees. Thus, one can deduce that high-earners are healthier than low-earners and, ultimately, less expensive to the health system.

This also supports the private healthcare system in keeping the premiums lower than the public healthcare system.

Conclusion

Premiums for both public and private health insurance will increase in the future. This is due to inflation and medical advancements.

Thus, regardless of which health insurance you choose, save for your retirement. Otherwise, you won’t be able to afford the health insurance premiums in old age.

NOTE: Don’t rely on the government to fix the broken healthcare system. Save for the worst times instead.

One of the best ways to save on autopilot is to start an ETF savings plan. You even get tax benefits if you invest in stock-based ETFs in Germany.

During our research, we found Scalable Capital*, SmartBroker+*, or Finanzen.net Zero* as the best online brokers in Germany. You can compare all online brokers in Germany and explore their key features here.

Premiums are among the many factors you must consider when taking out health insurance. You should also consider your health condition, family situation, and long-term strategy.

Individuals suffering from serious illness prefer the best medical treatment. In this case, private health insurance is the right choice. However, getting private insurance is impossible once you develop a serious health problem.

On the other hand, single earners in a family usually cannot afford private health insurance. This is why you should consider all the factors when making a decision.

You can use our “Health Insurance Finder” tool to check which health insurance (Public or Private) makes sense and when. We recommend getting advice from a fee-based advisor or health insurance broker before deciding.

Public and private health insurance costs in Germany

Public health insurance costs depend on your income. On the other hand, private health insurance costs depend on your age and health.

When comparing public and private insurance costs, we’ll assume you are a high earner. This is because private health insurance makes sense only for high earners.

2026 Cost Projection of Private and Public Health Insurance

| Age (Nr. of years after taking private insurance) | Private health insurance | Public health insurance | |

| Yearly increase in premium over the past 20 years (2006 to 2026) | 3.4% | 3.9% | |

| Premium of a high-earner, self-employed individual | Premium increases by 3.4% per annum | Premium increases by 3.9% per annum | |

| Age 35 (2026) | 920€ | 1,017€ | |

| Age 45 (after 10 years) | 1,285€ | 1,491€ | |

| Age 55 (after 20 years) | 1,796€ | 2,186€ | |

| Age 65 | 2,509€ | 3,205€ | |

| After Retirement | |||

| Age 67 (priced on retirement income) | 2,469€ (you stop paying for the sickness benefit) | 1,298€ (if you stay in public insurance throughout your work life) | 2,595€ (if you are voluntarily insured in public insurance after retirement)We assume that you have saved enough to generate 75% of your last income. |

| Maximum subsidy from pension insurance | 0€ (no state pension assumed) | 0€ (already built into the rate, no separate subsidy) | 0€ (no state pension assumed) |

| Net after retirement | 2,470€ | 1,380€ | 2,760€ |

| Total premium paid in 32 years(From age 35 to 67) | 621,852€ | 751,551€ | 751,551€ |

2025 Cost Projection of Private and Public Health Insurance

| Age (Nr. of years after taking private insurance) | Private health insurance | Public health insurance | |

| Yearly increase in premium over the past 10 years (2015 to 2025) | 3.9% | 4.1% | |

| Yearly increase in premium over the past 20 years (2005 to 2025) | 3.1% | 3.8% | |

| Premium of a high-earner, self-employed individual | Premium increases by 3.9% per annum | Premium increases by 4.1% per annum | |

| 35 (today) | 800 € (as of 2025) | 1174 € (as of 2025) | |

| 45 (after 10 years) | 1172 € | 1754 € | |

| 55 (after 20 years) | 1719 € | 2622 € | |

| 65 (after 30 years) | 2520 € | 3919 € | |

| After Retirement | |||

| 67 | 2320 € (you stop paying the sickness benefits) | 1400 € (if you stay in public insurance throughout your work life) | 3000 € (if you are voluntarily insured in public insurance after retirement) We assume that you have saved enough to generate 75% of your last income. |

| Maximum subsidy from pension insurance | 200 € (approx. as of 2024) | 200 € (approx. as of 2024) | 200 € (approx. as of 2024) |

| Net premium you pay after retirement (67) | 2120 € (2320 – 200) | 1200 € (1370 – 200) | 2800€ (3000 – 200) |

| Total premium paid in 32 years (From age 35 to 67) | 588,000€ | 873,000€ | 873,000€ |

As you can see, if you are a high earner, you’ll pay way more in the public system than in private throughout your working life. After retirement, private health insurance premiums are usually higher than public (KVdR).

This is why experts recommend creating a long-term strategy when purchasing private health insurance. You should save or invest the savings from moving to private health insurance.

These savings can help you pay the entire private insurance premium after retirement.

Moreover, you can reduce the cost of private health insurance by changing your plan or increasing the deductible. In the worst-case scenario, you move to the basic tariff of private health insurance that offers the same services as public insurance.

You should also consider that the public health system is in financial trouble. So, the chances that the German government will reduce or cut the public health insurance subsidy for retirees in the future are high.

Lastly, paying more in the public system doesn’t mean getting better services. On the contrary, good private health insurance plans offer better services than public insurance.

We recommend getting private health insurance via an insurance broker. They are experts and can help you find the best plan for your needs. You can book a call with an insurance broker we recommend here.

Book a free call with a health insurance expert

- German health insurance is a complicated product. There are several factors that must be considered before deciding which health insurance is best for you. An expert can guide you and help you pick the best option for you.

- An Insurance broker is liable for their advice. This means if the policy they recommended doesn’t offer the coverage you requested, they are liable to pay the damages incurred in the future.

More topics

- Is private health insurance worth it?

- Best private health insurance companies (Experts Rating)

- Private vs public health insurance

- Services a good private health insurance must cover

- Private health insurance for self-employed in Germany

- Private health insurance for the unemployed in Germany

- Private health insurance for students in Germany

- Private health insurance for children in Germany

- Family health insurance in Germany

- Minimum coverage your private health insurance plan should offer

![Number of People Insured in Public Health Insurance in Germany [2000-2025]](https://fefffe12.delivery.rocketcdn.me/wp-content/uploads/2025/03/number-of-people-insured-in-gkv-and-pkv-768x1152.webp)

![Number of People Insured in Public & Private Health Insurance in Germany [2025]](https://fefffe12.delivery.rocketcdn.me/wp-content/uploads/2025/03/number-of-people-insured-in-gkv-and-breakdown-768x1152.webp)