Key Takeaways

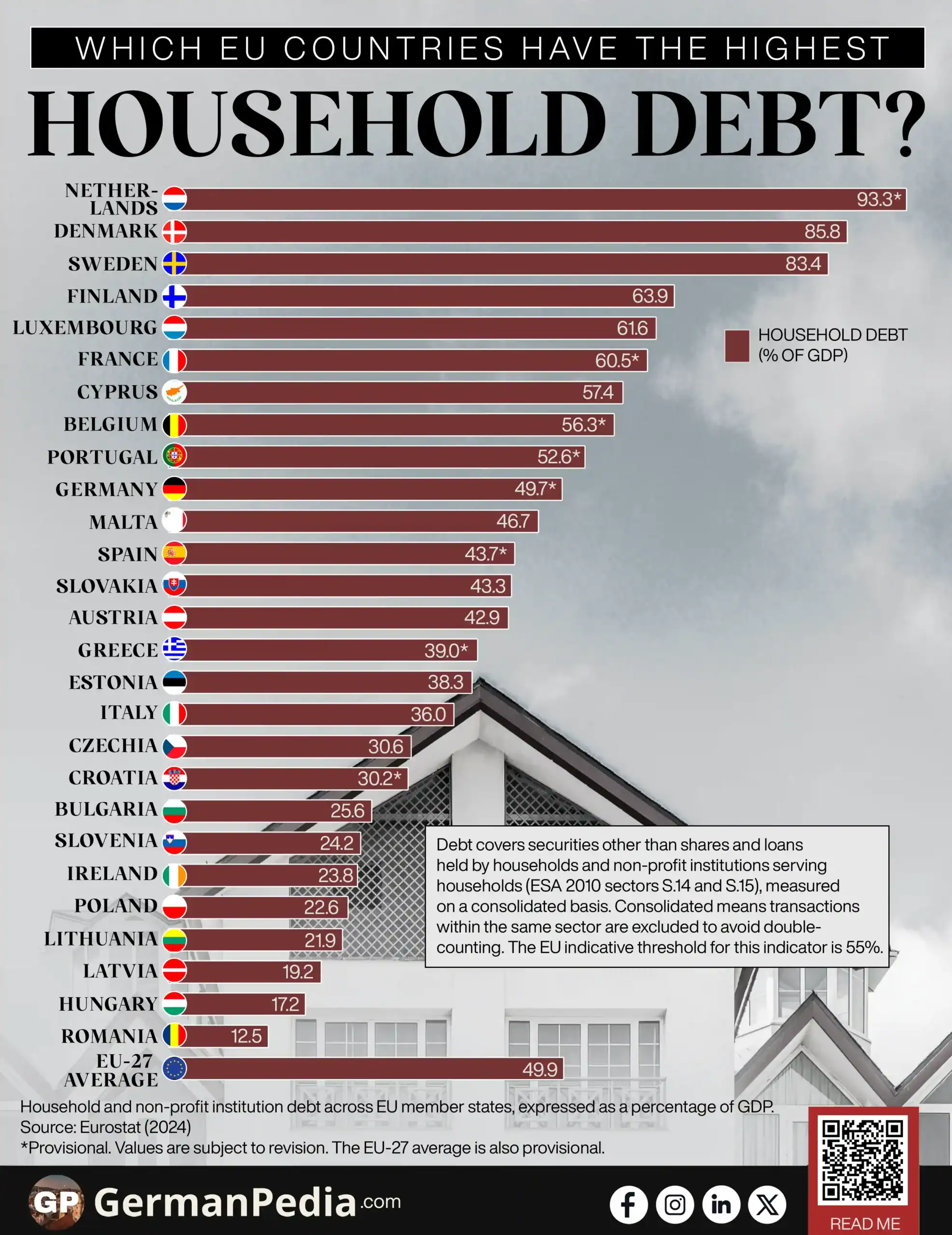

- The Netherlands leads the EU at 93.3% of GDP. That is nearly double the EU average of 49.9%. Three structural policies drive this: mortgage interest tax deductibility, a 100% loan-to-value allowance, and widespread interest-only mortgages.

- Every country above the 55% threshold is in Northern or Western Europe. Denmark, Sweden, Finland, Luxembourg, France, Cyprus, and Belgium all sit above the line.

- Every country below 30% of GDP is in Central or Eastern Europe. Romania ranks lowest at 12.5%. Hungary (17.2%), Latvia (19.2%), Lithuania (21.9%), and Poland (22.6%) follow.

- Low debt levels in Central and Eastern Europe trace to the 1990s. State-owned housing was privatised and sold to residents at heavily discounted prices. Most households in these countries own their homes outright with no mortgage.

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

Need help communicating complex ideas visually? We help you turn data into your most persuasive story. Contact us to learn more.

Household Debt as a Share of GDP Across EU Countries

| Country | Household Debt (% of GDP) |

|---|---|

| Netherlands | 93.3* |

| Denmark | 85.8 |

| Sweden | 83.4 |

| Finland | 63.9 |

| Luxembourg | 61.6 |

| France | 60.5* |

| Cyprus | 57.4 |

| Belgium | 56.3* |

| Portugal | 52.6* |

| Germany | 49.7* |

| Malta | 46.7 |

| Spain | 43.7* |

| Slovakia | 43.3 |

| Austria | 42.9 |

| Greece | 39.0* |

| Estonia | 38.3 |

| Italy | 36.0 |

| Czechia | 30.6 |

| Croatia | 30.2* |

| Bulgaria | 25.6 |

| Slovenia | 24.2 |

| Ireland | 23.8 |

| Poland | 22.6 |

| Lithuania | 21.9 |

| Latvia | 19.2 |

| Hungary | 17.2 |

| Romania | 12.5 |

| EU-27 Average | 49.9 |

Source: Eurostat (2024)

Debt covers securities other than shares and loans held by households and non-profit institutions serving households (ESA 2010 sectors S.14 and S.15), measured on a consolidated basis. Consolidated means transactions within the same sector are excluded to avoid double-counting. The EU indicative threshold for this indicator is 55%.

*Provisional. Values are subject to revision. The EU-27 average is also provisional.

In 2024, eight of the EU’s 27 member states carry household debt above 55% of GDP. The EU’s Macroeconomic Imbalance Procedure uses that figure as a warning level to identify countries where household borrowing poses an economic risk.

Household debt measures the total outstanding loans and debt securities held by private households. In this article, it is expressed as a share of a country’s annual economic output. The higher the ratio, the more households owe relative to the size of the economy they live in.

The Netherlands Leads EU Household Debt at 93.3% of GDP

The Netherlands carries the highest household debt in the EU at 93.3% of GDP. That figure sits 7.5 percentage points above Denmark, the second-highest country at 85.8%. It is nearly double the EU average of 49.9%.

Three structural policies drive the Netherlands to the top:

- Dutch law allows homeowners to deduct mortgage interest payments from their taxable income. This makes borrowing to buy a home significantly cheaper than in countries without such a subsidy.

- The country permits a loan-to-value ratio of up to 100%. Buyers can finance the full purchase price of a home through a mortgage, with no deposit required.

- Interest-only mortgages have historically been widespread. In this structure, borrowers repay no principal during the loan term, keeping the total debt balance high for longer.

Together, these policies have pushed Dutch household debt to levels that regulators have flagged as a financial stability risk.

The other seven countries above the threshold are Denmark (85.8%), Sweden (83.4%), Finland (63.9%), Luxembourg (61.6%), France (60.5%), Cyprus (57.4%), and Belgium (56.3%). Every country above the line is in Northern or Western Europe. These countries share developed mortgage markets, high rates of homeownership financed through long-term loans, and broad access to consumer credit. The cluster reflects economies where borrowing to buy a home is the standard route into ownership.

Central and Eastern EU Countries Carry the Lowest Debt

Every country below 30% of GDP is in Central or Eastern Europe:

- Romania: 12.5%

- Hungary: 17.2%

- Latvia: 19.2%

- Lithuania: 21.9%

- Poland: 22.6%

The structural reason dates back to the 1990s. After the fall of communism, state-owned housing across Central and Eastern Europe was privatised and sold to existing residents at heavily discounted prices. Romania has a homeownership rate of 93%. Most households in these countries own their homes outright with no mortgage. Debt levels are low because borrowing to buy housing was never the norm.

Less developed consumer credit markets reinforce this pattern. Households in these countries have historically had fewer opportunities to take on debt, regardless of preference.

Two Housing Systems, One EU Average

The EU average of 49.9% sits just below the 55% threshold. This average reveals a structural divide. In Northern and Western Europe, homeownership runs through long-term mortgage debt. In Central and Eastern Europe, ownership is widespread but largely debt-free, a direct legacy of post-communist privatisation.

The gap does not reflect different attitudes toward spending. It reflects the different systems each group of countries inherited.

More topics

- GDP of European Countries

- European Union’s Debt Has Grown Sharply Over Two Decades

- Top 10 Foreign Holders of German Government Debt

- Most Prosperous EU Countries by Prosperity Index

- Which EU Country Has the Highest Trade-to-GDP Ratio?

- EU Rent Price Index by Country Over Time

- Europe’s Population Shifted Over 20 Years

- Which European Countries Hold the Most Gold Reserves?

- Top 10 Richest Women in the EU

- Life Expectancy in European Countries

- EU Unicorn Startups: Which Countries Lead and Why

- Women Are Increasing in Managerial Roles Across the EU

- Average Working Hours in EU Countries

- Which EU Countries Have the Highest Unemployment?